🧪 The Story of Chemicals – From Mystery to Modern Life

Long ago, when humans first lit a fire 🔥, they didn’t know it — but they were already playing with chemicals. Burning wood, melting metals, mixing herbs into medicine… these were mankind’s first steps into the world of chemistry.

For centuries, people called it alchemy — a mix of magic and mystery. Ancient Egyptians colored their walls with mineral dyes. In India, ayurvedic healers mixed herbs and salts. In China, alchemists discovered gunpowder by accident. Every civilization was writing a new chapter in the story of chemicals.

But the real turning point came in the 18th century. A Frenchman, Antoine Lavoisier, looked at fire and said: “This is not magic, this is science.” He proved that air has oxygen, that matter cannot be destroyed, only transformed. His work laid the foundation for modern chemistry. People began to realize: chemicals are not dangerous mysteries, they are the building blocks of life.

Then came John Dalton in 1803. He gave the Atomic Theory — explaining that everything, from the stars above 🌌 to the soil beneath our feet 🌱, is made of tiny atoms. This was a revolution. Suddenly, the invisible world had a language, and that language was chemistry.

From that moment, chemicals became the silent partners of progress. They cured diseases through medicines 💊, fed billions through fertilizers 🌾, built modern cities with plastics and cement 🏙️, and today they even power electric cars and green energy ⚡.

So, what is a chemical in simple words?

👉 A chemical is not just a substance — it is a story of transformation, a key that unlocked the progress of human civilization.

And the reason why?

Because mankind has always been a dreamer and a problem-solver. We studied chemicals not just to understand the world, but to change it, improve it, and create a better future.

Chemicals teach us a timeless lesson: everything can transform. Coal can become diamond, crude oil can become medicine, and with the right vision, problems can turn into opportunities. Just like chemistry transforms elements, we too can transform challenges into success.

🧪 The Industrialization of Chemicals: When, Where, and How it Happened

⚙️ Introduction

The industrialization of chemicals stands as one of humanity’s greatest catalysts for progress. From the roots of alchemy to vast modern plants, chemical manufacturing has shaped science, economies, and societies, pointing to a future of remarkable opportunities and urgent responsibilities. The journey of this sector is a testament to vision, innovation, and cross-border enterprise—qualities at the heart of successful business leadership today.

🏭 Origins and Early Developments

The chemical industry’s birth can be traced to the 18th-century Industrial Revolution, beginning in Britain and rapidly expanding into Europe and North America. Early breakthroughs emerged from the needs of textiles, where bottlenecks in bleaching drove inventors to discover more efficient solutions. Joshua Ward’s practical sulfuric acid production in 1736 and John Roebuck’s large-scale lead chamber method in 1749 laid the foundation for volume manufacturing. Developments like Charles Tennant’s cheap bleaching powder revolutionized processing, enabling textile factories to scale up and meet exploding global demand.

🌍 Expansion Across Continents

By the mid-19th century, the chemical industry had matured to meet the demands of diversified manufacturing. Mass production of sulfuric acid and sodium carbonate via the Leblanc and later Solvay processes signaled new eras of efficiency and global competitiveness. Belgium’s Ernest Solvay perfected and commercialized the ammonia-soda process, making alkali production cleaner and more cost-effective. Transformative players such as Solvay in Belgium, Brunner, Mond & Co. in England, and Lawes’ superphosphate fertilizers in the UK fueled agricultural and technological leaps.

German ingenuity propelled organic chemical synthesis—including synthetic dyes, perfumes, and early plastics—pushing the boundaries of industry application. By 1913, three German giants—BASF, Bayer, and Hoechst—dominated the world’s supply of synthetic dyes, demonstrating how scientific discovery powered commercial success.

🏢 Chemical Engineering: Professionals and Processes

As the industry grew, a new discipline—chemical engineering—emerged to optimize large-scale processes. Batch production transitioned to continuous, assembly-line manufacturing, enabling vast outputs at lower costs. George E. Davis, recognized as the father of chemical engineering, introduced unit operations and coined the term, establishing chemical engineering as a cornerstone of modern business and industry.

🔗 Impact on Business and Society

The industrialization of chemicals has shaped modern life in countless ways:

- Healthcare: Mass production of pharmaceuticals, vaccines, and antiseptics transformed global health.

- Agriculture: Artificial fertilizers and pest control have multiplied yields, feeding billions.

- Transport and Construction: Petrochemicals and plastics revolutionized vehicles, infrastructure, and housing.

- Consumer Goods: Everyday products—from soaps to textiles and food preservatives—are sourced from chemical innovation.

Leadership in this domain has meant not just business growth but also confronting new challenges—from pollution regulations first introduced in the UK in 1863, to ongoing debates on sustainability and the circular economy.

🚀 Technology and Evolution

The 20th century witnessed consolidation, expansion, and innovation at a scale never before imagined. Petrochemical giants emerged, and new processes such as catalytic cracking revolutionized fuel and plastic production. World events—wars, discoveries, and globalization—led to merges and expansions; IG Farben (Germany), DuPont (USA), and Imperial Chemical Industries (UK) became household names and multinational forces.

Modern chemical companies operate across continents, investing billions in research and development to create sustainable polymers, specialty chemicals, and advanced pharmaceuticals. Digitalization—automation, data analytics, and collaborative platforms—has further accelerated transformation, making supply chains transparent, competitive, and resilient.

🌐 Future of the Chemical Industry

Business leaders face an era of promise and responsibility, as the future of chemical industrialization hinges on green innovation and strategic vision. Sustainability defines the new frontier. Circular economy principles, sourcing renewable feedstocks, carbon capture technologies, and green chemistry will distinguish tomorrow’s industry stewards from mere participants.

Emerging economies—China, India, Brazil—are reshaping global supply chains, providing leadership opportunities for businesses that embrace adaptability and collaboration. Digital transformation and AI-driven innovation will empower stronger safety, efficiency, and discovery. The chemical industry’s history is not just a story of products, but of people—visionaries, researchers, and entrepreneurs who dared to dream bigger.

🌟 Leadership Call: Shaping the Next Chapter

Visionary business leadership in chemicals means thinking beyond profits—towards stewardship, innovation, and partnership. Industrialization has overcome immense obstacles. Now, the challenge is to sustain growth ethically, serve communities, and create solutions for tomorrow’s world. With legacy as a guide and innovation as a tool, the next industrial chapter belongs to those who seize opportunity, value collaboration, and refuse to compromise on progress.

Industrialization is not just history; it is the ongoing adventure of ambition, resilience, and responsible growth. May business leaders continue to build, inspire, and unlock the limitless potential of chemistry for generations to come.

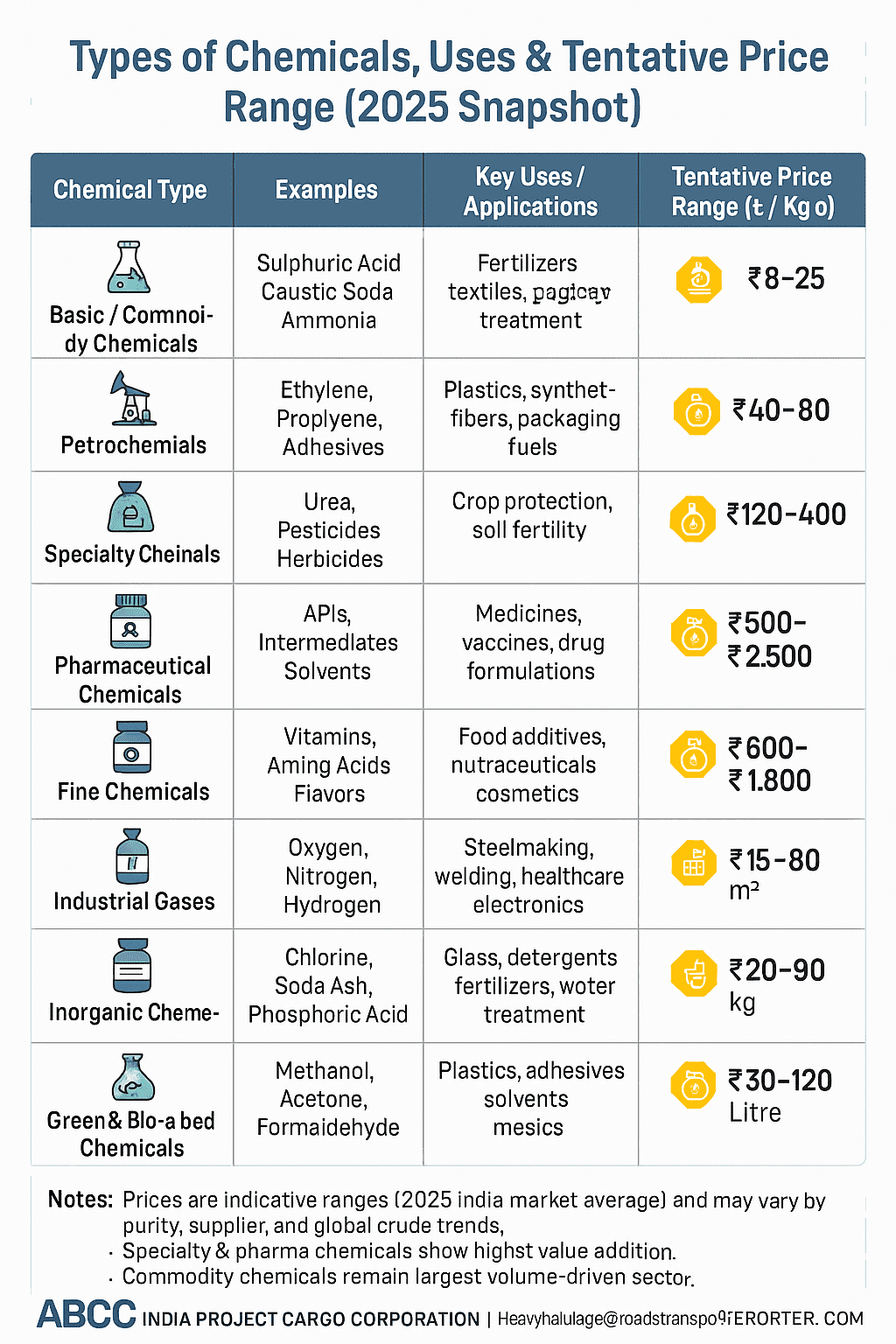

Types of Chemicals, Uses & Tentative Price Range

| Chemical Type | Examples | Key Uses / Applications | Tentative Price Range (₹ / Kg or Litre) |

|---|---|---|---|

| Basic / Commodity Chemicals | Sulphuric Acid, Caustic Soda, Ammonia | Fertilizers, textiles, water treatment | ₹8 – ₹25 / Kg |

| Petrochemicals | Ethylene, Propylene, Benzene | Plastics, synthetic fibers, packaging, fuels | ₹40 – ₹80 / Kg |

| Specialty Chemicals | Dyes, Pigments, Adhesives | Paints, coatings, automotive, electronics | ₹120 – ₹400 / Kg |

| Agrochemicals | Urea, Pesticides, Herbicides | Crop protection, soil fertility | ₹20 – ₹250 / Kg |

| Pharmaceutical Chemicals | APIs, Intermediates, Solvents | Medicines, vaccines, drug formulations | ₹500 – ₹2,500 / Kg |

| Fine Chemicals | Vitamins, Amino Acids, Flavors | Food additives, nutraceuticals, cosmetics | ₹600 – ₹1,800 / Kg |

| Industrial Gases | Oxygen, Nitrogen, Hydrogen | Steelmaking, welding, healthcare, electronics | ₹15 – ₹60 / m³ |

| Inorganic Chemicals | Chlorine, Soda Ash, Phosphoric Acid | Glass, detergents, fertilizers, water treatment | ₹20 – ₹90 / Kg |

| Organic Chemicals | Methanol, Acetone, Formaldehyde | Plastics, adhesives, solvents, resins | ₹30 – ₹120 / Litre |

| Green & Bio-based Chemicals | Bio-ethanol, Bioplastics, Enzymes | Renewable fuels, packaging, sustainable materials | ₹60 – ₹200 / Litre/Kg |

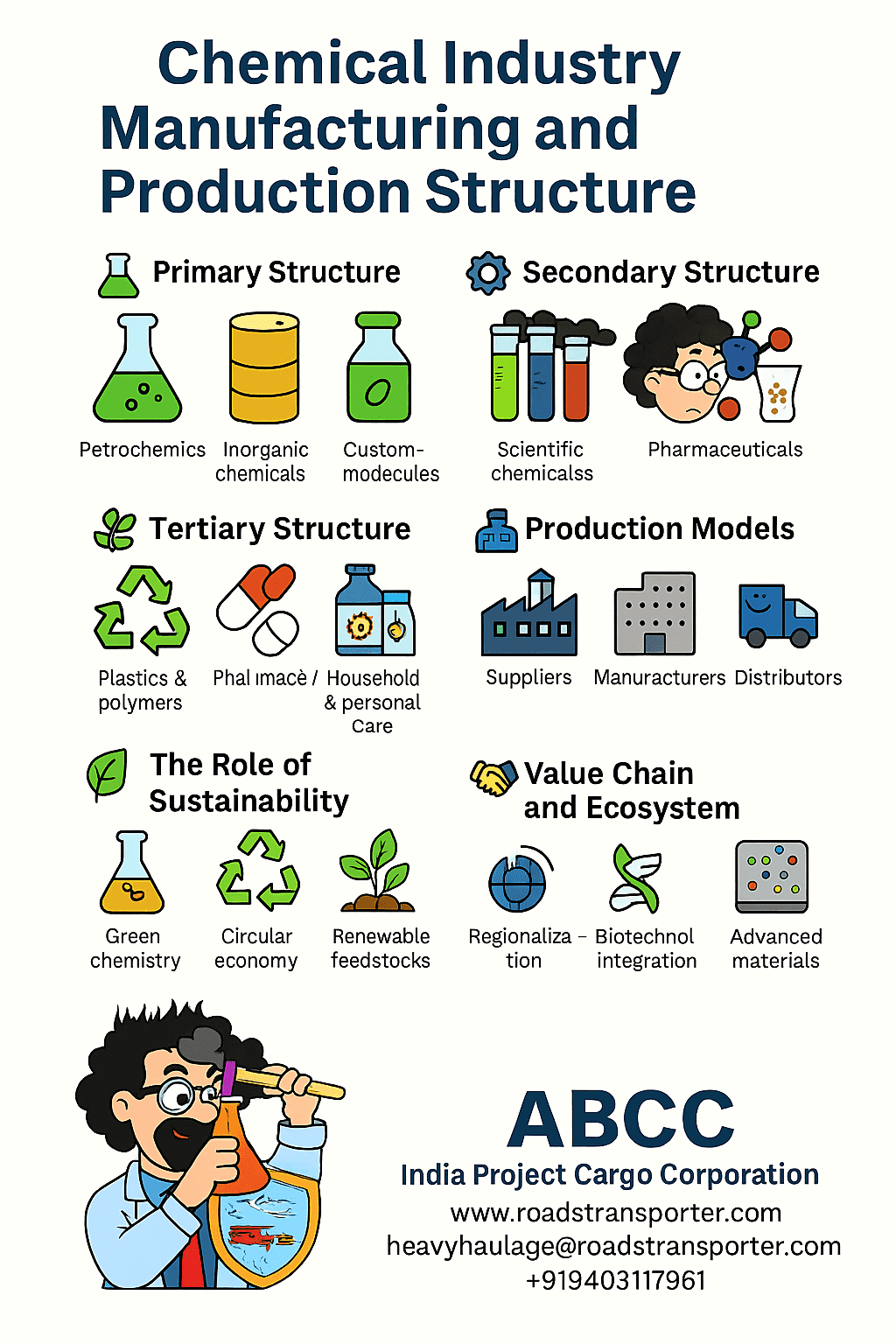

🏭 Chemical Industry Manufacturing and Production Structure

The chemical industry is one of the world’s most complex and essential sectors, powering agriculture, energy, construction, healthcare, and technology. Its manufacturing and production structure represents a fusion of science, engineering, and global business strategy. Understanding this structure provides leaders with insight into how the industry adds value, drives innovation, and sustains economic growth.

🔬 Primary Structure: Basic Chemicals

The foundation of the chemical industry lies in the primary or base chemicals. These are produced in high volumes and serve as building blocks for almost every other chemical product.

- Petrochemicals – Derived from crude oil and natural gas, they form the backbone for plastics, synthetic fibers, and fuels.

- Inorganic chemicals – Such as sulfuric acid, chlorine, soda ash; essential in fertilizers, detergents, and glass.

- Intermediates – Serve as transition products for further chemical transformations.

💡 Leadership Insight: Primary chemicals are about scale and cost efficiency. Global leaders excel in managing large plants and raw material supply chains.

⚙️ Secondary Structure: Specialty and Fine Chemicals

Once base chemicals are established, the industry moves into specialty and fine chemicals. These involve more complex processes, smaller volumes, and higher value.

- Specialty chemicals – Coatings, adhesives, construction chemicals, agrochemicals, water treatment solutions.

- Fine chemicals – High-purity, custom-made molecules used in pharmaceuticals, electronics, and biotechnology.

📊 Leadership Insight: This segment demands innovation, customization, and R&D investments. Companies win here not through scale, but through differentiation and intellectual property.

🧪 Tertiary Structure: Consumer and End-Use Products

At the final stage, chemicals transform into end-user products directly touching human lives.

- Plastics & Polymers – Packaging, automotive, textiles, electronics.

- Pharmaceuticals – Life-saving drugs, vaccines, diagnostic chemicals.

- Household & Personal Care – Detergents, cosmetics, hygiene products.

🌍 Leadership Insight: Here, branding, customer trust, and regulatory compliance are critical. This is where chemical companies most visibly influence society.

🏭 Production Models in the Chemical Industry

The production structure is also defined by how companies organize manufacturing plants and supply chains:

- Integrated Production (Clusters):

- Massive complexes where raw material, energy, and utilities are shared across units.

- Examples: Chemical hubs in Germany’s Ruhr Valley, India’s Gujarat, and the U.S. Gulf Coast.

- Dedicated Plants (Focused Manufacturing):

- Specialized plants for one or few products (e.g., ammonia, methanol, or resins).

- Highly automated for efficiency and consistency.

- Contract Manufacturing:

- Outsourced production for smaller players, common in pharmaceuticals and specialty chemicals.

💡 Leadership Insight: Efficiency is no longer enough—leaders must design plants with sustainability and digital transformation at the core.

🌱 The Role of Sustainability

No modern discussion on chemical manufacturing is complete without addressing sustainability:

- Green Chemistry: Designing processes that reduce waste and energy consumption.

- Circular Economy: Recycling and reusing plastics and materials.

- Renewable Feedstocks: Bio-based raw materials replacing petrochemicals.

- Carbon Neutrality: Investments in carbon capture and clean energy.

📈 Leadership Insight: Tomorrow’s winners will not be the largest players but the most sustainable innovators.

🤝 Value Chain and Ecosystem

The chemical industry does not work in isolation. Its structure is deeply interconnected:

- Suppliers: Oil & gas companies, mining operations, renewable feedstock providers.

- Manufacturers: Base chemical producers, specialty chemical innovators.

- Distributors: Traders, logistics firms, and bulk shipping providers.

- Customers: Automotive, construction, healthcare, agriculture, and consumer goods companies.

🚚 Leadership Insight: Collaboration across this chain requires logistics partners who can handle complexity, scale, and reliability—exactly where ABCC India Project Cargo Corporation plays a vital role in India’s growth story.

🔮 Future of Manufacturing and Production Structure

The industry is entering a new era defined by:

- Digital Plants (Industry 4.0): Smart sensors, automation, and AI-driven analytics.

- Regionalization: Diversifying supply chains closer to markets post-pandemic.

- Biotechnology Integration: Merging chemical processes with bio-based solutions.

- Advanced Materials: Nanomaterials, composites, and high-performance polymers.

📊 Leadership Insight: Business leaders must embrace digital and biological convergence to stay competitive in the next decade.

🏭 Chemical Industry Evolution: Local (India) vs Global 🌍

| 🏷️ Category | 🇮🇳 India (Local Evolution) | 🌍 Global (World Evolution) |

|---|---|---|

| ⏳ Origins | 1900s – Small-scale fertilizer & dye units | 18th century – Britain industrial revolution, sulfuric acid, soda ash |

| 🏭 Early Growth | 1940s–60s – Public sector dominance (Hindustan Insecticides, Indian Petrochemicals) | 19th century – Germany & USA lead with petrochemicals, dyes, pharma |

| 🚀 Expansion Phase | 1970s–90s – Large-scale PSUs + private players (Reliance, Tata Chemicals) | 20th century – US petrochemicals, Japan’s specialty chemicals |

| 🌱 Liberalization/Shift | 1991 onwards – FDI inflows, private-sector boom, export focus | Global diversification – China emerging, EU advancing sustainability |

| 📈 Present | 4th largest producer of chemicals globally; strong in agrochemicals, dyes, pharma | Global market leaders in petrochemicals, specialty, advanced materials |

| 🔮 Future Trends | India: Make-in-India, bio-based feedstocks, digitalization | Global: Green chemistry, circular economy, AI-driven smart plants |

💡 Leadership Insights

- India: Moving from a cost-based hub to an innovation and sustainability-driven hub.

- Global: Leading with R&D, green chemistry, and advanced materials.

- Both: Facing the challenge of balancing growth, environment, and digital transformation.

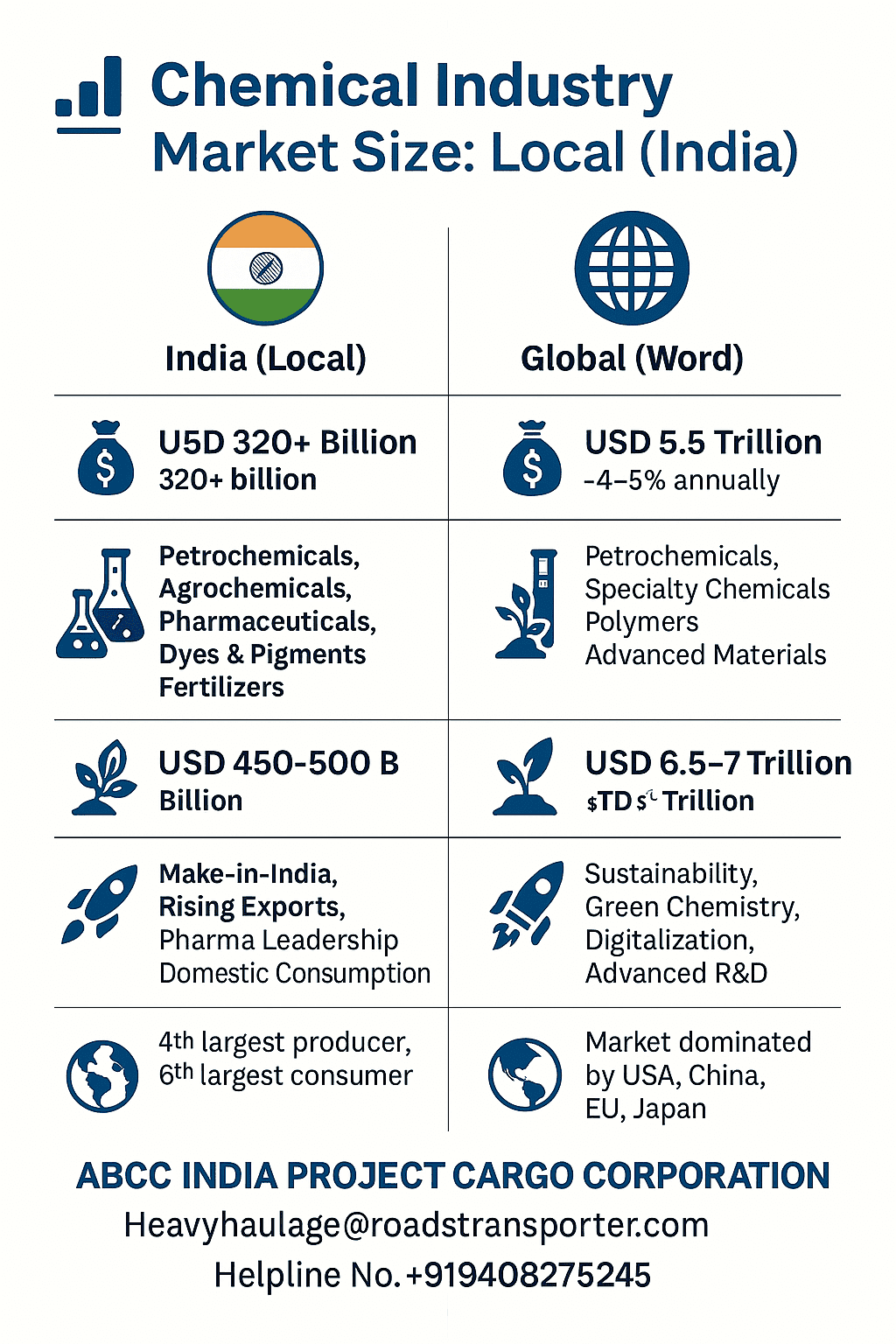

📊 Chemical Industry Market Size: Local (India) & Global 🌍

| 🏷️ Category | 🇮🇳 India (Local) | 🌍 Global (World) |

|---|---|---|

| 💰 Current Market Size (2025 est.) | USD 320+ Billion | USD 5.5 Trillion |

| 📈 CAGR Growth Rate | ~8–10% annually | ~4–5% annually |

| 🧪 Major Segments | Petrochemicals, Agrochemicals, Pharmaceuticals, Dyes & Pigments, Fertilizers | Petrochemicals, Specialty Chemicals, Polymers, Advanced Materials |

| 🌱 Future Projections (2030) | USD 450–500 Billion | USD 6.5–7 Trillion |

| 🚀 Growth Drivers | Make-in-India, Rising Exports, Pharma Leadership, Domestic Consumption | Sustainability, Green Chemistry, Digitalization, Advanced R&D |

| 🌍 Global Position | 4th largest producer, 6th largest consumer | Market dominated by USA, China, EU, Japan |

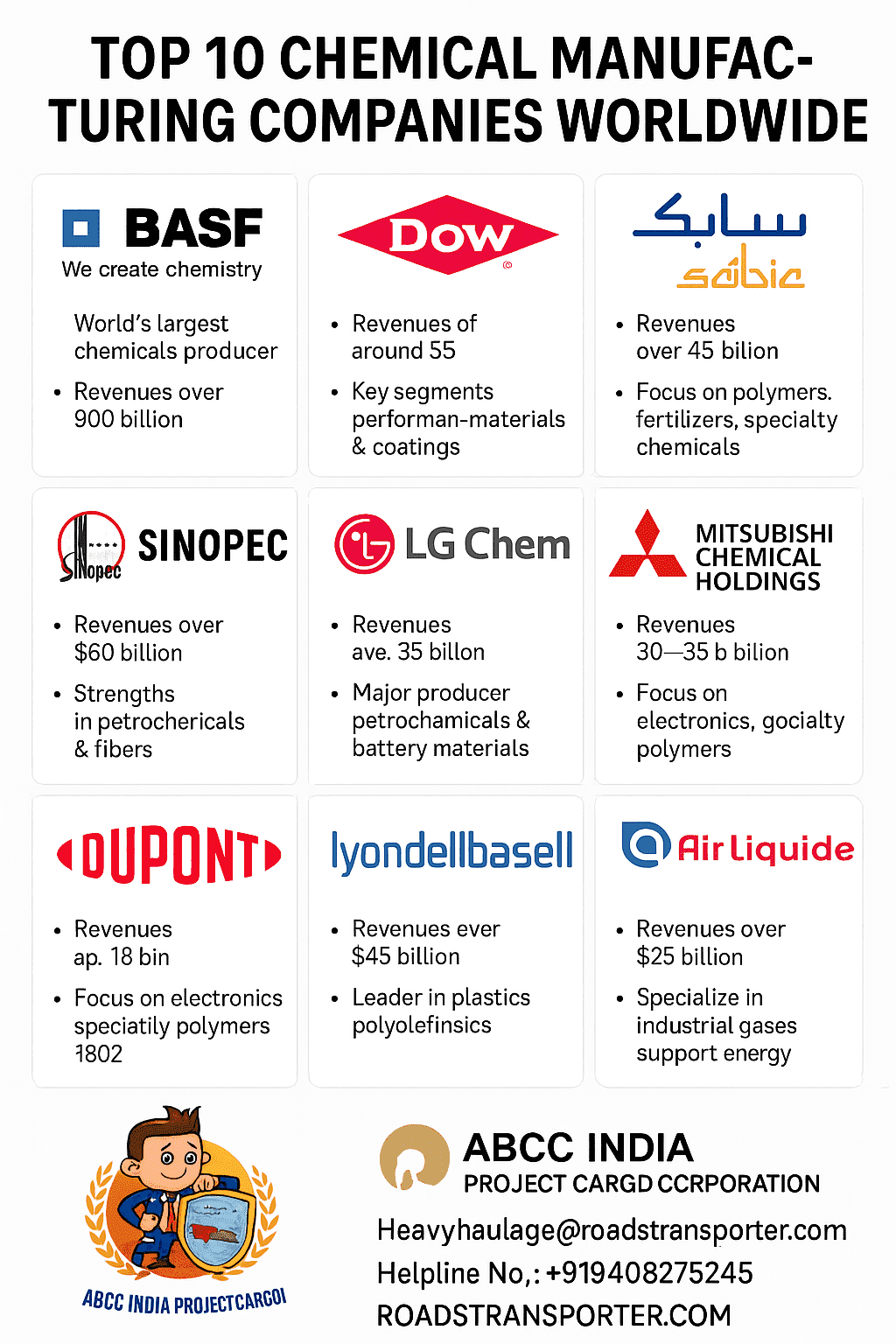

🌍 Top 10 Chemical Manufacturing Companies Worldwide

🏭 1. BASF SE (Germany)

BASF, headquartered in Ludwigshafen, Germany, is the world’s largest chemical company. Established in 1865, BASF has grown into a global leader spanning six segments: chemicals, materials, industrial solutions, surface technologies, nutrition & care, and agricultural solutions. Its integrated “Verbund” production system is a hallmark of operational excellence, allowing BASF to optimize resources, reduce costs, and maximize innovation.

Market Leadership: BASF maintains global dominance with revenues exceeding USD 90 billion annually. Its products range from petrochemicals and polymers to agricultural chemicals, nutrition, and coatings.

Innovation: The company invests heavily in R&D, with dedicated innovation hubs in Europe, North America, and Asia. Focus areas include climate-smart agriculture, lightweight automotive materials, and green chemistry.

Sustainability: BASF has committed to becoming carbon neutral by 2050. It leads in recycling plastics, developing renewable feedstocks, and digitalizing supply chains for efficiency.

Future Outlook: With its diversified portfolio and global presence, BASF is positioning itself as the pioneer of sustainable chemistry. Its leadership lesson: scale and integration matter, but sustainability is the future currency of the chemical industry.

⚙️ 2. Dow Inc. (USA)

Founded in 1897, Dow is one of the world’s most recognized chemical giants, headquartered in Midland, Michigan. The company’s portfolio includes performance materials, coatings, packaging, and specialty plastics.

Market Position: Dow generates annual revenues of around USD 55–60 billion. Its core strength lies in advanced materials for packaging, infrastructure, and consumer care.

Innovation & Strategy: Dow emphasizes sustainable packaging solutions, circular economy models, and electrification materials for renewable energy systems. Its “Stop the Waste” initiative focuses on global plastic recycling.

Leadership & Vision: Dow champions inclusion and diversity, embedding ESG goals into its business strategy. It aims for carbon neutrality by 2050 while leveraging AI-driven smart plants.

Future Outlook: By balancing sustainability, customer-centricity, and advanced R&D, Dow stands as a model of adapting legacy strengths to modern challenges.

🧪 3. Sinopec (China)

China Petroleum & Chemical Corporation (Sinopec) is Asia’s largest chemical manufacturer and one of the top three globally. Established in 2000 as a state-owned enterprise, Sinopec integrates energy, petrochemicals, and chemical production.

Market Strength: With revenues exceeding USD 60 billion from chemicals alone, Sinopec dominates in petrochemicals, synthetic fibers, and resins. Its scale supports China’s vast manufacturing demand.

Innovation Drive: Sinopec is investing in bio-based chemicals, hydrogen energy, and renewable polymers. It is actively diversifying to reduce dependence on crude oil.

Sustainability & Growth: The company faces global scrutiny over emissions but has committed to green development strategies under China’s “dual carbon” goals.

Future Outlook: Sinopec’s leadership shows the power of scale, state-backed growth, and strategic diversification to maintain dominance in a competitive market.

🌱 4. SABIC (Saudi Arabia)

Saudi Basic Industries Corporation (SABIC), founded in 1976 and headquartered in Riyadh, is a global leader in diversified chemicals.

Market Position: SABIC’s annual revenues exceed USD 45 billion, with products spanning petrochemicals, specialty plastics, fertilizers, and metals.

Innovation & Global Reach: SABIC operates in 50+ countries with manufacturing hubs in Saudi Arabia, Europe, the USA, and Asia. Its innovation strategy focuses on sustainable polymers, lightweight automotive solutions, and advanced packaging.

Sustainability: SABIC is a leader in chemical recycling and has pledged to move toward a circular economy.

Future Outlook: Backed by Saudi Aramco’s resources, SABIC is positioned as a key global influencer in the transition toward sustainable petrochemicals.

⚡ 5. LG Chem (South Korea)

LG Chem, founded in 1947, is South Korea’s largest chemical company and a major global supplier of advanced materials.

Market Position: LG Chem generates revenues of over USD 35 billion, with a strong presence in petrochemicals, advanced materials, and life sciences.

Innovation Leadership: The company is known for its leadership in battery materials, supporting the global EV revolution. It also produces cutting-edge plastics and IT materials.

Sustainability Commitment: LG Chem has pledged carbon neutrality by 2050 and invests in bio-based plastics and recycling technologies.

Future Outlook: With its focus on EV batteries and sustainable chemicals, LG Chem exemplifies how chemical companies can drive both industrial growth and green mobility.

🔬 6. Mitsubishi Chemical Holdings (Japan)

Mitsubishi Chemical, headquartered in Tokyo, is Japan’s largest chemical manufacturer, with operations spanning chemicals, healthcare, and advanced materials.

Market Position: Mitsubishi generates around USD 30–35 billion annually, with diversified interests in polymers, films, and healthcare solutions.

Innovation Strategy: Known for R&D leadership, the company focuses on high-performance polymers, biotech integration, and healthcare-related chemicals.

Sustainability: Mitsubishi aims for carbon neutrality by 2050 and is a pioneer in circular plastics and renewable feedstock chemistry.

Future Outlook: Mitsubishi’s leadership model proves the value of diversification and long-term innovation investment for staying resilient.

🏗️ 7. DuPont de Nemours, Inc. (USA)

DuPont, founded in 1802, has transformed from explosives manufacturing into a global leader in specialty chemicals and materials.

Market Leadership: DuPont generates around USD 13 billion annually from electronics, safety materials, and specialty polymers.

Innovation: Famous for brands like Kevlar, Tyvek, and Corian, DuPont leads in safety, construction, and electronics materials.

Sustainability: The company emphasizes renewable energy, clean water technologies, and sustainable materials.

Future Outlook: DuPont’s evolution highlights reinvention and adaptability as critical survival skills in the chemical industry.

🚀 8. LyondellBasell Industries (Netherlands/USA)

Headquartered in Houston and Rotterdam, LyondellBasell is a leader in plastics, chemicals, and refining.

Market Size: Annual revenues exceed USD 45 billion. Core strengths include polyolefins and polypropylene.

Innovation & Growth: The company invests in circular plastics and recycling solutions, partnering globally on waste-to-chemicals.

Sustainability: Carbon neutrality goals and innovation in sustainable polymers are key priorities.

Future Outlook: LyondellBasell proves that global scale and innovation in recycling can set industry benchmarks.

🌍 9. Air Liquide (France)

Air Liquide, established in 1902, specializes in industrial gases for industries including healthcare, electronics, and energy.

Market Position: With annual revenues exceeding USD 25 billion, Air Liquide is a leader in oxygen, hydrogen, and nitrogen supply.

Innovation: Air Liquide is at the forefront of hydrogen energy, supporting decarbonization efforts.

Future Outlook: Air Liquide demonstrates the growing role of industrial gases in energy transition and healthcare innovation.

🔮 10. Reliance Industries Ltd. (India)

Reliance Industries, headquartered in Mumbai, is India’s largest private-sector company with a strong chemical and petrochemical division.

Market Position: Reliance’s chemical business generates billions annually, with strengths in petrochemicals, polymers, and fibers.

Innovation & Growth: Reliance invests in bio-based chemicals, digitalization, and integration across refining-to-retail.

Sustainability: The company has pledged net carbon zero by 2035.

Future Outlook: Reliance is positioning India as a global hub for chemicals and energy transition, showcasing leadership from emerging markets.

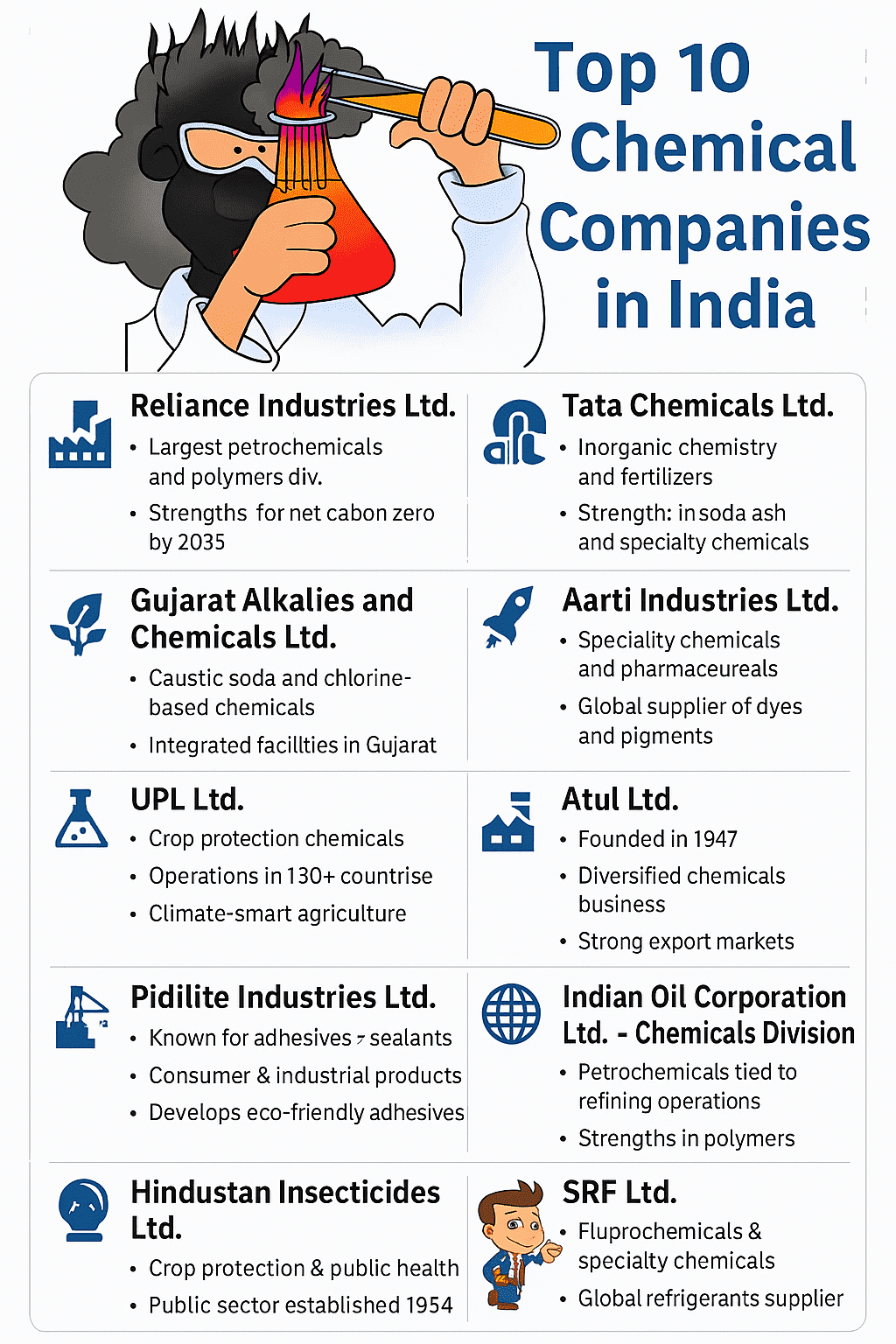

🇮🇳 Top 10 Chemical Manufacturing Companies in India

🏭 1. Reliance Industries Ltd. (Mumbai)

Reliance Industries is India’s largest private-sector conglomerate and a dominant force in petrochemicals and polymers. Its Jamnagar refinery complex is the world’s largest, seamlessly integrated with petrochemical production.

Market Position: Reliance commands leadership in polymers, fibers, and petrochemicals. It generates billions in revenue from its chemicals division, contributing significantly to India’s industrial growth.

Innovation & Growth: Heavy investments in bio-based chemicals, recycling, and advanced materials. Reliance is actively diversifying into renewable energy and green hydrogen, strengthening its long-term sustainability.

Future Outlook: With a pledge to achieve net carbon zero by 2035, Reliance is set to transform India into a global chemical hub.

⚙️ 2. Tata Chemicals Ltd. (Mumbai)

A member of the Tata Group, Tata Chemicals has a legacy in inorganic chemistry, fertilizers, and consumer products.

Strengths: Market leader in soda ash, sodium bicarbonate, and specialty chemicals. Operates globally with plants in India, Kenya, UK, and the USA.

Innovation: Focus on specialty nutrition, agri-solutions, and sustainable chemistry. Strong research in bio-based chemicals and green technologies.

Future Outlook: Tata Chemicals exemplifies responsible growth with sustainability and social responsibility at its core.

🌱 3. Gujarat Alkalies and Chemicals Ltd. (Vadodara)

Founded in 1973, GACL is one of India’s largest producers of caustic soda and chlorine-based chemicals.

Strengths: Operates multiple integrated facilities in Gujarat. Supplies to textiles, paper, alumina, and detergent industries.

Innovation: Adoption of renewable energy in its plants and investment in eco-friendly chlor-alkali processes.

Future Outlook: Positioned as a sustainable backbone of India’s manufacturing ecosystem.

🚀 4. Aarti Industries Ltd. (Mumbai)

Aarti Industries specializes in specialty chemicals, agrochemicals, and pharmaceuticals.

Market Position: Major supplier to global clients in dyes, pigments, and pharma intermediates. Exports contribute significantly to revenue.

Innovation: Focused R&D in specialty molecules, green chemistry, and customer-specific solutions.

Future Outlook: Aarti is transitioning from a cost-efficient supplier to a global innovation partner.

🔬 5. UPL Ltd. (Mumbai)

UPL is a global leader in crop protection chemicals and agro-solutions.

Strengths: Present in over 130 countries. Among the top 5 global agrochemical companies. Strong portfolio in herbicides, fungicides, and insecticides.

Sustainability: UPL drives climate-smart agriculture through its “OpenAg” platform, promoting sustainable farming worldwide.

Future Outlook: UPL highlights India’s role as a global food security enabler through chemical innovation.

🧪 6. Atul Ltd. (Valsad, Gujarat)

Founded in 1947, Atul Ltd. is a pioneer in India’s chemical industry.

Strengths: Diverse portfolio across agrochemicals, dyes, polymers, and pharmaceuticals. Operates globally in over 30 countries.

Innovation: Heavy R&D investments in sustainable dyes and pharma intermediates.

Future Outlook: Atul showcases the strength of diversification and global market linkages.

🏗️ 7. Pidilite Industries Ltd. (Mumbai)

Known for its household brands like Fevicol, Pidilite is also a major industrial chemicals player.

Strengths: Strong consumer and industrial adhesives, sealants, and construction chemicals portfolio.

Innovation: Continues to innovate in waterproofing solutions, eco-friendly adhesives, and consumer products.

Future Outlook: Pidilite’s model shows how consumer branding and industrial chemicals can go hand-in-hand.

🌍 8. Indian Oil Corporation Ltd. – Chemicals Division (New Delhi)

IOC, India’s largest PSU, is also a key player in petrochemicals.

Strengths: Operates naphtha and polymer plants integrated with refineries. Produces polypropylene, MEG, and LAB.

Sustainability: Expanding into green fuels and bio-based chemicals under India’s energy transition goals.

Future Outlook: IOC demonstrates public-sector leadership in integrating energy and chemicals.

⚡ 9. Hindustan Insecticides Ltd. (New Delhi)

Established in 1954, HIL is India’s oldest agrochemical PSU.

Strengths: Specializes in crop protection chemicals, pesticides, and agro-solutions. Supplies to both Indian farmers and global markets.

Future Outlook: HIL remains central to India’s agricultural productivity and rural development.

🔮 10. SRF Ltd. (Gurgaon)

SRF is a leading manufacturer of fluorochemicals, specialty chemicals, and packaging films.

Strengths: Supplies refrigerants, agrochemical intermediates, and industrial chemicals worldwide.

Innovation: Known for R&D in high-performance materials and advanced fluorochemicals.

Future Outlook: SRF is India’s rising star in global specialty chemicals.

🏭 Best Era for Chemical Industry (When and Why)

| 🏷️ Era | 📅 Timeframe | 🔑 Key Features | ⭐ Why Important |

|---|---|---|---|

| ⏳ Birth Era | 18th–19th Century | – Sulfuric acid, soda ash, synthetic dyes – Start of fertilizer production – Foundation of industrial chemistry | Proved chemistry’s industrial potential and economic value |

| ⚙️ Golden Era | 20th Century (1900s–1970s) | – Petrochemicals, plastics, fertilizers, pharma – Haber-Bosch process revolutionized agriculture – Global corporations like BASF, Dow, DuPont | Known as the Golden Era due to scale, global expansion, and mass industrial growth |

| 🌱 Transformation Era | 21st Century (2000s–Present) | – Green chemistry, circular economy – AI & digital plants – Bio-based feedstocks, sustainability goals | Era of responsibility and reinvention, balancing profit with planet |

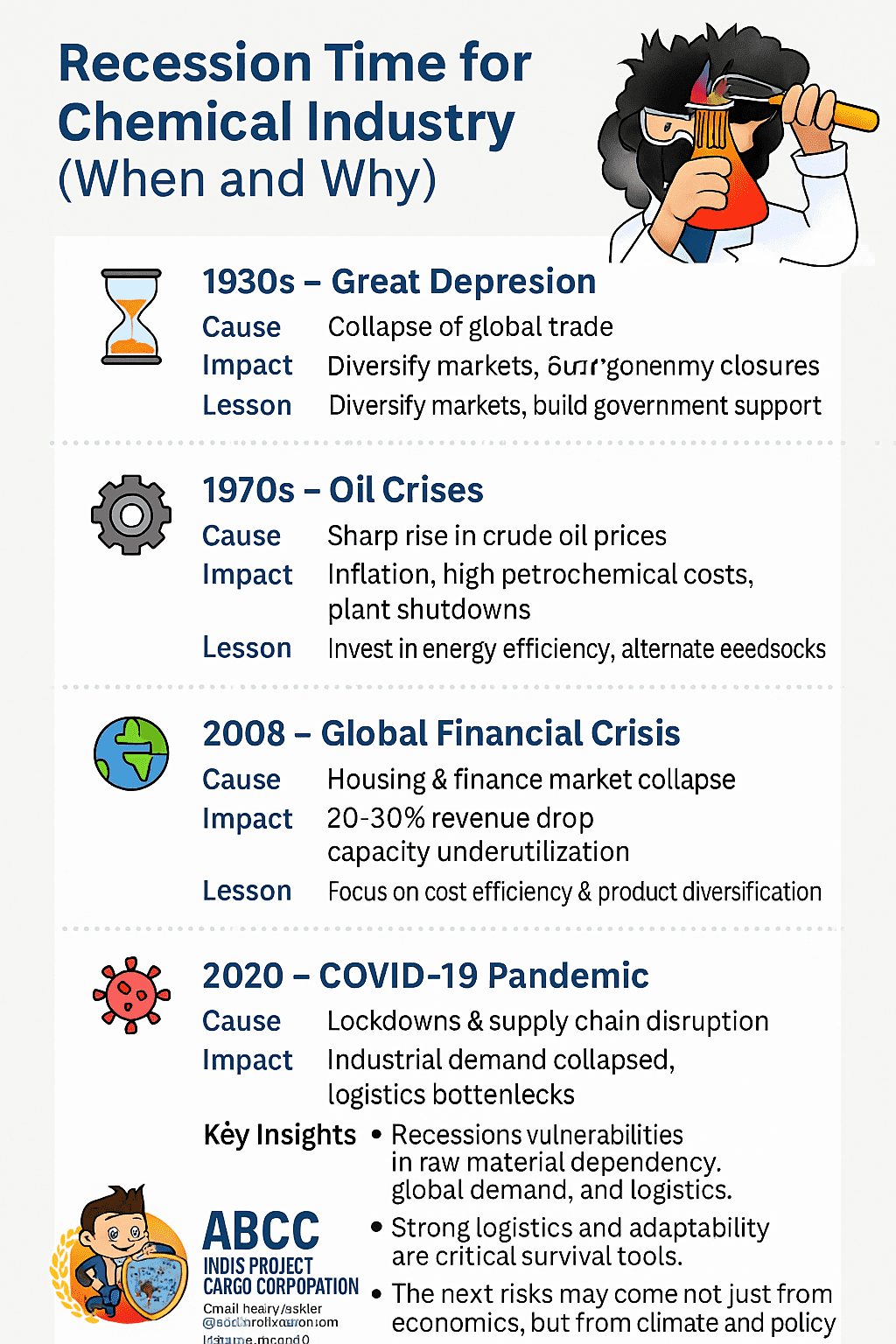

📉 Recession Time for Chemical Industry

| 📅 Period | 🛑 Cause | ⚡ Impact | 🔑 Lessons |

|---|---|---|---|

| ⏳ 1930s – Great Depression | Collapse of global trade | Fertilizer & dye shortages, company closures | Diversify markets, build government support |

| ⚙️ 1970s – Oil Crises | Sharp rise in crude oil prices | Inflation, high petrochemical costs, plant shutdowns | Invest in energy efficiency, alternate feedstocks |

| 🌍 2008 – Global Financial Crisis | Housing & finance market collapse | 20–30% revenue drop, capacity underutilization | Focus on cost efficiency & product diversification |

| 🦠 2020 – COVID-19 Pandemic | Lockdowns & supply chain disruption | Industrial demand collapsed, logistics bottlenecks | Build resilient supply chains, flexible operations |

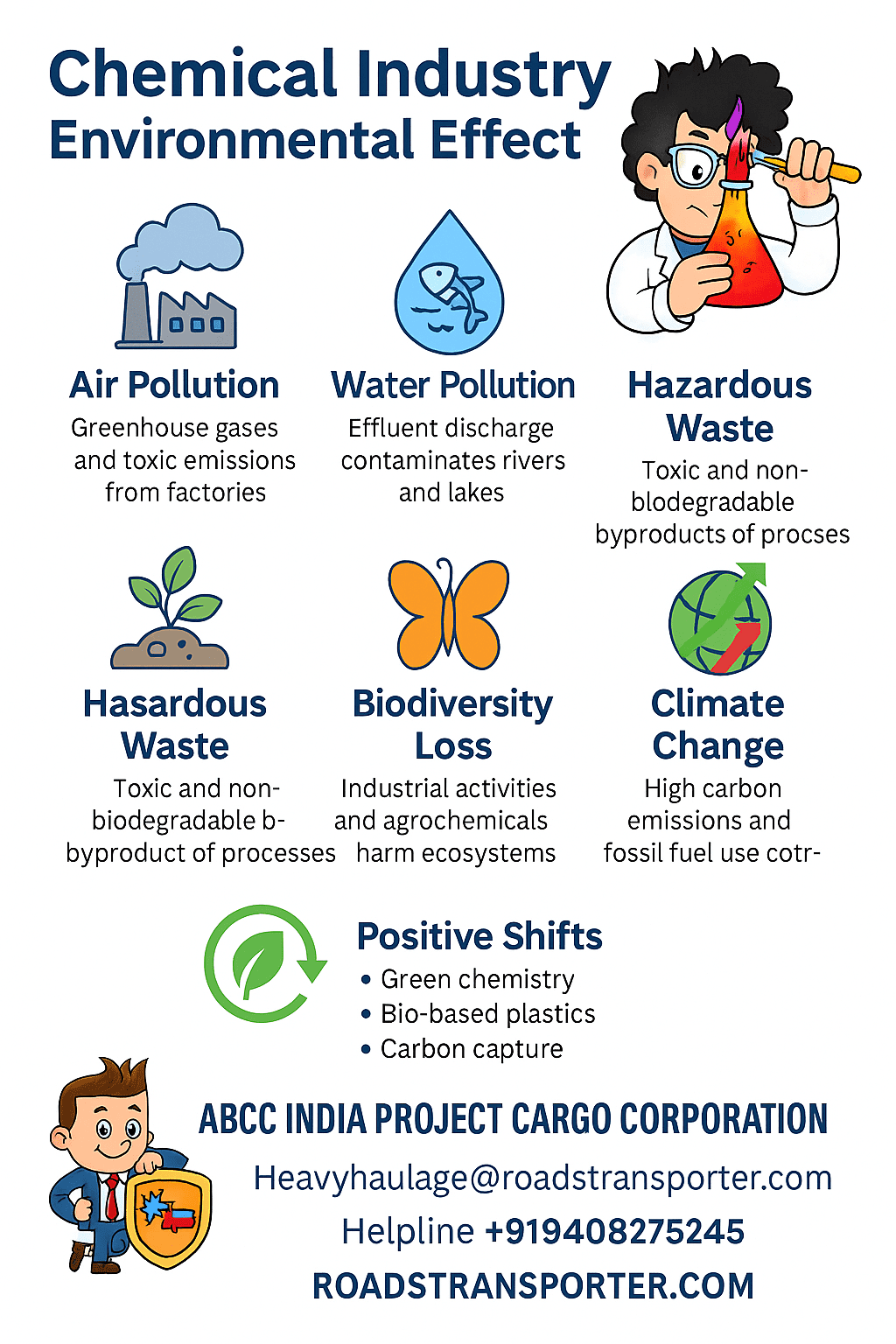

🌱 Chemical Industry Environmental Effect

The chemical industry has played a defining role in shaping modern civilization—fueling agriculture, healthcare, construction, and consumer goods. But alongside these achievements, the sector has left a deep environmental footprint. Understanding these effects helps leaders chart a future where industrial growth and environmental sustainability coexist.

🌍 Air Pollution

- Impact: Emissions of greenhouse gases (CO₂, methane, nitrous oxide), toxic fumes (SO₂, NOx), and particulate matter from chemical plants.

- Effect: Contributes to climate change, smog, and respiratory illnesses.

- Leadership Insight: Transition to clean fuels, renewable energy, and emission-control systems is crucial.

💧 Water Pollution

- Impact: Effluents discharged into rivers and lakes carry heavy metals, acids, and organic compounds.

- Effect: Water contamination harms aquatic ecosystems, biodiversity, and drinking water quality.

- Leadership Insight: Companies must embrace zero-liquid discharge (ZLD) systems and stricter wastewater management.

🏭 Soil Contamination

- Impact: Hazardous waste, pesticide residues, and chemical spills degrade soil fertility.

- Effect: Reduces agricultural productivity, harms microorganisms, and contaminates food chains.

- Leadership Insight: Adoption of eco-friendly agrochemicals and responsible waste handling is a must.

🛢️ Hazardous Waste

- Impact: Solid waste from chemical processes often contains toxic and non-biodegradable substances.

- Effect: Long-term environmental hazards, leaching into soil and groundwater.

- Leadership Insight: Circular economy practices like recycling and resource recovery can reduce the burden.

🐠 Biodiversity Loss

- Impact: Overuse of agrochemicals and industrial discharge damages ecosystems and species diversity.

- Effect: Decline of pollinators, soil organisms, and aquatic life.

- Leadership Insight: Leaders must promote integrated pest management (IPM) and sustainable farming.

⚡ Climate Change Contribution

- Impact: The chemical industry is one of the largest industrial energy consumers.

- Effect: Directly linked to global warming through emissions and fossil-fuel dependency.

- Leadership Insight: Decarbonization strategies—green hydrogen, bio-based feedstocks, and renewable energy—are the way forward.

📊 Positive Shifts Emerging

- Adoption of green chemistry principles

- Growing investment in carbon capture and utilization (CCU)

- Global moves towards bio-based and biodegradable plastics

- Regulatory frameworks pushing cleaner production standards

🔮 The Way Forward

- Innovation: Design products and processes that minimize waste.

- Collaboration: Partner with governments, NGOs, and communities.

- Responsibility: Ensure compliance with global sustainability standards (UN SDGs, ESG frameworks).

- Logistics Role: Efficient and clean logistics reduce emissions across supply chains.

🚚 ABCC INDIA PROJECT CARGO CORPORATION

At ABCC INDIA PROJECT CARGO CORPORATION, we understand that logistics is at the heart of reducing the chemical industry’s environmental impact. By providing multi-axle trailers, ODC cargo solutions, and containerized transport, we help industries minimize emissions, reduce bottlenecks, and promote sustainable operations.

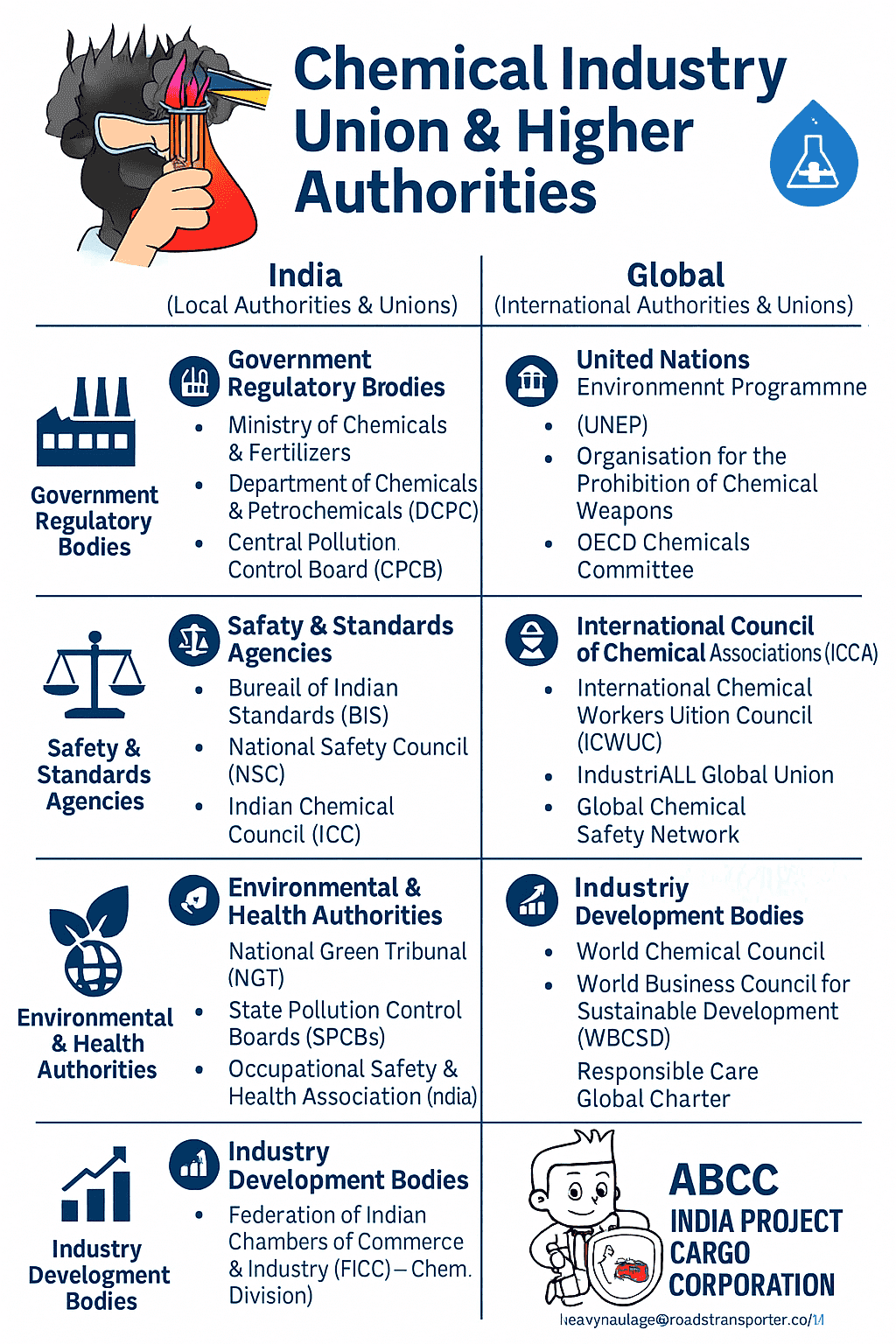

🏛️ Chemical Industry Union & Higher Authorities – Local (India) & Global

| 🏷️ Category | 🇮🇳 India (Local Authorities & Unions) | 🌍 Global (International Authorities & Unions) |

|---|---|---|

| 🏭 Government Regulatory Bodies | – Ministry of Chemicals & Fertilizers – Department of Chemicals & Petrochemicals (DCPC) – Central Pollution Control Board (CPCB) | – United Nations Environment Programme (UNEP) – Organisation for the Prohibition of Chemical Weapons (OPCW) – OECD Chemicals Committee |

| ⚖️ Safety & Standards Agencies | – Bureau of Indian Standards (BIS) – National Safety Council (NSC) – Indian Chemical Council (ICC) | – International Council of Chemical Associations (ICCA) – American Chemistry Council (ACC) – European Chemical Industry Council (Cefic) |

| 👷 Worker Unions & Trade Associations | – Indian Chemical Workers Union – All India Chemical Employees Federation – Petroleum & Chemical Workers Federation of India | – International Chemical Workers Union Council (ICWUC) – IndustriALL Global Union – Global Chemical Safety Network |

| 🌱 Environmental & Health Authorities | – National Green Tribunal (NGT) – State Pollution Control Boards (SPCBs) – Occupational Safety & Health Association (India) | – World Health Organization (WHO – chemical safety programs) – International Labour Organization (ILO – chemical conventions) – Basel, Rotterdam & Stockholm Conventions (hazardous waste & chemicals) |

| 📊 Industry Development Bodies | – Federation of Indian Chambers of Commerce & Industry (FICCI – Chemical Division) – Confederation of Indian Industry (CII – Chemicals Sector) | – World Chemical Council – World Business Council for Sustainable Development (WBCSD) – Responsible Care Global Charter |

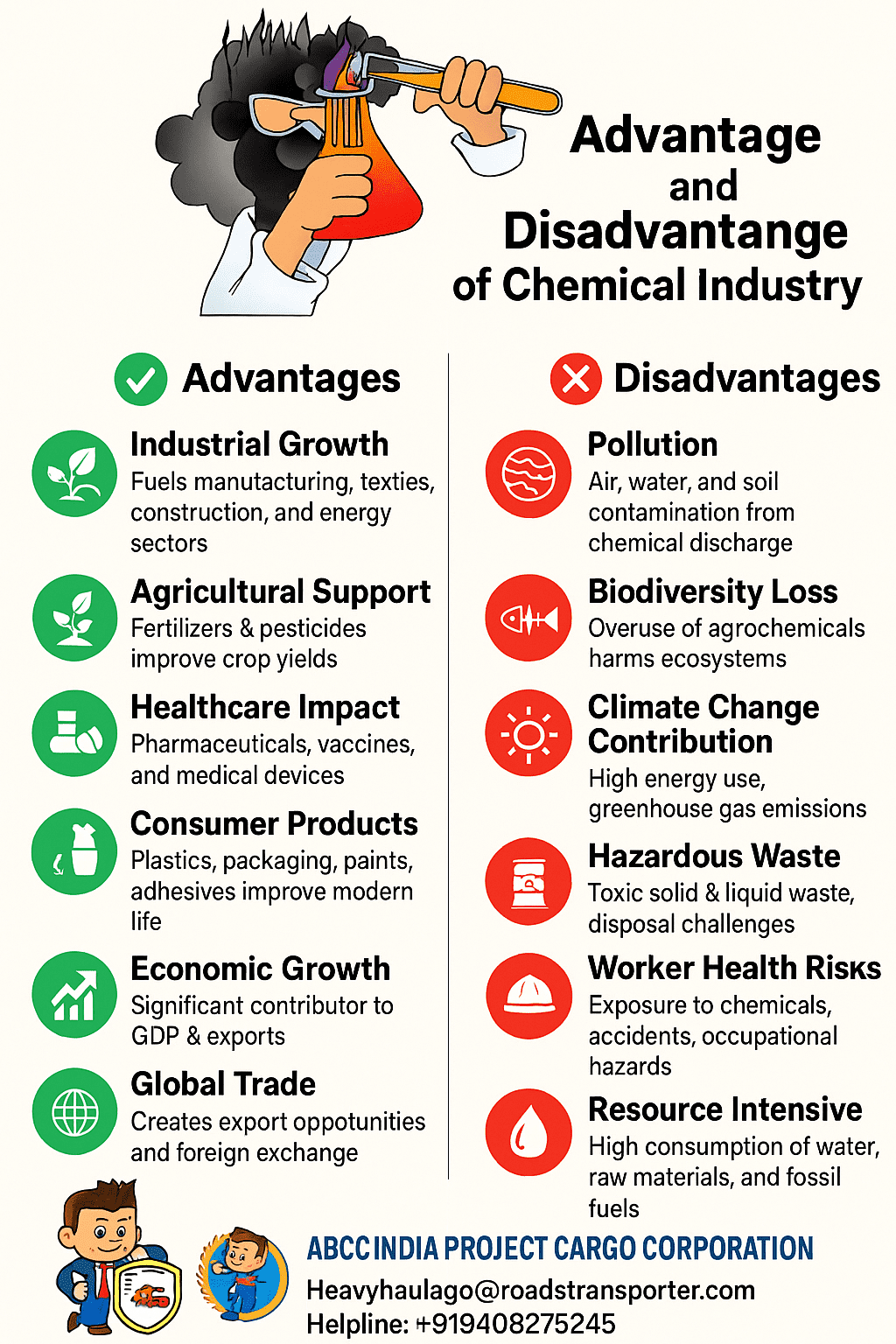

⚖️ Advantage and Disadvantage of Chemical Industry

| ✅ Advantages | ❌ Disadvantages |

|---|---|

| 🏭 Industrial Growth – Fuels manufacturing, textiles, construction, and energy sectors | 🌍 Pollution – Air, water, and soil contamination from chemical discharge |

| 🌱 Agricultural Support – Fertilizers & pesticides improve crop yields | 🐠 Biodiversity Loss – Overuse of agrochemicals harms ecosystems |

| 💊 Healthcare Impact – Pharmaceuticals, vaccines, and medical devices | ⚡ Climate Change Contribution – High energy use, greenhouse gas emissions |

| 🚗 Consumer Products – Plastics, packaging, paints, adhesives improve modern life | ☣️ Hazardous Waste – Toxic solid & liquid waste, disposal challenges |

| 📈 Economic Growth – Significant contributor to GDP & exports | 👷 Worker Health Risks – Exposure to chemicals, accidents, occupational hazards |

| 🌍 Global Trade – Creates export opportunities and foreign exchange | 💧 Resource Intensive – High consumption of water, raw materials, and fossil fuels |

| 🔬 Innovation Driver – Fuels R&D in green chemistry, materials, and clean tech | ⚖️ Regulatory Challenges – Constant compliance with safety & environmental laws |

⚖️ Legal & Compliance Framework for Chemical Industry

| 🏷️ Category | 🇮🇳 Local (India) | 🌍 Global (International) |

|---|---|---|

| 🏭 Primary Regulation | – Ministry of Chemicals & Fertilizers – Department of Chemicals & Petrochemicals (DCPC) | – United Nations Environment Programme (UNEP) – OECD Chemical Safety & Pesticides Programme |

| ⚖️ Environmental Laws | – Environment Protection Act, 1986 – Water Act, 1974 – Air Act, 1981 | – Basel Convention (hazardous waste) – Stockholm Convention (POPs) – Rotterdam Convention (chemicals & pesticides in trade) |

| 🧪 Chemical Safety & Handling | – Factories Act, 1948 – Manufacture, Storage & Import of Hazardous Chemicals Rules, 1989 – Chemical Accidents (Emergency Planning, Preparedness, and Response) Rules, 1996 | – Globally Harmonized System (GHS) for classification & labeling – REACH Regulation (EU) – Toxic Substances Control Act (USA) |

| 🌱 Worker Safety & Health | – Occupational Safety, Health & Working Conditions Code (OSHWC), 2020 – National Green Tribunal (NGT) oversight | – ILO Conventions on chemical safety – WHO International Programme on Chemical Safety (IPCS) |

| 📊 Industry Standards & Guidelines | – Bureau of Indian Standards (BIS) – Indian Chemical Council (ICC – Responsible Care) | – International Council of Chemical Associations (ICCA) – American Chemistry Council (ACC) – European Chemical Industry Council (Cefic) |

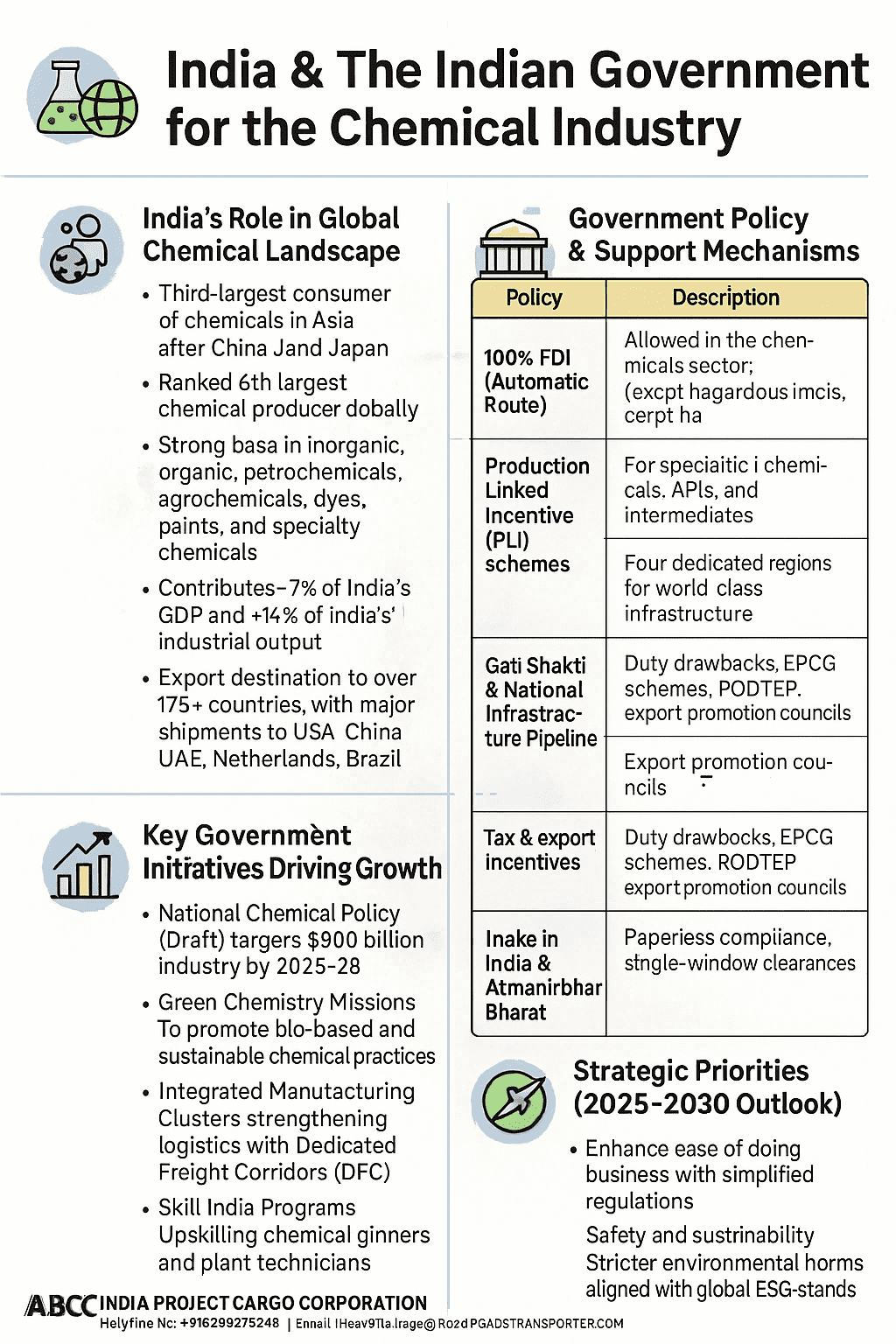

🏛️ India & The Indian Government for the Chemical Industry

🇮🇳 India’s Role in Global Chemical Landscape

- Third-largest consumer of chemicals in Asia after China and Japan.

- Ranked 6th largest chemical producer globally.

- Strong base in inorganic, organic, petrochemicals, agrochemicals, dyes, paints, and specialty chemicals.

- Contributes ~7% of India’s GDP and ~14% of India’s industrial output.

- Export destination for over 175+ countries, with major shipments to USA, China, UAE, Netherlands, and Brazil.

🏗️ Government Policy & Support Mechanisms

- 100% FDI (Automatic Route): Allowed in the chemicals sector (except hazardous chemicals).

- Production Linked Incentive (PLI) schemes: For specialty chemicals, APIs, and intermediates.

- Petroleum, Chemicals & Petrochemicals Investment Regions (PCPIRs): Four dedicated regions (Andhra Pradesh, Gujarat, Odisha, Tamil Nadu) for world-class infrastructure.

- Gati Shakti & National Infrastructure Pipeline: Improving connectivity for ports, pipelines, multimodal transport.

- Tax & export incentives: Duty drawbacks, EPCG schemes, RODTEP, and export promotion councils.

- Make in India & Atmanirbhar Bharat: Encouraging domestic capacity and import substitution.

📈 Key Government Initiatives Driving Growth

- National Chemical Policy (Draft): Targets $300 billion industry by 2025–28.

- Green Chemistry Missions: To promote bio-based and sustainable chemical practices.

- Integrated Manufacturing Clusters: Strengthening logistics with Dedicated Freight Corridors (DFC).

- Skill India Programs: Upskilling chemical engineers and plant technicians.

- Digital India push: Paperless compliance, single-window clearances.

🧭 Strategic Priorities (2025–2030 Outlook)

- Enhance ease of doing business with simplified regulations.

- Safety & sustainability: Stricter environmental norms aligned with global ESG standards.

- Expand PCPIRs into global hubs with mega-projects for petrochemicals and downstream units.

- Support export competitiveness through FTAs, logistics efficiency, and tax rationalization.

- Promote R&D in specialty chemicals, electronic chemicals, EV battery materials, and biopolymers.

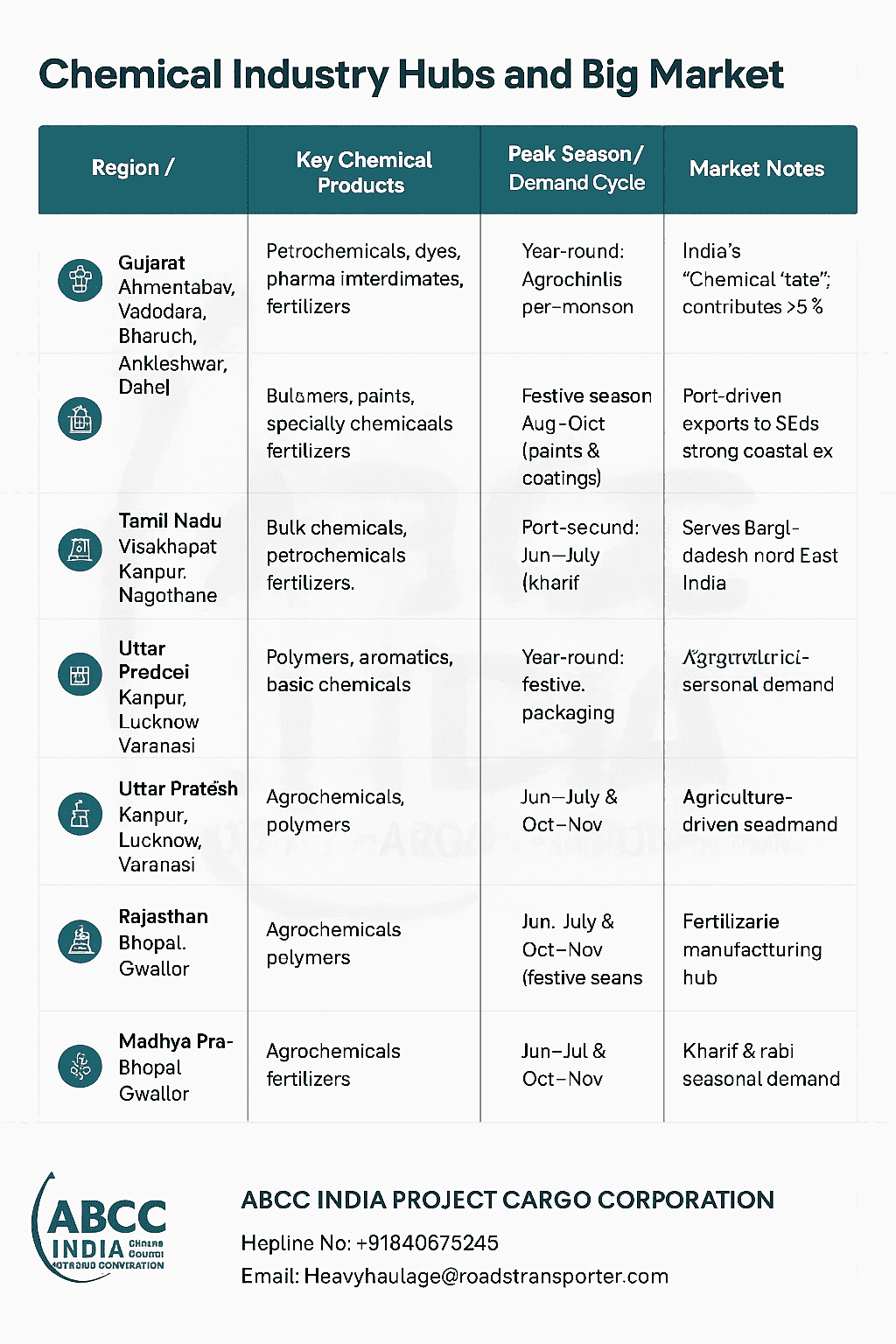

Chemical Industry Hubs and Big Market in India

| Region / State / City | Key Chemical Products | Peak Season / Demand Cycle | Market Notes |

|---|---|---|---|

| Gujarat – Ahmedabad, Vadodara, Bharuch, Ankleshwar, Dahej | Petrochemicals, dyes, pharma intermediates, fertilizers | Year-round; agrochemicals peak Apr–Jun (pre-monsoon) | India’s “Chemical State”; contributes >60% of exports |

| Maharashtra – Mumbai, Thane, Raigad, Nagothane | Polymers, paints, specialty chemicals, plastics | Festive season Aug–Oct (paints & coatings) | Strong demand from auto, housing, pharma sectors |

| Tamil Nadu – Cuddalore, Chennai, Tuticorin | Fertilizers, petrochemicals, industrial gases | Jun–Jul & Oct–Nov (sowing cycles) | Port-driven exports to SE Asia & Sri Lanka |

| Andhra Pradesh – Visakhapatnam, Kakinada | Bulk chemicals, petrochemicals, fertilizers | Jun–Jul (kharif sowing) | PCPIR & SEZ-driven hub; strong coastal exports |

| Odisha – Paradip | Petrochemicals, fertilizers | Jun–Jul & Oct–Nov (fertilizer demand) | Refinery-linked hub; focus on eastern demand |

| West Bengal – Haldia | Polymers, aromatics, basic chemicals | Year-round; festive packaging demand | Serves Bangladesh & North-East India |

| Uttar Pradesh – Kanpur, Lucknow, Varanasi | Agrochemicals, fertilizers, leather chemicals | Jun–Jul & Oct–Nov (fertilizer demand) | Strong rural-driven chemical demand |

| Punjab & Haryana – Ludhiana, Panipat | Agrochemicals, polymers | Peaks in kharif & rabi sowing | Agriculture-driven seasonal demand |

| Rajasthan – Kota | Fertilizers (urea, DAP) | Jun–Jul & Oct–Nov (sowing seasons) | Fertilizer manufacturing hub |

| Madhya Pradesh – Bhopal, Gwalior | Agrochemicals, fertilizers | Kharif & rabi seasonal peaks | Central India distribution hub |

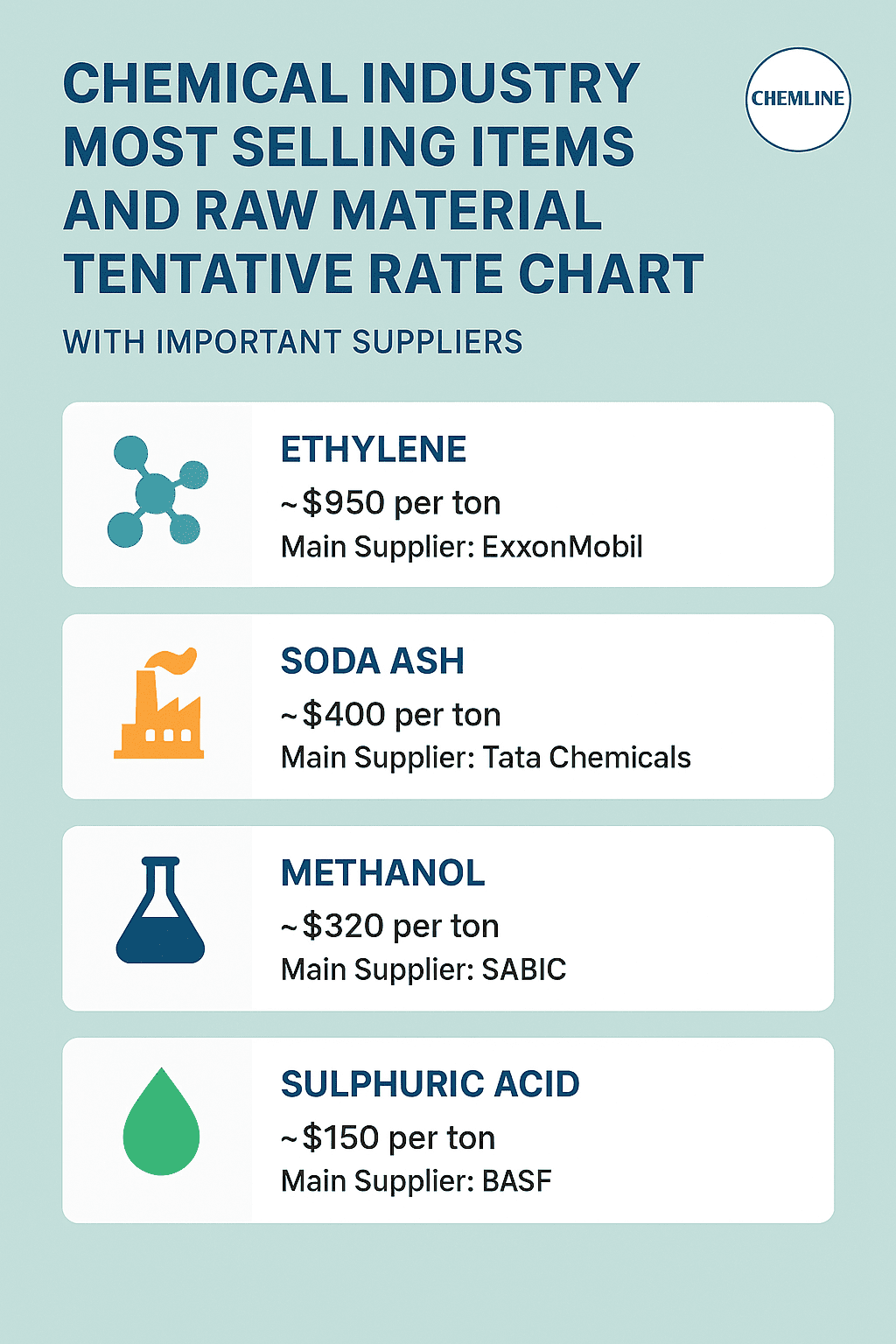

Chemical Industry – Most Selling Items, Raw Materials, Tentative Rates & Big Suppliers

| Item / Category | Key Raw Material Used | Tentative Rate (INR / Kg or Litre) | Major Indian Suppliers (Big Players) | Market Notes / Demand Driver |

|---|---|---|---|---|

| Caustic Soda (Solid/Flakes) | Salt, electricity | ₹35 – ₹45 / Kg | Gujarat Alkalies & Chemicals, Aditya Birla Chemicals | Used in textiles, paper, alumina, soap |

| Soda Ash (Light/Dense) | Limestone, salt | ₹28 – ₹38 / Kg | Tata Chemicals, GHCL Ltd | Glass, detergents, intermediates |

| Sulphuric Acid | Sulphur, oxygen, water | ₹8 – ₹12 / Kg | Hindustan Copper Ltd, Nirma Ltd | Fertilizers, dyes, steel pickling |

| Nitric Acid | Ammonia, oxygen | ₹25 – ₹35 / Kg | Rashtriya Chemicals & Fertilizers (RCF), Deepak Fertilisers | Fertilizers, nylon, pharma |

| Hydrochloric Acid | Salt + sulphuric acid | ₹5 – ₹8 / Kg | Gujarat Alkalies & Chemicals, Chemplast Sanmar | PVC, chlorides, water treatment |

| Chlorine Gas | Electrolysis of brine | ₹15 – ₹22 / Kg | DCM Shriram, Grasim Industries | PVC, disinfectants, textiles |

| Methanol | Natural gas, coal | ₹25 – ₹35 / Litre | Deepak Fertilisers, Assam Petrochemicals | Pharma, paints, adhesives, solvents |

| Acetone | Propylene | ₹60 – ₹80 / Kg | Deepak Phenolics, Hindustan Organics | Paints, coatings, adhesives, pharma |

| Benzene | Petroleum refining | ₹55 – ₹70 / Kg | Reliance Industries, BPCL | Styrene, nylon, detergents, dyes |

| Toluene | Petroleum refining | ₹60 – ₹75 / Kg | Reliance Industries, Indian Oil Corp (IOCL) | Paints, thinners, adhesives, pharma |

| Xylene (Mixed/Ortho/Para) | Crude oil fractions | ₹65 – ₹85 / Kg | Reliance Industries, HPCL | Polyester, paints, plastics |

| Ethanol (Industrial) | Molasses, biomass | ₹45 – ₹55 / Litre | Praj Industries, Balrampur Chini Mills | Pharma, beverages, biofuel blending |

| Urea (Fertilizer) | Ammonia, CO₂ | ₹6 – ₹8 / Kg | National Fertilizers Ltd, IFFCO | Major agricultural fertilizer |

| DAP (Diammonium Phosphate) | Ammonia, phosphoric acid | ₹22 – ₹28 / Kg | Coromandel International, RCF | High nutrient fertilizer |

| NPK Fertilizers | Nitrogen, phosphorus, potash | ₹25 – ₹32 / Kg | Zuari Agro Chemicals, Chambal Fertilisers | Balanced fertilizer blends |

| PVC Resin | Ethylene, chlorine | ₹85 – ₹100 / Kg | Reliance Industries, Finolex Industries | Pipes, profiles, cables, packaging |

| HDPE / LDPE | Ethylene | ₹95 – ₹120 / Kg | Reliance Industries, ONGC Petro Additions | Packaging, pipes, household plastics |

| Styrene Monomer | Benzene, ethylene | ₹95 – ₹115 / Kg | Reliance Industries, Supreme Petrochem | Polystyrene, ABS plastics, resins |

| Phosphoric Acid | Phosphate rock, sulphur | ₹55 – ₹70 / Kg | Paradeep Phosphates, Coromandel Intl. | Fertilizers, food additives, detergents |

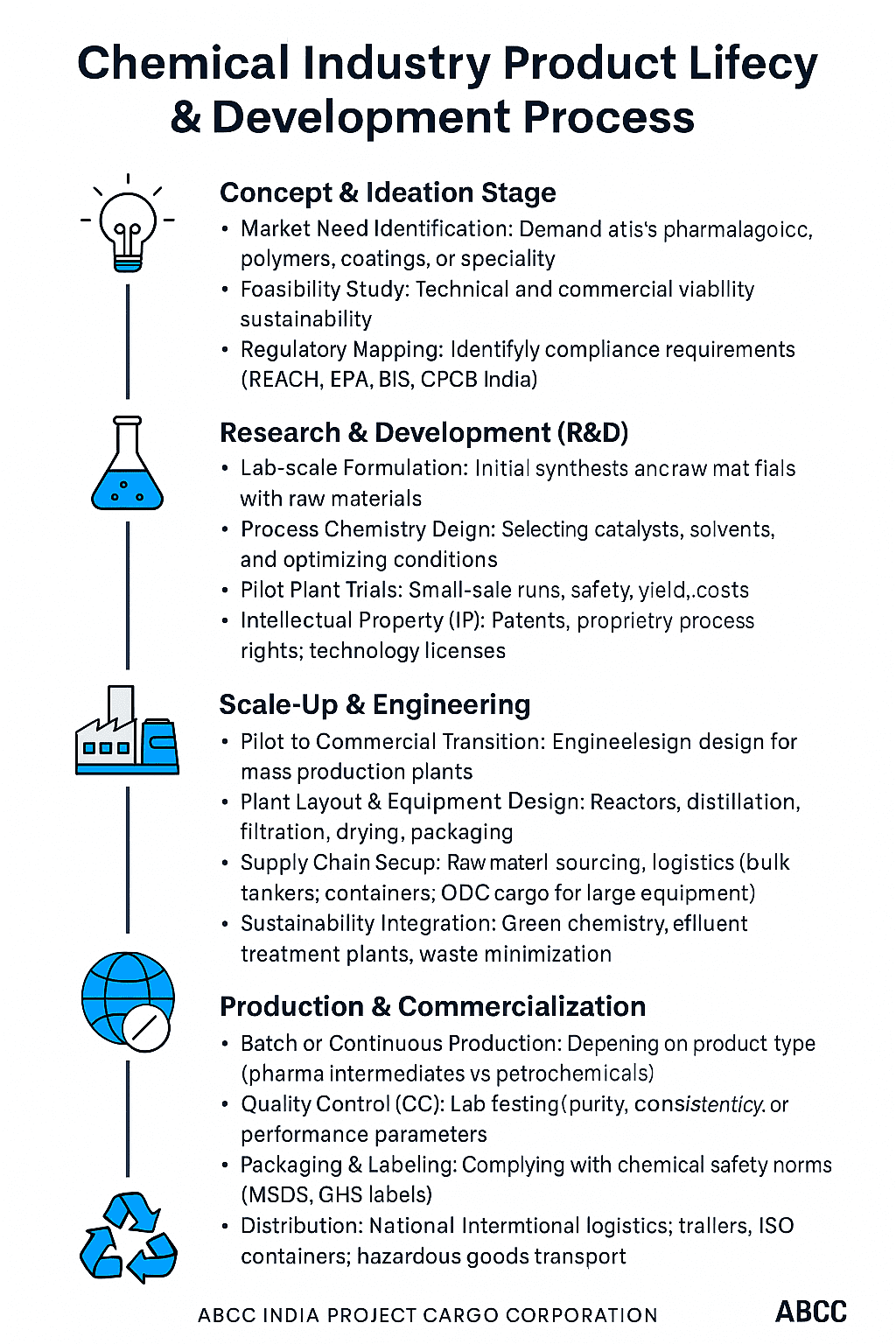

🔄 Chemical Industry Product Lifecycle & Development Process

1. 🏁 Concept & Ideation Stage

- Market Need Identification: Demand analysis in pharma, agrochemicals, polymers, coatings, or specialty sectors.

- Feasibility Study: Technical and commercial viability, sustainability assessments.

- Regulatory Mapping: Identify compliance requirements (REACH, EPA, BIS, CPCB in India).

2. ⚗️ Research & Development (R&D)

- Lab-scale Formulation: Initial synthesis and trials with raw materials.

- Process Chemistry Design: Selecting catalysts, solvents, and optimization conditions.

- Pilot Plant Trials: Small-scale runs for safety, yield, cost checks.

- Intellectual Property (IP): Patents, proprietary process rights, technology licenses.

3. 🏭 Scale-Up & Engineering

- Pilot to Commercial Transition: Engineering design for mass production plants.

- Plant Layout & Equipment Design: Reactors, distillation, filtration, drying, packaging.

- Supply Chain Setup: Raw material sourcing, logistics (bulk tankers, containers, ODC cargo for large equipment).

- Sustainability Integration: Green chemistry, effluent treatment plants (ETP), waste minimization.

4. 📦 Production & Commercialization

- Batch or Continuous Production: Depending on product type (pharma intermediates vs. petrochemicals).

- Quality Control (QC): Lab testing (purity, consistency, performance parameters).

- Packaging & Labeling: Complying with chemical safety norms (MSDS, GHS labels).

- Distribution: National and international logistics (trailers, ISO containers, hazardous goods transport).

5. 🌍 Market Expansion & Application Development

- End-User Integration: Tailoring formulations for customers (coatings, fertilizers, pharma APIs).

- Export Markets: Leveraging ports (Dahej, Tuticorin, Paradip) for global demand.

- Alliances: Tie-ups with downstream manufacturers for steady offtake.

6. ♻️ Maturity, Sustainability & Decline Phase

- Maturity Stage: Cost competitiveness, global pricing pressure.

- Innovation Renewal: Shift toward specialty or green chemicals for differentiation.

- Decline or Diversification: Phase-out due to obsolescence, regulations, or demand shift; move to substitutes.

- Circular Economy: Recycling, waste valorization, by-product utilization.

📌 Insights for 2025–2030

- R&D is shifting toward bio-based feedstocks (ethanol, lactic acid, biopolymers).

- Lifecycle success depends on logistics + compliance + technology adoption.

- Digital twins & AI being integrated into chemical process design for predictive safety & efficiency.

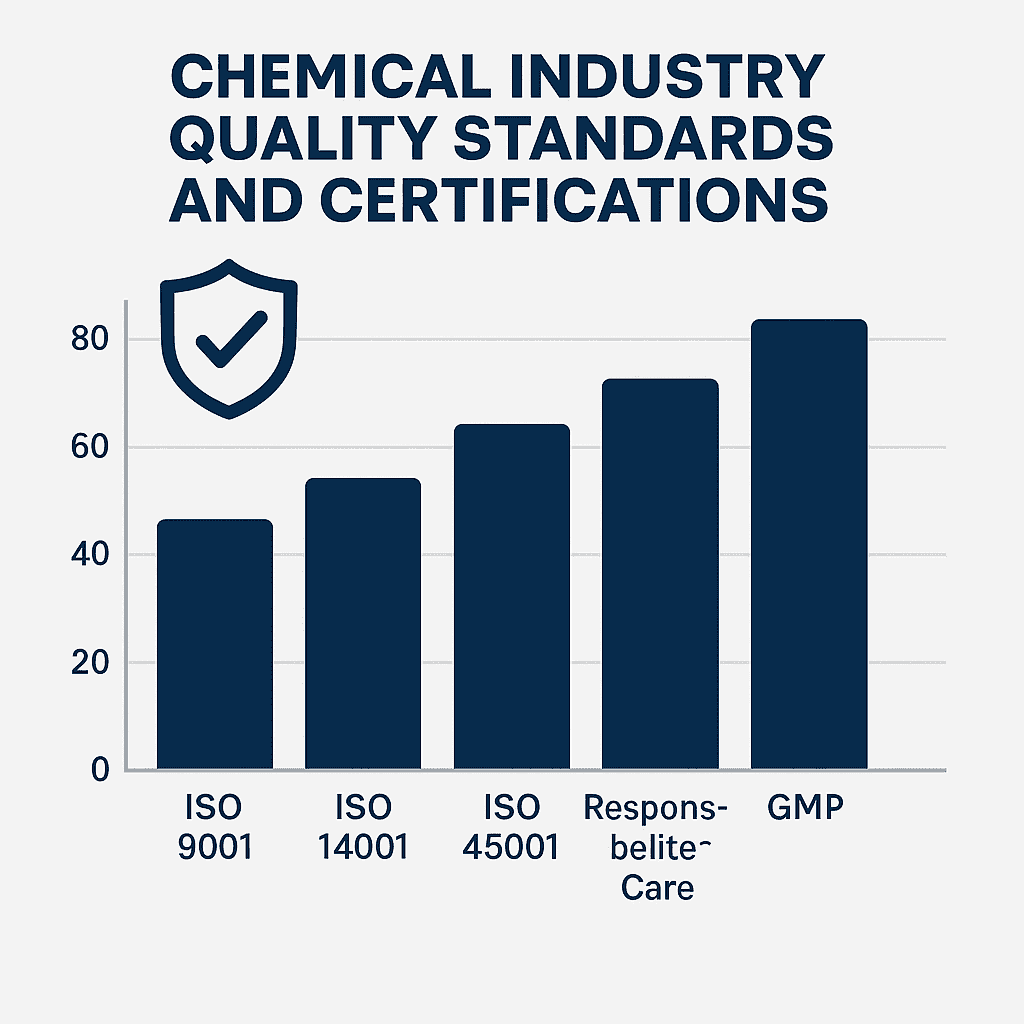

Chemical Industry – Quality Standards and Certifications

| Standard / Certification | Region / Authority | Purpose / Coverage | Industry Relevance |

|---|---|---|---|

| ISO 9001 (Quality Management) | International (ISO) | Consistent product quality, customer satisfaction | All chemical sectors |

| ISO 14001 (Environment) | International (ISO) | Eco-friendly and sustainable practices | Petrochemicals, agrochemicals, specialty |

| ISO 45001 (Health & Safety) | International (ISO) | Workplace safety management | Chemical plants, refineries, manufacturing |

| ISO 50001 (Energy Management) | International (ISO) | Efficient energy use, lower emissions | Energy-intensive chemical units |

| REACH Compliance | European Union | Safe use of chemicals for humans & environment | Exporters to EU markets |

| RoHS | European Union | Restriction of hazardous substances | Chemicals for electronics, coatings |

| BIS Certification | Bureau of Indian Standards (India) | Mandatory quality certification for selected chemicals | Fertilizers, paints, polymers |

| ISI Mark | Bureau of Indian Standards (India) | National quality symbol | Industrial & consumer chemicals |

| CPCB / SPCB Approvals | India (Central/State Pollution Control) | Environmental clearance for water, air, waste | All chemical industries |

| PESO Certification | India (Petroleum & Explosives Safety Org.) | Handling/storage approval for hazardous chemicals | Explosives, solvents, flammable chemicals |

| FSSAI | Food Safety & Standards Authority of India | Certification for food-grade chemicals & additives | Food, pharma, beverages |

| IBR | Indian Boiler Regulations | Safety for boiler treatment chemicals | Power plants, industrial boilers |

| NABL Accreditation | India (NABL under ISO/IEC 17025) | Testing & calibration lab approval | QC labs, R&D centers |

| GMP (Good Manufacturing Practices) | Global / India | Ensures safe, consistent production of pharma chemicals | Pharma & specialty chemicals |

| GLP (Good Laboratory Practices) | Global / India | Standard procedures for lab testing & safety | R&D, testing labs |

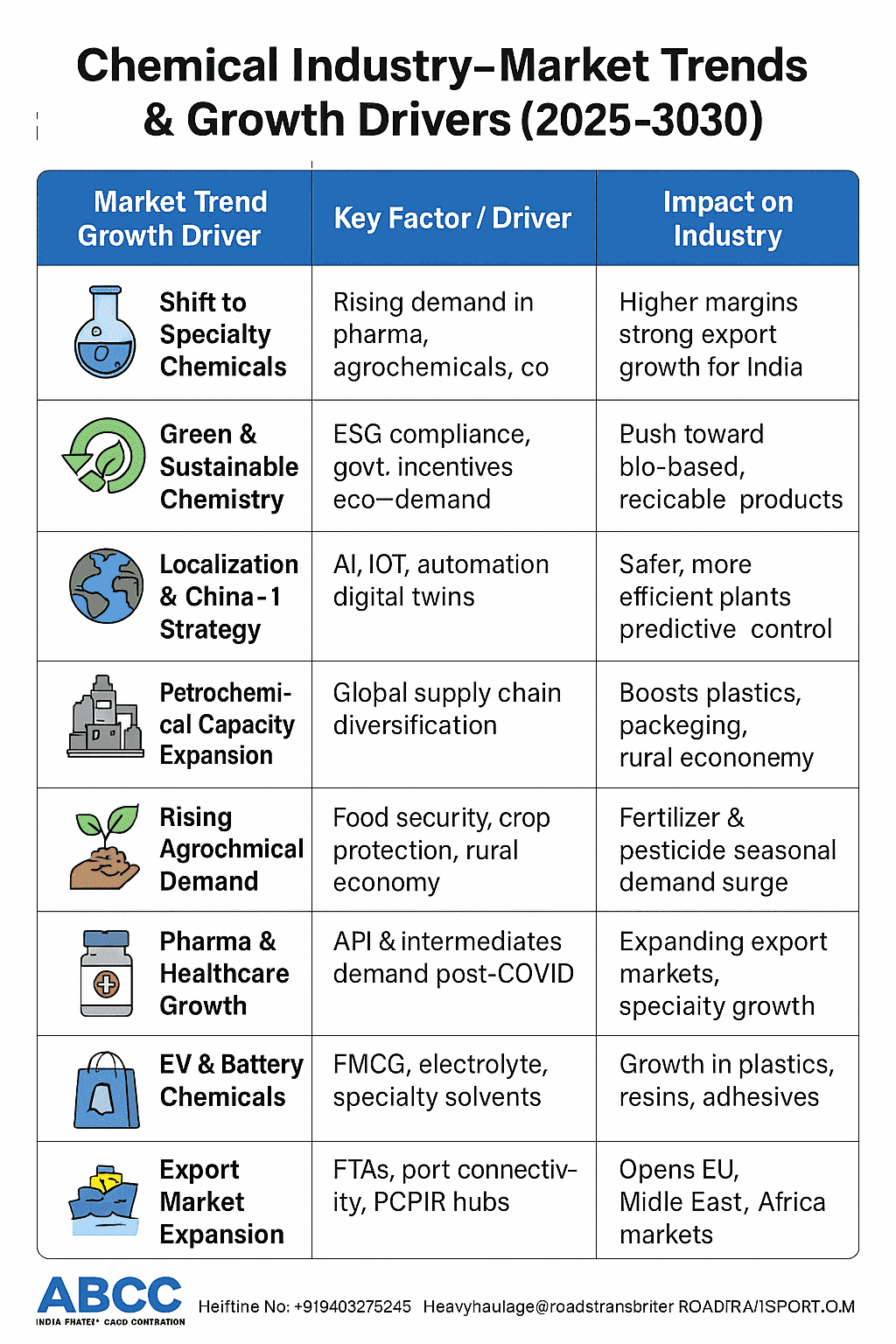

Chemical Industry – Market Trends & Growth Drivers

| Market Trend / Growth Driver | Key Factor / Driver | Impact on Industry |

|---|---|---|

| Shift to Specialty Chemicals | Rising demand in pharma, agrochemicals, coatings | Higher margins, strong export growth for India |

| Green & Sustainable Chemistry | ESG compliance, govt. incentives, eco-demand | Push toward bio-based, recyclable products |

| Digitalization & Industry 4.0 | AI, IoT, automation, digital twins | Safer, more efficient plants, predictive control |

| Localization & China+1 Strategy | Global supply chain diversification | India as alternative hub, Make in India boost |

| Petrochemical Capacity Expansion | New refinery-linked & cracker projects | Boosts plastics, packaging, infra materials |

| Rising Agrochemical Demand | Food security, crop protection, rural economy | Fertilizer & pesticide seasonal demand surge |

| Pharma & Healthcare Growth | API & intermediates demand post-COVID | Expanding export markets, specialty growth |

| EV & Battery Chemicals | Lithium, electrolyte, specialty solvents demand | New chemical markets for EVs & energy storage |

| Packaging & Consumer Goods | FMCG, e-commerce, urbanization | Growth in plastics, resins, adhesives |

| Export Market Expansion | FTAs, port connectivity, PCPIR hubs | Opens EU, Middle East, Africa markets |

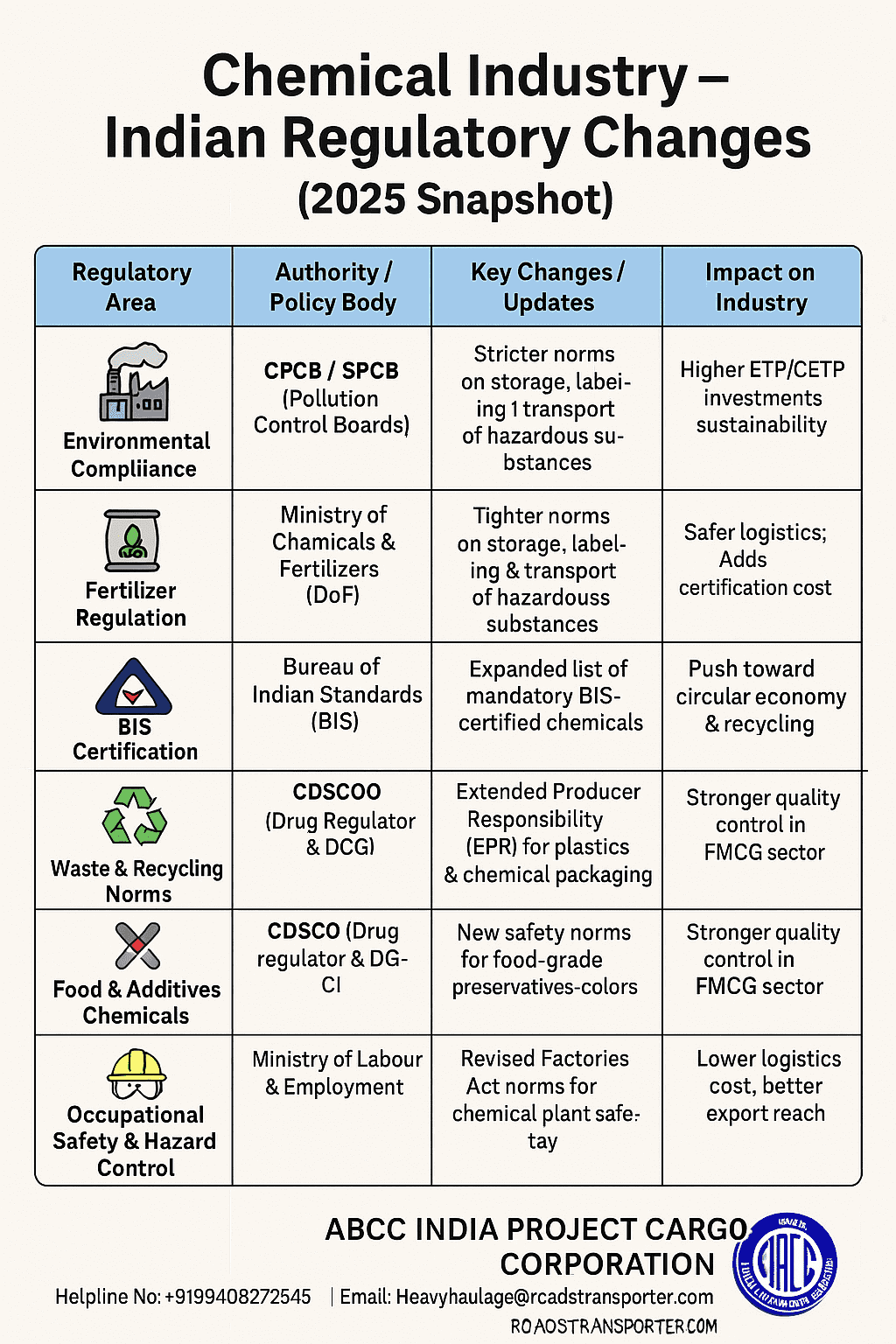

Chemical Industry – Indian Regulatory Changes

| Regulatory Area | Authority / Policy Body | Key Changes / Updates | Impact on Industry |

|---|---|---|---|

| Environmental Compliance | CPCB / SPCB (Pollution Control Boards) | Stricter emission norms for air & effluents; Zero Liquid Discharge push | Higher ETP/CETP investments, sustainability |

| Hazardous Chemical Handling | PESO (Petroleum & Explosives Safety Org.) | Tighter norms on storage, labeling & transport of hazardous substances | Safer logistics; compliance costs increase |

| Fertilizer Regulation | Ministry of Chemicals & Fertilizers (DoF) | Nutrient-Based Subsidy (NBS) scheme revamp; tracking via DBT (Direct Benefit Transfer) | Price rationalization; farmer affordability |

| BIS Certification | Bureau of Indian Standards (BIS) | Expanded list of mandatory BIS-certified chemicals | Ensures product quality; adds certification cost |

| Waste & Recycling Norms | MoEFCC (Environment Ministry) | Extended Producer Responsibility (EPR) for plastics & chemical packaging | Push toward circular economy & recycling |

| Pharma & Specialty Chemicals | CDSCO (Drug Regulator) & DCGI | Stricter GMP & GLP compliance for API/intermediates | Better export acceptance, higher compliance |

| Food & Additives Chemicals | FSSAI | New safety norms for food-grade preservatives, colors | Stronger quality control in FMCG sector |

| Occupational Safety & Hazard Control | Ministry of Labour & Employment | Revised Factories Act norms for chemical plants safety | Worker safety improved; operational upgrades |

| Export-Import Policy | DGFT (Directorate General of Foreign Trade) | Import restrictions on hazardous/bulk chemicals; new HS codes | Boost to domestic production capacity |

| Infrastructure & Logistics | Gati Shakti / PCPIR Policy | PCPIR policy revamp; port-led chemical cluster focus | Lower logistics cost, better export reach |

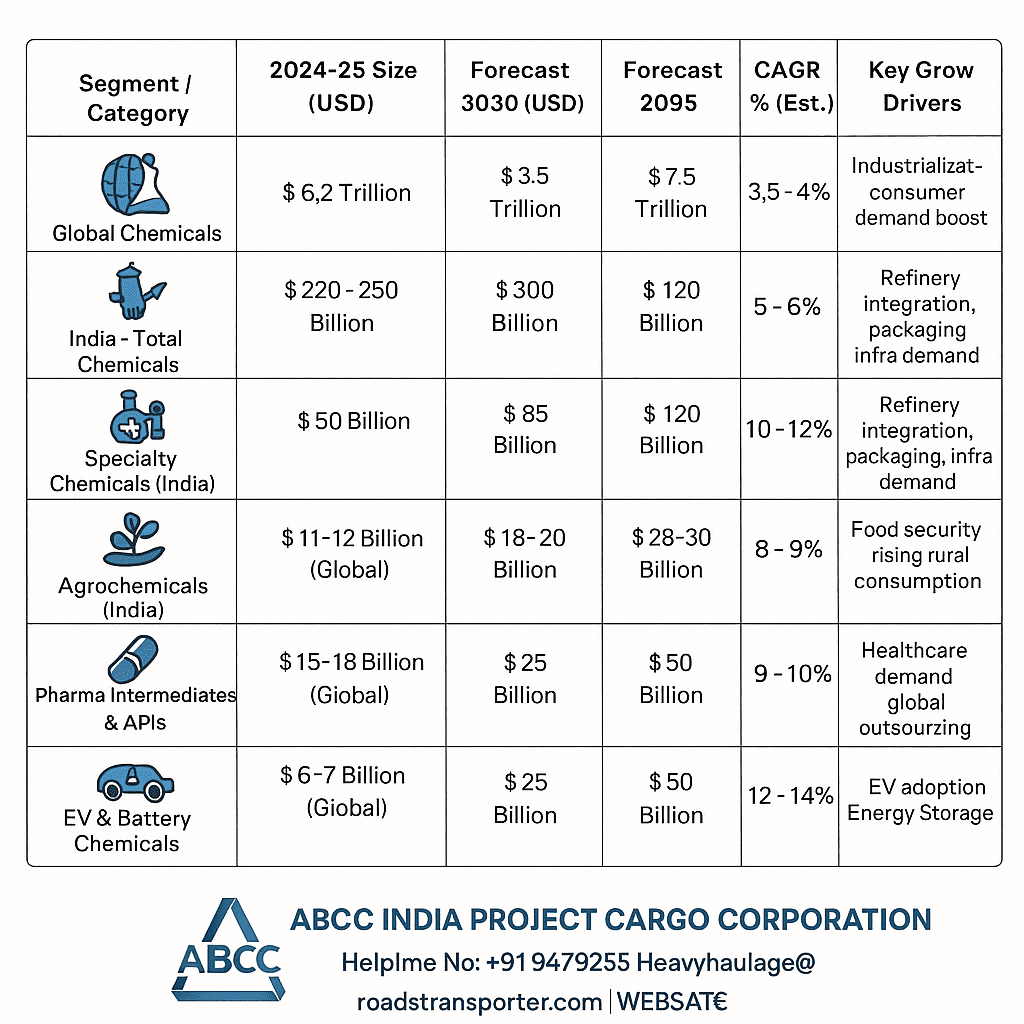

Chemical Industry – Industry Forecast

| Segment / Category | 2024–25 Size (USD) | Forecast 2030 (USD) | Forecast 2035 (USD) | CAGR % (Est.) | Key Growth Drivers |

|---|---|---|---|---|---|

| Global Chemicals (Overall) | ~$6.2 Trillion | ~$7.5 Trillion | ~$9.0 Trillion | 3.5 – 4% | Industrialization, consumer demand, sustainability |

| India – Total Chemicals | ~$220–250 Billion | ~$300 Billion | ~$400–450 Billion | 8 – 10% | Domestic demand + export boost, China+1 strategy |

| India – Petrochemicals | ~$58 Billion | ~$85 Billion | ~$120 Billion | 5 – 6% | Refinery integration, packaging, infra demand |

| India – Specialty Chemicals | ~$50 Billion | ~$80–90 Billion | ~$120–130 Billion | 10 – 12% | Pharma, agrochemicals, coatings, adhesives exports |

| Agrochemicals (India) | ~$11–12 Billion | ~$18–20 Billion | ~$28–30 Billion | 8 – 9% | Food security, rising rural consumption |

| Pharma Intermediates & APIs | ~$15–18 Billion | ~$25 Billion | ~$35–40 Billion | 9 – 10% | Healthcare demand, global outsourcing |

| Green & Bio-based Chemicals | ~$10–12 Billion (Global) | ~$25 Billion | ~$50 Billion | 12 – 14% | ESG push, renewable feedstocks |

| EV & Battery Chemicals | ~$6–7 Billion (Global) | ~$18 Billion | ~$35–40 Billion | 14 – 16% | EV adoption, energy storage demand |

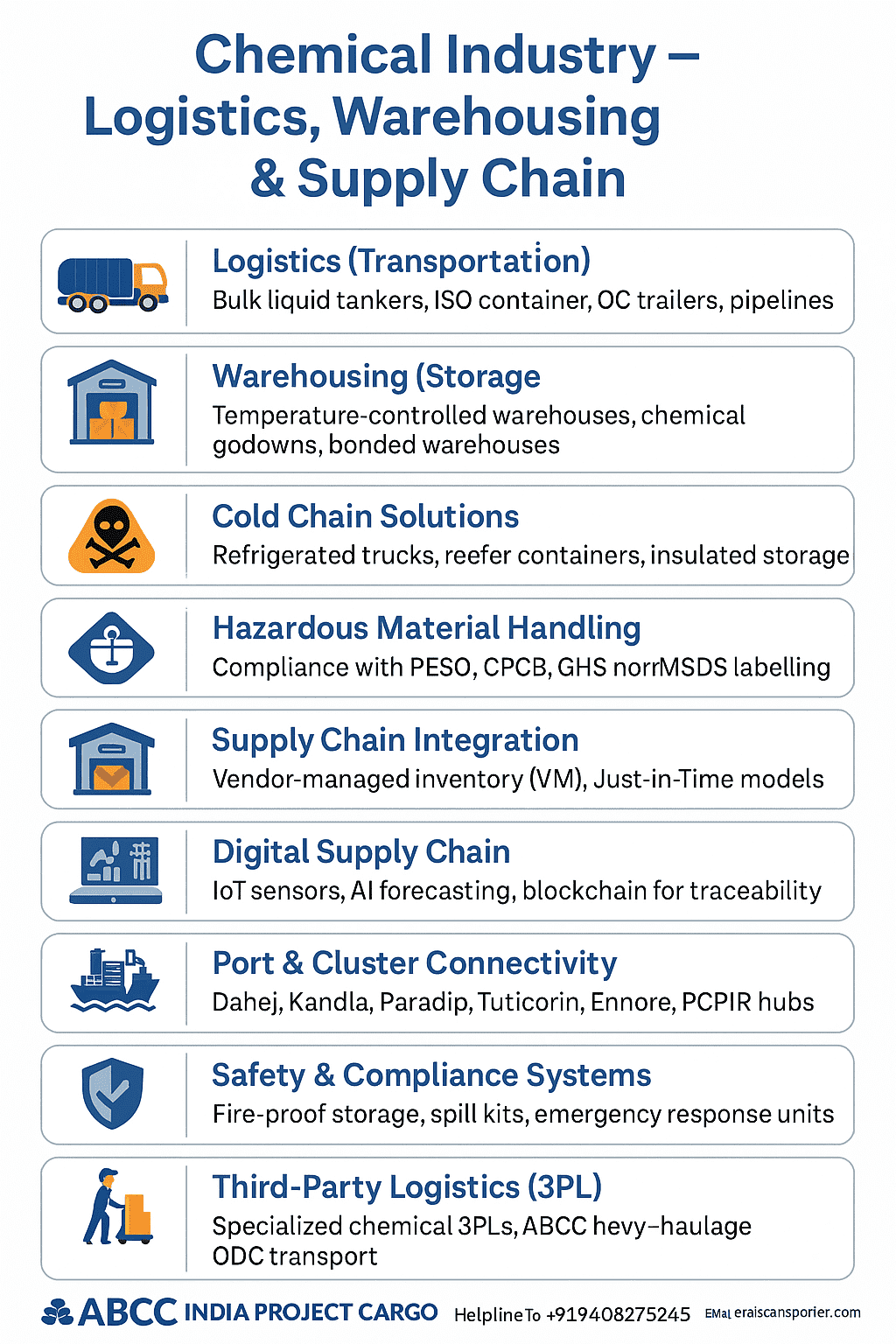

Chemical Industry – Logistics, Warehousing & Supply Chain

| Area / Function | Key Aspects / Activities | Impact on Chemical Industry |

|---|---|---|

| Logistics (Transportation) | Bulk liquid tankers, ISO containers, ODC trailers, pipelines | Safe transport of hazardous goods; cost efficiency |

| Warehousing (Storage) | Temperature-controlled warehouses, chemical godowns, bonded warehouses | Ensures safe storage, prevents spoilage & hazards |

| Cold Chain Solutions | Refrigerated trucks, reefer containers, insulated storage | Critical for pharma, specialty & food-grade chemicals |

| Hazardous Material Handling | Compliance with PESO, CPCB, GHS norms; MSDS labeling | Worker & environment safety, avoids penalties |

| Multi-Modal Transport | Rail (chemical rakes), road (tankers), coastal shipping, air freight | Reduces cost, improves speed, supports exports |

| Supply Chain Integration | Vendor-managed inventory (VMI), just-in-time (JIT) models | Lowers inventory cost, increases responsiveness |

| Digital Supply Chain | IoT sensors, AI forecasting, blockchain for traceability | Real-time monitoring, predictive logistics |

| Port & Cluster Connectivity | Dahej, Kandla, Paradip, Tuticorin, Ennore, PCPIR hubs | Boosts exports, global market access |

| Safety & Compliance Systems | Fire-proof storage, spill kits, emergency response units | Ensures accident-free, sustainable operations |

| Third-Party Logistics (3PL) | Specialized chemical 3PLs, ABCC heavy-haulage ODC transport | Outsourced efficiency with expert handling |

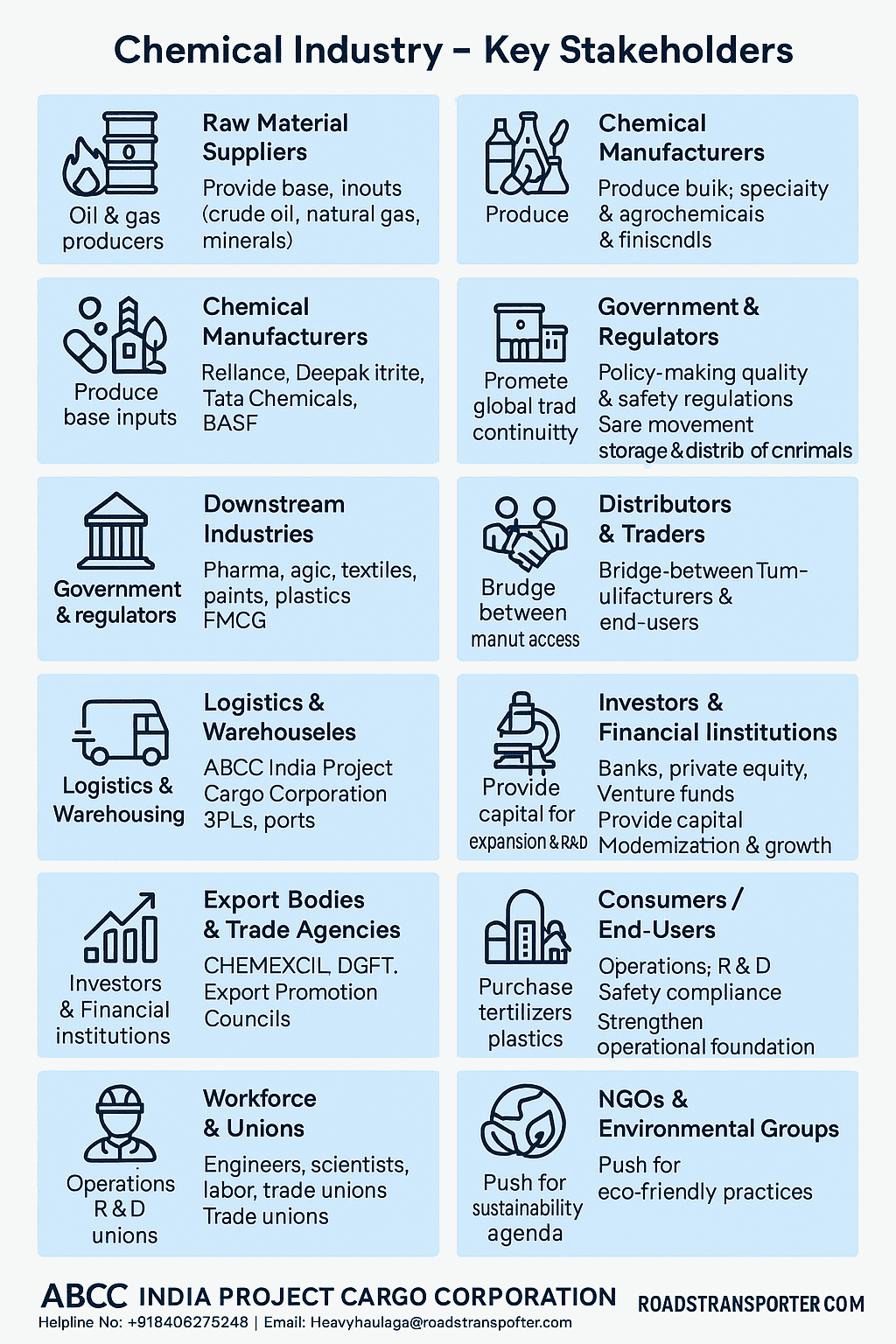

Chemical Industry – Key Stakeholders

| Stakeholder Category | Examples / Entities | Role in Industry | Impact on Chemical Ecosystem |

|---|---|---|---|

| Raw Material Suppliers | Oil & gas producers, petrochemical feedstock firms | Provide base inputs (crude oil, natural gas, minerals) | Backbone of entire value chain |

| Chemical Manufacturers | Reliance, Deepak Nitrite, Tata Chemicals, BASF | Produce bulk, specialty & agrochemicals | Core drivers of industry growth |

| Downstream Industries | Pharma, agro, textiles, paints, plastics, FMCG | Use chemicals in formulations & finished goods | Major demand generators |

| Government & Regulators | MoEFCC, BIS, CPCB, PESO, FSSAI, DGFT | Policy-making, quality & safety regulations | Ensure compliance, environmental sustainability |

| Logistics & Warehousing | ABCC India Project Cargo Corporation, 3PLs, ports | Safe movement, storage & distribution of chemicals | Critical for supply chain continuity |

| Distributors & Traders | Regional wholesalers, chemical traders | Bridge between manufacturers & end-users | Expand market access |

| Export Bodies & Trade Agencies | CHEMEXCIL, DGFT, Export Promotion Councils | Promote global trade & Indian chemical exports | Enhance India’s global share |

| Investors & Financial Institutions | Banks, private equity, venture funds | Provide capital for expansion & R&D | Enable modernization & growth |

| Research & Academia | CSIR, IITs, NCL Pune, global universities | Drive innovation, product development | Build long-term competitiveness |

| Consumers / End-Users | Agriculture sector, households, industries | Purchase fertilizers, plastics, pharma goods | Directly drive demand cycles |

| Workforce & Unions | Engineers, scientists, labor, trade unions | Operations, R&D, safety compliance | Strengthen operational foundation |

| NGOs & Environmental Groups | Greenpeace, local environmental NGOs | Push for eco-friendly practices | Shape sustainability agenda |

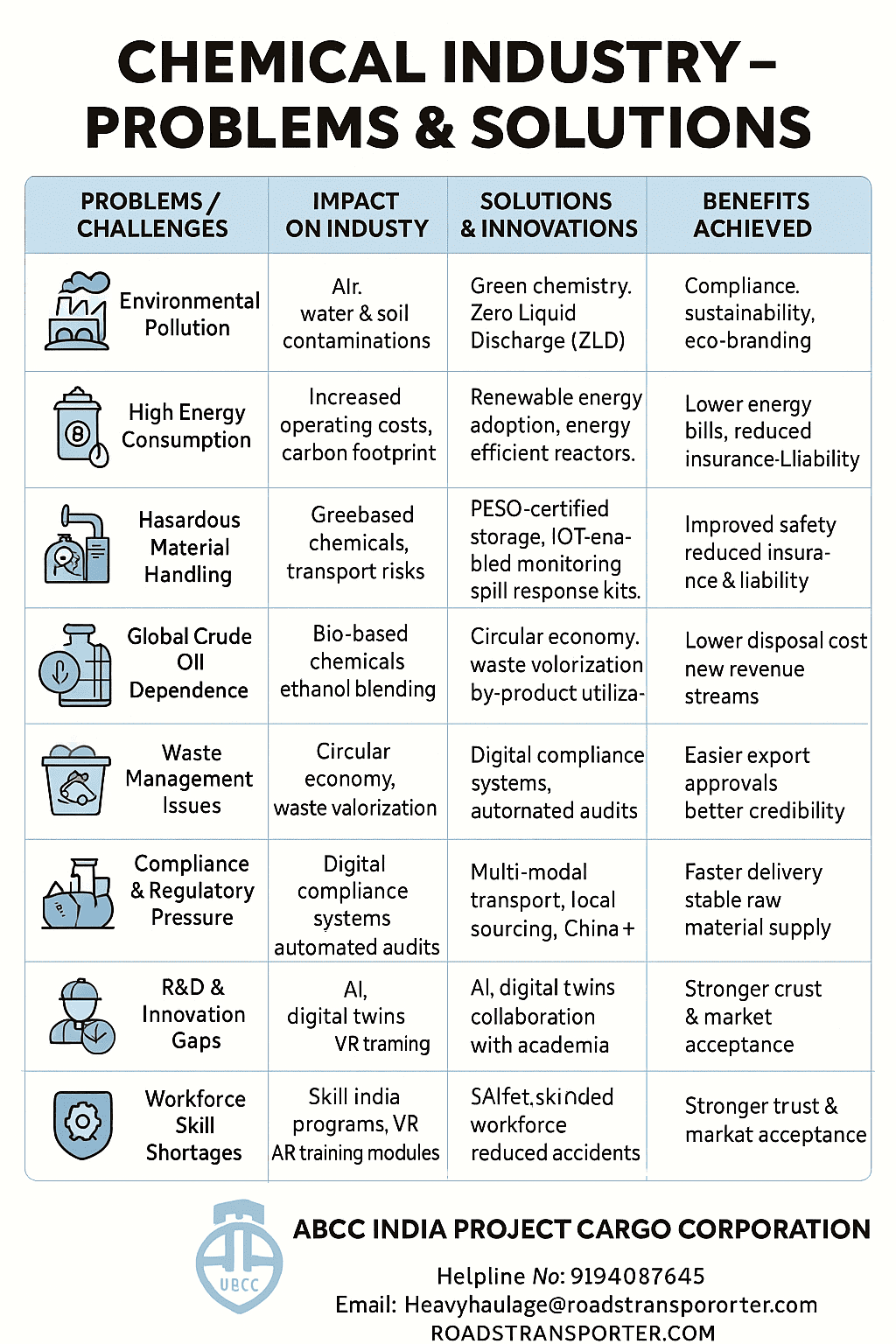

Chemical Industry – Problems & Challenges vs. Solutions & Innovations

| Problems / Challenges | Impact on Industry | Solutions & Innovations | Benefits Achieved |

|---|---|---|---|

| Environmental Pollution | Air, water & soil contamination; regulatory fines | Green chemistry, Zero Liquid Discharge (ZLD), effluent treatment plants (ETP) | Compliance, sustainability, eco-branding |

| High Energy Consumption | Increased operating costs, carbon footprint | Renewable energy adoption, energy-efficient reactors, ISO 50001 | Lower energy bills, reduced emissions |

| Hazardous Material Handling | Worker accidents, transport risks | PESO-certified storage, IoT-enabled monitoring, spill response kits | Improved safety, reduced insurance & liability |

| Global Crude Oil Dependence | Price volatility in petrochemical feedstocks | Bio-based chemicals, ethanol blending, recycling initiatives | Price stability, reduced import dependency |

| Waste Management Issues | Chemical waste disposal challenges | Circular economy, waste valorization, by-product utilization | Lower disposal cost, new revenue streams |

| Compliance & Regulatory Pressure | Higher cost of meeting international standards | Digital compliance systems, automated audits | Easier export approvals, better credibility |

| Supply Chain Disruptions | Delays, cost overruns, shortage of raw materials | Multi-modal transport, local sourcing, China+1 strategy | Faster delivery, stable raw material supply |

| R&D & Innovation Gaps | Low competitiveness vs. global players | AI, digital twins, collaboration with academia | Faster product development, improved efficiency |

| Workforce Skill Shortages | Lack of trained manpower in chemical operations | Skill India programs, VR/AR training modules | Safer, skilled workforce, reduced accidents |

| Public Perception & Safety Concerns | Negative image of chemical hazards | ESG reporting, community outreach, transparent safety practices | Stronger trust & market acceptance |

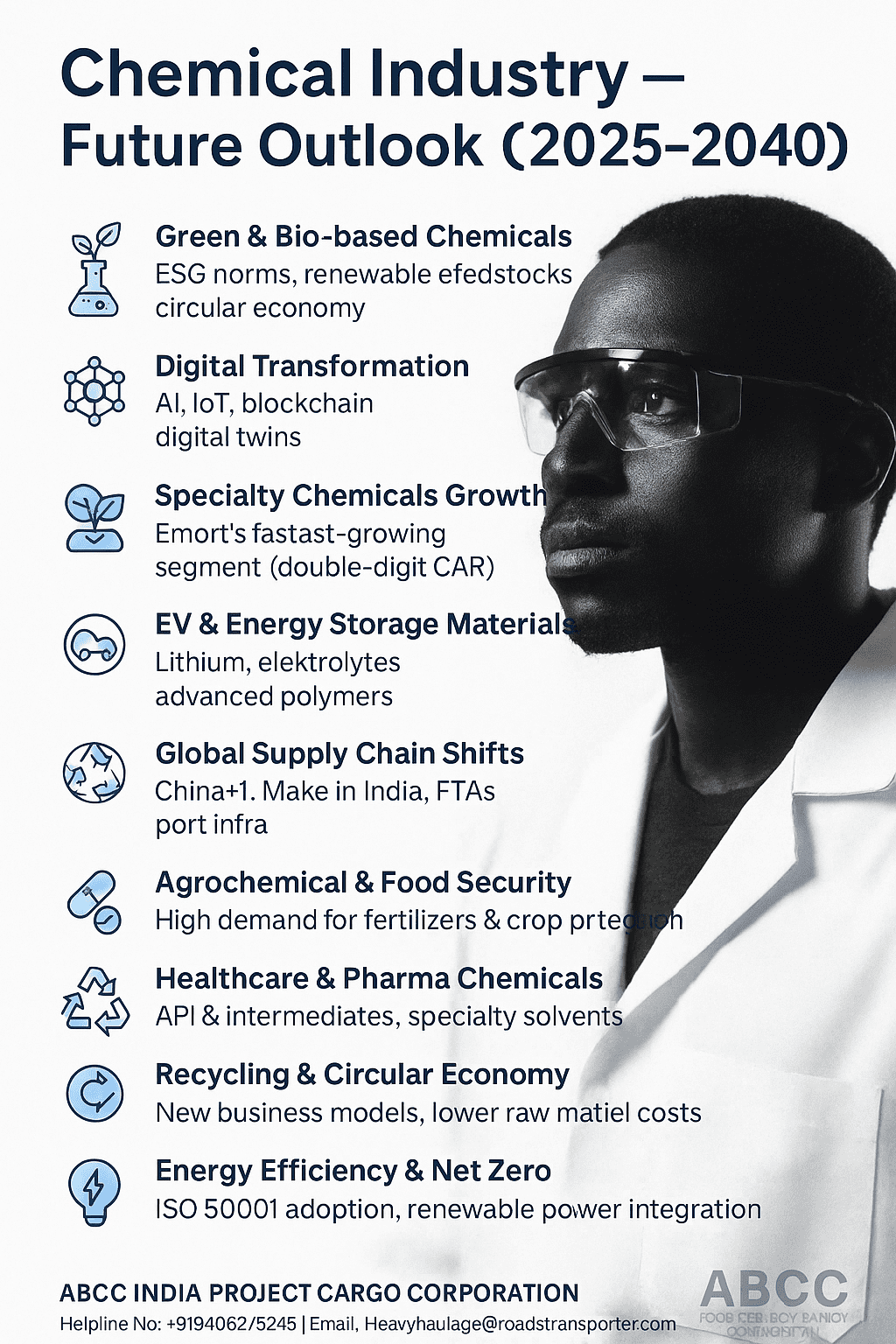

Chemical Industry – Future Outlook (2025–2040)

| Future Theme / Direction | Key Drivers / Factors | Expected Impact on Industry |

|---|---|---|

| Green & Bio-based Chemicals | ESG norms, renewable feedstocks, circular economy | Shift from fossil-based to sustainable chemistry |

| Digital Transformation | AI, IoT, blockchain, digital twins | Smart plants, predictive maintenance, efficiency |

| Specialty Chemicals Growth | Pharma, agro, coatings, adhesives exports | India’s fastest-growing segment (double-digit CAGR) |

| EV & Energy Storage Materials | Lithium, electrolytes, advanced polymers | New global market for EVs, batteries, renewables |

| Global Supply Chain Shifts | China+1, Make in India, FTAs, port infra | India emerging as manufacturing & export hub |

| Agrochemical & Food Security | Population growth, climate change adaptation | High demand for fertilizers & crop protection |

| Healthcare & Pharma Chemicals | API & intermediates, specialty solvents | Expanding exports, stronger domestic healthcare |

| Recycling & Circular Economy | Plastic waste management, EPR mandates | New business models & lower raw material costs |

| Energy Efficiency & Net Zero | ISO 50001 adoption, renewable power integration | Reduced carbon footprint, cost competitiveness |

| Global Mergers & Collaborations | Cross-border alliances, R&D partnerships | Faster innovation, global market access |

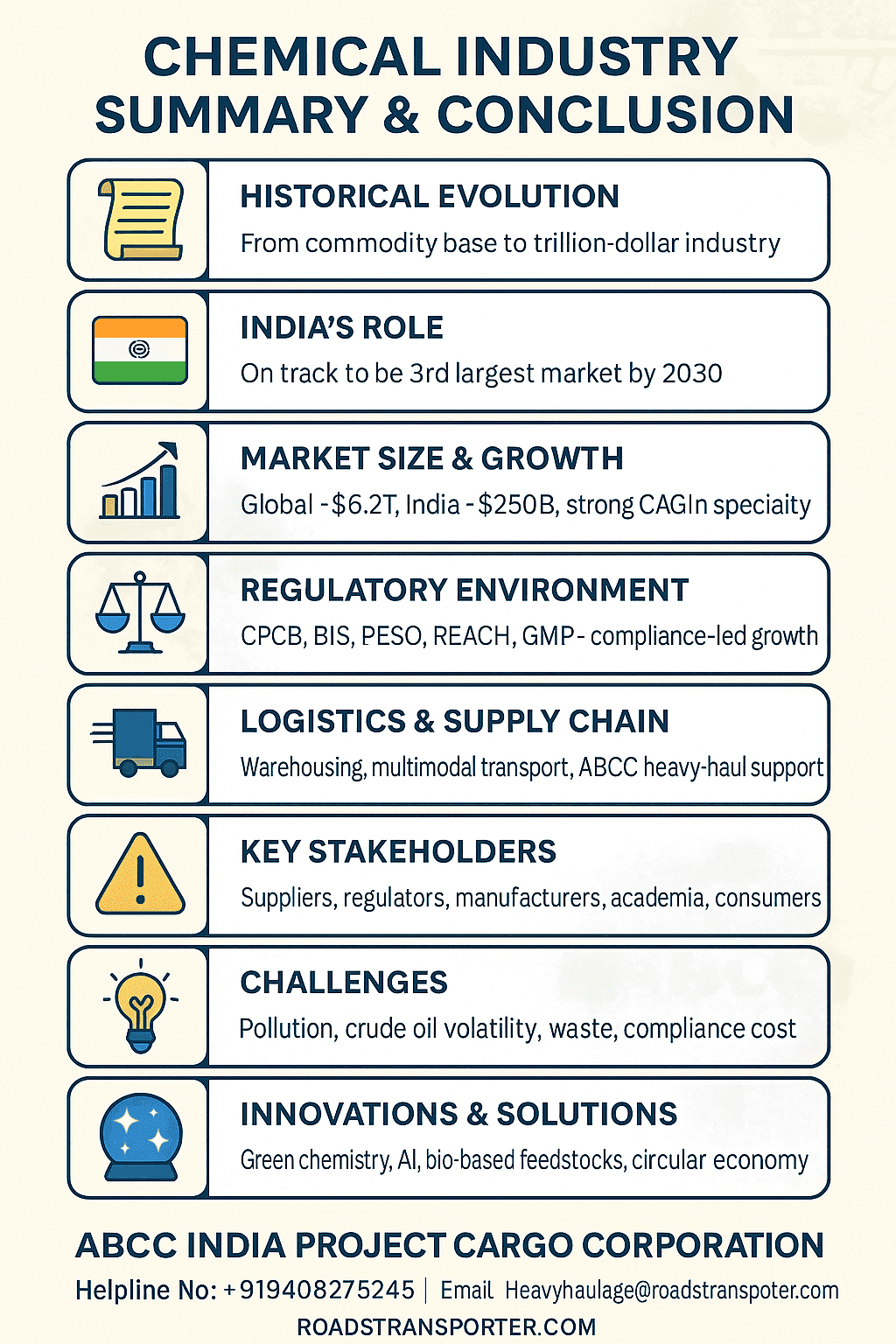

Chemical Industry – Summary & Conclusion

| Key Area | Summary Points |

|---|---|

| Historical Evolution | Grew from small-scale commodity production to a global trillion-dollar industry. |

| India’s Role | Emerging as world’s 3rd largest market by 2030; strong in agro, pharma, specialty chemicals. |

| Market Size & Growth | Global size ~$6.2 Trillion (2024), India ~$250 Billion, with high CAGR in specialty segment. |

| Regulatory Environment | Tightening norms (CPCB, BIS, PESO, REACH, GMP); compliance now key to competitiveness. |

| Logistics & Supply Chain | Specialized warehousing, cold chain, multimodal transport critical for safe & efficient flow. |

| Key Stakeholders | Raw material suppliers, manufacturers, regulators, logistics firms (ABCC), academia, consumers. |

| Challenges | Pollution, crude oil dependency, compliance cost, waste management, supply disruptions. |

| Innovations & Solutions | Green chemistry, AI, digital twins, bio-based feedstocks, circular economy. |

| Future Outlook (2025–2040) | Focus on sustainability, EV chemicals, pharma growth, specialty dominance, digitalization. |

🏁 Conclusion

The Chemical Industry is the backbone of global growth, powering sectors from agriculture to healthcare, and from infrastructure to energy. As India rises to become the 3rd largest chemical market by 2030, the sector is rapidly transforming with sustainability, specialty products, digitalization, and global trade expansion at its core.

In this journey of progress, ABCC INDIA PROJECT CARGO CORPORATION stands as a trusted logistics and heavy-haul partner, ensuring safe, timely, and cost-efficient movement of raw materials, finished chemicals, and over-dimensional cargo across India and beyond. With a commitment to safety, compliance, and innovation, ABCC continues to support the chemical industry’s supply chain backbone through:

- 🚛 Specialized chemical logistics & warehousing

- ⚖️ PESO & regulatory-compliant hazardous cargo handling

- 🌍 Seamless multi-modal transport & export support

- 🏭 Partnership with industries in petrochemicals, agrochemicals, and pharma

The future of the chemical industry is built on innovation, sustainability, and strong partnerships. With its expertise in logistics and project cargo, ABCC INDIA PROJECT CARGO CORPORATION will remain a driving force, enabling the industry to move safely, efficiently, and sustainably into the future.

📚 Chemical Industry – Recommended Books & Movies

| Category | Title / Name | Author / Creator / Director | Focus / Theme |

|---|---|---|---|

| Books – Global | Chemical Engineering Design | R. K. Sinnott, Gavin Towler | Process design, plant economics, safety |

| Elements of Chemical Reaction Engineering | H. Scott Fogler | Core reaction engineering concepts | |

| Industrial Chemistry | Mark Anthony Benvenuto | Overview of industrial chemical processes | |

| Green Chemistry: Theory and Practice | Paul Anastas, John Warner | Sustainable chemical practices | |

| Shreve’s Chemical Process Industries | George Austin | Industrial processes and raw material chemistry | |

| Books – India Focus | Chemical Process Technology & Simulation | Nayef Ghasem | Case studies with Indian context |

| Indian Chemical Industry: Challenges & Growth | Various industry papers (ICMAI, FICCI) | Indian market & regulatory evolution | |

| Bollywood Movies | Swades (2004) | Ashutosh Gowariker | Rural development, energy, water purification |

| Koi Mil Gaya (2003) – lab & experiments focus | Rakesh Roshan | Scientific curiosity, lab-based storytelling | |

| Chehre Pe Chehra (1981) | Raj Tilak | Chemical experiment drama | |

| Hollywood Movies | The Constant Gardener (2005) | Fernando Meirelles | Pharma industry & ethics |

| Erin Brockovich (2000) | Steven Soderbergh | Water pollution, corporate chemical negligence | |

| A Civil Action (1998) | Steven Zaillian | Chemical waste, environment law | |

| Lorenzo’s Oil (1992) | George Miller | Biochemistry & pharma research | |

| Thank You for Smoking (2005) | Jason Reitman | Chemical lobbying, corporate influence | |

| Chinese Movies / Series | Battle of Memories (2017) | Leste Chen | Neuroscience & chemical memory theme |

| Skyfire (2019) | Simon West | Volcanic chemistry & natural disasters | |

| The Island (2018) | Huang Bo | Survival science & chemistry | |

| Chinese medical dramas (various) | CCTV / Local studios | Pharma, R&D, medical chemistry |

{kind=link}