☀️ What is Solar Energy?

Solar energy is the power of the sun converted into useful electricity and heat. In simple words, it means using sunlight to produce power for homes, industries, and transportation.

Instead of depending only on coal, oil, or gas, solar energy teaches us:

“🌞 Why burn the earth’s future when the sun gives us free energy every day?”

👨🔬 Who Invented Solar Energy?

The journey of solar energy started with Alexandre Edmond Becquerel in 1839, a young French scientist.

He discovered the photovoltaic effect — the process of converting sunlight into electricity.

That single experiment lit up a path that, 200 years later, has become one of the world’s greatest energy revolutions.

📅 When Did Solar Become Popular?

Although discovered in 1839, solar panels only started becoming practical in the 1950s when Bell Labs created the first silicon solar cell.

From powering satellites in space 🚀 to becoming affordable rooftop panels on houses, solar has transformed into a mainstream clean energy source.

❓ Why Was Solar Invented?

The motivation was simple yet powerful:

- To find an alternative to fossil fuels.

- To create clean, renewable energy that doesn’t harm the planet.

- To bring energy independence to people and industries.

Solar energy was not just an invention—it was a vision to give light without smoke, hope without pollution, and growth without limits.

🌍 The Sun Never Stops Shining

Imagine this: every day, the sun gives the earth more energy in one hour than the whole world uses in a year.

The only question is: Do we have the courage and technology to capture it?

Solar energy is not only about science. It is about dreamers, innovators, and entrepreneurs who believed the impossible could be possible.

Today, every solar panel on a rooftop or in a desert solar farm is not just a machine—it is a symbol of human progress and sustainability.

☀️ The Industrialization of Solar Energy:

Every great industrial story begins with a spark — a small discovery that changes the destiny of industries, nations, and people.

The story of solar energy is one such spark. A spark that turned into fire, and then into a revolution that powers the 21st century.

🌱 A Young Dreamer in 1839

In 1839, in the city of Paris, a 19-year-old physicist named Alexandre Edmond Becquerel was experimenting in his father’s laboratory. He dipped metal electrodes in a conducting solution, exposed them to sunlight, and to his amazement — electricity was born.

This was the first photovoltaic effect in history.

Of course, Becquerel didn’t know he had just planted a seed that would one day grow into a trillion-dollar industry.

But every leadership journey begins with someone daring to ask: “What if?”

🚀 From Lab to Space

For nearly a century, the idea of solar remained trapped in books and experiments. It wasn’t until the 1950s that Bell Labs created the first practical silicon solar cell.

And where did solar energy first find its purpose?

In space. Satellites circling Earth couldn’t carry barrels of oil or coal. They needed something light, durable, and eternal. Solar was the answer.

For the first time, the sun’s power was not only seen as natural light — it became industrial energy.

🌍 Crisis Creates Opportunity

Then came the 1970s oil crisis. Gas stations went dry, industries panicked, and governments realized the danger of depending on fossil fuels.

It was a wake-up call — the world needed an alternative.

That’s when solar energy leaped out of the shadows and into the boardrooms of leaders. Germany, Japan, and the U.S. began investing in solar technology. Visionary governments offered subsidies, and entrepreneurs dared to set up solar companies.

The leadership lesson?

Industries often grow fastest not in comfort, but in crisis.

🏭 The Great Leap: China and Global Expansion

But the real industrial explosion of solar came when China entered the game.

Factories scaled up panel production, costs dropped dramatically, and suddenly, solar was not just for scientists or governments — it became affordable for households, factories, and entire nations.

From deserts in India 🌞 to rooftops in California 🏠, solar panels began to rise like soldiers of a new industrial revolution.

Solar energy was no longer a choice. It was becoming a global movement.

⚡ More Than Power: A Social Revolution

The industrialization of solar has done more than just light up factories:

- In rural Africa and Asia, children now study under solar lamps instead of kerosene flames.

- Villages once trapped in darkness now run small businesses with solar-powered machines.

- Homeowners have turned into energy producers, selling power back to the grid.

This is not just an industrial story. It is a human story of empowerment, independence, and equality.

📈 The Corporate Angle: Why Solar Became Big Business

From the perspective of business leadership, solar industrialization is a textbook case study.

Innovation → Market → Scale

Becquerel’s discovery → Bell Labs’ invention → China’s scaling.

Policy + Entrepreneurship = Industrial Revolution

Without government incentives, the industry would have stalled.

Without entrepreneurs and logistics providers, solar would have never reached homes and industries.

Solar became big business because leaders realized:

“The sun shines everywhere, so the market is infinite.”

🌟 The Future: A Sunrise Yet to Come

Today, solar contributes a significant share of global electricity. But this is just the beginning.

- New Technology: Perovskite cells, floating solar farms, and solar highways are rewriting possibilities.

- Corporate Strategy: From Tesla’s solar roofs to smart cities powered by renewables, the business of solar is becoming central to global leadership.

- Responsibility: In a world struggling with climate change, solar energy is not just about profit, it is about survival.

And the leadership call is clear:

The future belongs to those who rise with the sun.

✨ Final Leadership

The industrialization of solar energy is more than history.

It is a story of leaders who dared to dream, governments who chose courage over comfort, and industries that saw responsibility as opportunity.

The sun has always risen. But only now, humanity has learned to rise with it.

And in that rise, lies not just the future of energy — but the future of leadership.

☀️ Types of Solar Uses & Tentative Price Range

| 🔆 Type of Solar Use | 🏢 Application / Usage | 💰 Tentative Price Range (India) | 📌 Notes |

|---|---|---|---|

| 🌞 Solar Rooftop Systems | Residential homes, offices, schools | ₹45,000 – ₹65,000 per kW | Reduces household electricity bills by 70–80% |

| 🏭 Industrial Solar Power Plants | Factories, warehouses, large-scale industries | ₹38,000 – ₹55,000 per kW | Bulk usage, helps industries cut long-term costs |

| 🏠 Solar Water Heaters | Homes, hotels, hospitals | ₹20,000 – ₹1,50,000 (100–500 LPD) | Cost-effective replacement for electric/geyser heating |

| 💡 Solar Street Lights | Highways, rural roads, parks | ₹8,000 – ₹25,000 per unit | Used for villages, smart cities, & infrastructure |

| 🚜 Solar Pumps (Agriculture) | Irrigation, farms, rural water supply | ₹1.5 Lakh – ₹4 Lakh per pump (2–10 HP) | Helps farmers reduce diesel/electricity costs |

| 🔋 Solar Power Banks & Portable Kits | Small shops, rural areas, travel | ₹5,000 – ₹50,000 | Used for mobile charging, lights, and backup in off-grid areas |

| 🚘 Solar EV Charging Stations | Electric cars, buses, two-wheelers | ₹2 Lakh – ₹10 Lakh | Future of mobility, supports electric vehicle adoption |

| 🏢 Solar Mini Grids / Off-Grid Systems | Remote villages, islands, mining areas | ₹50,000 – ₹80,000 per kW | Provides power where electricity grid is unavailable |

| 🏨 Solar Air Conditioning Systems | Hotels, offices, data centers | ₹1 Lakh – ₹3 Lakh per ton | Saves 30–40% electricity costs in commercial cooling |

☀️ Solar Industry — Manufacturing & Production Structure (Step-by-Step)

| 🔧 Step | 🧩 What happens | 🧪 Inputs | 📦 Outputs | ✅ Quality & Compliance | ⏱️ Indicative time |

|---|---|---|---|---|---|

| 1️⃣ Raw Material Sourcing | Contract suppliers and check specs | Polysilicon/Si, glass, EVA, backsheet, frames, junction boxes, silver/aluminum paste | Approved lots | COA check, RoHS/REACH, BIS/IEC material specs | 2–10 days |

| 2️⃣ Polysilicon → Ingot | Melt/seed growth (Czochralski) | Polysilicon | Mono/multi ingots | Resistivity & impurity tests | 1–3 days |

| 3️⃣ Ingot → Wafering | Slice, edge, clean | Ingots | Silicon wafers | Thickness, micro-crack, TTV control | 1–2 days |

| 4️⃣ Cell Line (Surface/Texturing) | Texturing, cleaning | Wafers, chemicals | Textured wafers | Reflectance/roughness tests | Hours |

| 5️⃣ Cell Doping/Diffusion | Add p/n junction | Wafers, dopants | PN-junction wafers | Sheet resistance, lifetime | Hours |

| 6️⃣ ARC & Passivation | Anti-reflection & passivation layers | Coating gases | Coated wafers | Color uniformity, EQE | Hours |

| 7️⃣ Metallization & Firing | Screen print fingers/busbars; fire | Silver/Al paste | Finished cells | Cell IV test, EL imaging, binning | Hours |

| 8️⃣ Stringing & Tabbing | Connect cells into strings | Cells, ribbons | Cell strings | Pull test, alignment check | < 1 day |

| 9️⃣ Lay-up & Lamination | Glass–EVA–Cells–EVA–Backsheet stack; laminate | BOM set | Laminated module | Gel content, voids check | < 1 day |

| 🔟 Framing & J-Box | Fit aluminum frame; attach junction box | Frames, sealant, J-box | Finished module | Hi-Pot, ground, IP rating | < 1 day |

| 1️⃣1️⃣ Final Test & Pack | IV curve, EL, flash test; label | Test bench | Tested modules | IEC/UL/BIS labels, serials | < 1 day |

| 1️⃣2️⃣ BOS Manufacturing | Inverters, structures, cables, SCADA | Electronics, steel | BOS kits | Type tests, earthing checks | 3–15 days |

| 1️⃣3️⃣ Warehousing & Dispatch | Store FIFO; load for project | Modules & BOS | Packed lots | Drop/tilt tests, count & seal | 1–3 days |

| 1️⃣4️⃣ EPC Installation | Civil, mounting, DC/AC wiring | Modules, BOS, crews | Built plant | PQP, torque logs, insulation | Rooftop: 2–8 weeks; Utility: 3–12 months |

| 1️⃣5️⃣ Commissioning & Handover | Energize, PR test, docs | Completed plant | Operational asset | Grid sync, PR/GHI baseline | 1–3 weeks |

Cross-functional units (run across all steps):

🔬 R&D • 📊 Process Engineering • 🛡️ QA/QC • 🧯 EHS • 🧭 Compliance (IEC 61215/61730, BIS) • 🔗 Supply Chain • 🛠️ Maintenance • 📈 Finance & Sales • 🚚 Logistics.

🔄 Solar Industry — Product Lifecycle & Development Process (Gate-Wise)

| 🚀 Lifecycle Phase | 🎯 Goal | 📝 Key Deliverables | 🧪 Validation/Gate | ⏱️ Indicative time |

|---|---|---|---|---|

| G0: Market Discovery | Find need & business case | Market/competitor scan, pricing, target PR/IRR | Gate review: go/no-go | 2–4 weeks |

| G1: Feasibility & Concept | Choose tech & specs | Tech map (PERC/TopCon/HJT/Perovskite), BOM targets, cost model | Tech feasibility sign-off | 3–6 weeks |

| G2: R&D & Prototype | Build working samples | Lab cells/modules, process window | Reliability quick checks, IV/EL, mini-IEC | 6–12 weeks |

| G3: Pilot & Certification | Run small batch & certify | Pilot run, FMEA, control plan, IEC/BIS testing | Certification pass, yield ≥ target | 8–16 weeks |

| G4: Supply Chain & Tooling | Secure vendors & tools | Supplier PPAP, molds/jigs, safety plan | PPAP approval, EHS audit | 4–8 weeks |

| G5: Mass Production Ramp | Hit volume & quality | SOP, work instructions, SPC dashboards | FPY/yield, CTQ stable | 4–12 weeks |

| G6: Distribution & Install | Deliver to projects | Logistics plan, project kit lists | Delivery OTIF, site QA logs | Ongoing |

| G7: Operations & O&M | Keep output high | PR/availability KPIs, cleaning, thermal scans | PR ≥ baseline, warranty claims | 25–30 years |

| G8: Upgrade/Repower | Improve performance | Inverter/Module upgrades, tracking | ROI check, safety review | 1–6 months |

| G9: End-of-Life & Recycling | Recover value safely | Dismantle plan, glass/Si recovery | Environmental compliance | 1–3 months |

| Feedback Loop | Learn & redesign | Field data → next-gen specs | NPI kick-off | Continuous |

Core controls throughout the lifecycle:

📌 DFMEA/PFMEA • SPC on CTQs (efficiency, power bin, EL defects) • Traceability (serialization) • Warranty stack (product/performance) • EHS (chemical handling, fire safety) • Cyber/SCADA security.

🧭 Practical Notes for Leaders

- Cost drivers: cell efficiency, silver paste, glass/EVA pricing, scale, and yield.

- Risk mitigators: multi-sourcing, tight incoming QC, preventive maintenance, and robust logistics.

- Data matters: use PR, CUF, degradation rate, and LCOE to steer decisions.

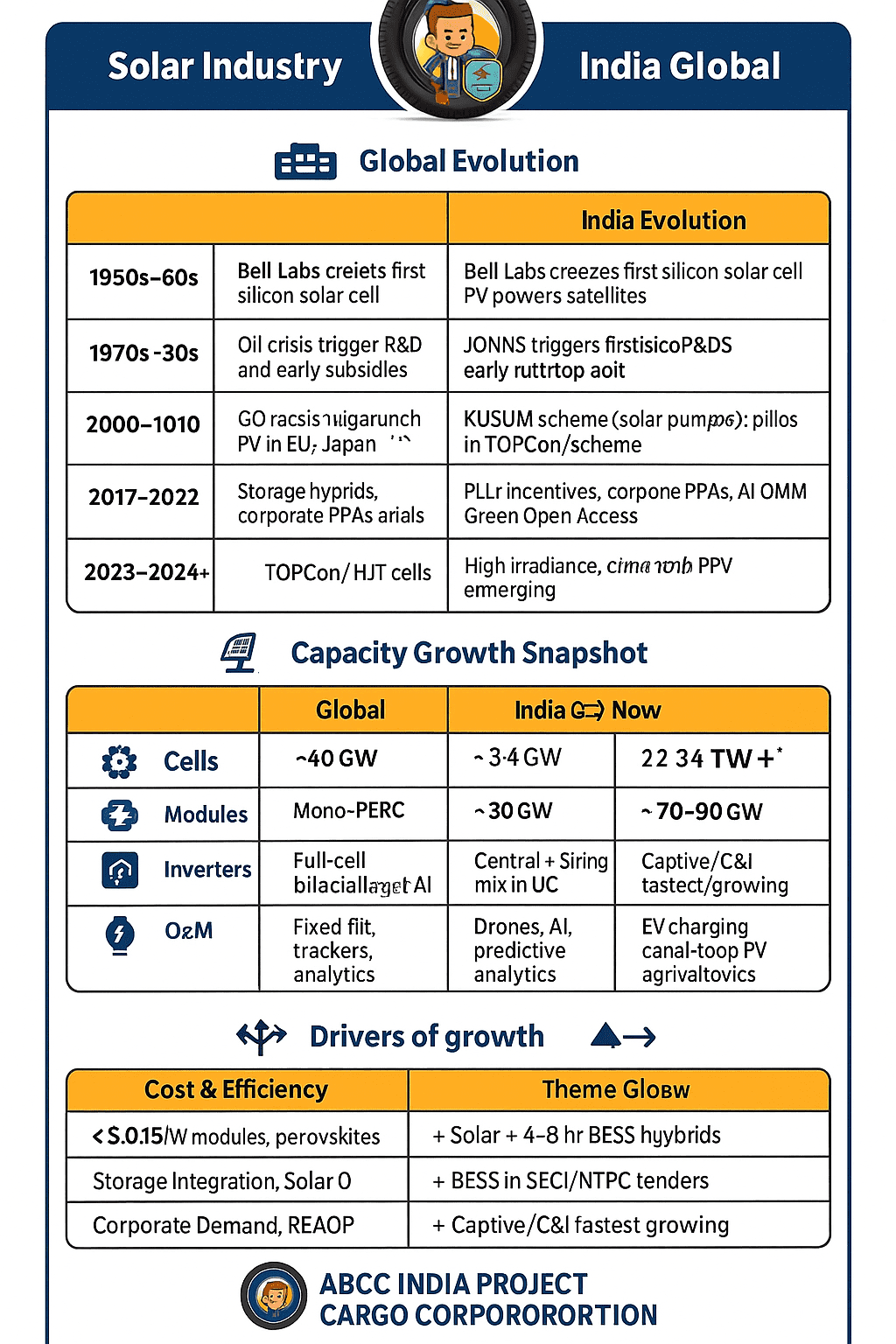

☀️ Solar Industry Evolution — India & Global

| 🗓️ Period | 🌍 Global Evolution | 🇮🇳 India Evolution |

|---|---|---|

| 1950s–60s | Bell Labs creates first silicon solar cell; PV powers satellites | – |

| 1970s | Oil crisis triggers R&D, early subsidies in US, EU, Japan | – |

| 1990s | Grid-connected PV in EU/Japan; inverters mature | – |

| 2000–2010 | EU feed-in tariffs, US tax credits; rapid rooftop adoption | 2009–10: JNNSM launched, first utility parks |

| 2010–2016 | China scales production; costs drop sharply | 2014–16: SECI/NTPC tenders; state solar parks |

| 2017–2019 | Bifacial, trackers, large-scale projects; record-low tariffs | Record-low tariffs; Rajasthan, Gujarat, TN scale-up |

| 2020–2022 | Storage hybrids, corporate PPAs, AI O&M | KUSUM scheme (solar pumps), domestic manufacturing push |

| 2023–2024+ | TOPCon/HJT cells, AI O&M, floating PV, green hydrogen | PLI incentives, corporate PPAs, captive/C&I boom |

⚡ Technology Evolution (Global ↔ India)

| 🔧 Area | 🌍 Global Trend | 🇮🇳 India Trend |

|---|---|---|

| Cells | Multi-Si → Mono-PERC → TOPCon/HJT | Rapid shift to Mono-PERC, pilots in TOPCon |

| Modules | Full-cell → Half-cut, bifacial, larger wafers | 144-cell, bifacial utility projects common |

| Inverters | Central → String-heavy, smart AI | Central + String mix in utility & rooftop |

| Structures | Fixed-tilt → Trackers (1P/2P) | Trackers in mega-parks; canal-top/float PV pilots |

| O&M | Drones, AI, predictive analytics | Drones, module cleaning robots emerging |

📈 Capacity Growth Snapshot

| 🌍 Global | 🇮🇳 India |

|---|---|

| 2010: ~40 GW | 2014: ~3–4 GW |

| 2020: ~700 GW | 2019: ~30 GW |

| 2024: 1–1.5 TW+ | 2024: ~70–90 GW |

🧭 Drivers of Growth

| 🌍 Global Drivers | 🇮🇳 India Drivers |

|---|---|

| EU feed-in tariffs, US tax credits, China’s scale-up | JNNSM, SECI auctions, rooftop subsidies |

| Corporate PPAs, ESG mandates | Green Open Access, PLI scheme, KUSUM pumps |

| Storage cost decline, EV adoption | High irradiance, falling tariffs, C&I demand |

🔮 5–10 Year Outlook

| 🎯 Theme | 🌍 Global | 🇮🇳 India |

|---|---|---|

| Cost & Efficiency | <$0.15/W modules, perovskites | Lower $/W with domestic value chain |

| Storage Integration | Solar + 4–8 hr BESS hybrids | BESS in SECI/NTPC tenders |

| Corporate Demand | RE100, 24×7 green PPAs | Captive/C&I fastest growing |

| Manufacturing | Global shift to high-efficiency | India: PLI-driven polysilicon→module chain |

| New Markets | Green hydrogen, solar fuels | EV charging, canal-top PV, agrivoltaics |

🌐 Solar Industry Market Size — India vs Global

| ❇️ Region | 💰 Market Size / Revenue Estimate | 📅 Reference Year | 🔍 Notes / Source |

|---|---|---|---|

| Global | USD 253.69 billion | 2023 | Global solar power market size (Fortune Business Insights) |

| Global (System Market) | USD 258.76 billion | 2023 | Global solar energy systems market (Extrapolate) |

| Global (Earlier) | USD 160.3 billion | 2021 | Global solar energy systems (Grand View Research) |

| India | USD 10.4 billion | 2023 | Indian solar energy market revenue (PSMarketResearch) |

| India (Forecast) | USD 14 billion | 2031 | Projected India solar market size (TechSci) |

| India (Panels Segment) | USD 7.31 billion | 2023 | India solar PV panels market (Grand View Research) |

| India (Module Market Projection) | USD 17.20 billion | 2032 | India solar module market forecast (Markets & Data) |

☀️ Top 10 Solar Manufacturing Companies (Worldwide – Shortlist)

- LONGi Green Energy (China) — wafer-to-module giant; scale + mono expertise.

- JinkoSolar (China) — global shipments leader; sales reach in 180+ countries.

- Trina Solar (China) — utility-scale projects + trackers + high-efficiency modules.

- JA Solar (China) — strong cell tech (PERC/TOPCon), reliable utility presence.

- Canadian Solar (Canada/China) — vertical integration + global project pipeline.

- First Solar (USA) — thin-film CdTe specialist; low carbon footprint modules.

- Qcells (Hanwha, South Korea/USA/EU) — strong in distributed/C&I, ingot-to-module in U.S.

- Tongwei (China) — world leader in cells; expanding into modules aggressively.

- Aiko Solar (China) — high-efficiency cell innovator; premium modules.

- Astronergy (CHINT) (China) — bifacial utility modules, bankable track record.

☀️ The Rise of the Solar Titans: Top 10 Manufacturers Driving the World’s Energy Revolution

Every revolution has its champions. The solar industry — once a dream powered by laboratories and small rooftop experiments — is now a trillion-dollar global force, and behind its rise are companies that dared to think big, invest boldly, and deliver consistently. The following story unites the Top 10 Solar Manufacturing Companies worldwide into one sweeping narrative of leadership, innovation, and courage.

🌟 LONGi Green Energy — “The Power of Focus”

The story of LONGi begins in Xi’an, China in 2000 with a conviction: monocrystalline wafers will outlast all rivals. While competitors chased volume in multicrystalline, LONGi doubled down on efficiency. By betting on mono-PERC early, the company aligned with the industry’s future. Today, LONGi is the world’s largest solar manufacturer, exporting wafers, cells, and modules globally. Its success shows that long-term focus, when coupled with scale and quality discipline, can redefine an industry.

🌟 JinkoSolar — “Execution at Global Scale”

Founded in 2006, JinkoSolar represents the power of reliable execution. With a presence in over 180 countries, Jinko built trust not through flashy claims but by delivering on-time, high-performing panels again and again. It pioneered bifacial technology at scale, won bankability rankings repeatedly, and became a supplier of choice for both utility projects and rooftop developers. Jinko’s leadership lesson is clear: in a high-growth, high-risk market, consistency is the real differentiator.

🌟 Trina Solar — “From Manufacturer to Solution Provider”

Born in 1997, Trina Solar didn’t stop at modules. It expanded into solar trackers, storage, and EPC services, offering customers a complete ecosystem. Its Vertex series modules broke efficiency records, while its smart trackers increased energy yields in utility-scale farms. Trina’s story is about ambition: instead of staying a module supplier, it became a solutions leader. The lesson? Scale isn’t enough — integration creates trust and recurring value.

🌟 JA Solar — “Consistency as Identity”

Founded in 2005, JA Solar took a different path: no big slogans, no risky bets. Its approach? Relentless consistency. By investing in strong cell production (PERC, TOPCon), focusing on global certifications, and ensuring reliable shipments, JA became one of the most bankable names in solar. In many tenders, EPCs prefer JA simply because “it always works.” The leadership lesson: sometimes, quiet reliability builds the loudest reputation.

🌟 Canadian Solar — “The Entrepreneur’s Dream”

Canadian Solar’s story is a global entrepreneurial tale. Founded in 2001 in Ontario by Dr. Shawn Qu, the company began with humble means but an ambitious vision: make solar affordable worldwide. Two decades later, Canadian Solar is not just a module supplier but also a top developer of utility-scale solar farms, with gigawatts of projects across continents. The company symbolizes cross-border persistence and shows how one leader’s vision can cross cultures and capital markets to transform an industry.

🌟 First Solar — “Different on Purpose”

In a world dominated by crystalline silicon, First Solar of the USA took the contrarian route — thin-film Cadmium Telluride (CdTe). This choice gave it unique advantages: better hot-climate performance, lower carbon footprint, and fully integrated factories. While others fought in the c-Si price war, First Solar carved its niche in utility-scale markets where its modules outperform. Its recycling programs make it a sustainability leader. The lesson? Different can be powerful, if done with conviction.

🌟 Qcells (Hanwha) — “Local Manufacturing, Global Vision”

Qcells, once a German startup, became a South Korean-backed global brand under Hanwha. It has since risen as a leader in distributed solar (residential and C&I) and as a symbol of manufacturing revival in the West. With factories in the US and EU, Qcells caters to markets that prioritize local supply, quality, and trust. Its Q.ANTUM cell technology remains widely adopted. The story of Qcells proves that localization + corporate backing can challenge global giants.

🌟 Tongwei Solar — “Owning the Heart of the Supply Chain”

Tongwei’s journey is almost mythical: from a feed and aquaculture company to becoming the largest solar cell producer in the world. By specializing in cells, Tongwei became the backbone of the global industry — supplying nearly every major module brand. Its story shows the power of specialization: rather than diversifying everywhere, Tongwei mastered the critical bottleneck, making itself indispensable.

🌟 Aiko Solar — “Premium Through Innovation”

While many Chinese solar companies competed on price, Aiko Solar positioned itself differently: premium innovation. Specializing in high-efficiency back-contact and TOPCon cells, Aiko built its reputation with clients who value performance over cost. Its story teaches that even in a commoditized market, differentiation through technology can win loyalty. The leadership lesson? Don’t compete where everyone is cheapest — compete where you are unique.

🌟 Astronergy (CHINT Group) — “Bankability as a Business Model”

Part of CHINT, Astronergy focused on utility-scale modules, with special attention to bifacial technologies. But its real edge lies in bankability: Astronergy works closely with financial institutions to ensure its modules qualify for project financing. This positioning gives developers confidence to choose Astronergy. The lesson: in capital-intensive industries, winning financiers is as critical as winning customers.

🌍 The Collective Impact

Together, these 10 companies power more than 80% of global solar shipments. They are not just manufacturers; they are architects of the clean energy transition.

- They have reduced the cost of solar modules from $3/W in 2010 to under $0.20/W today.

- They have turned solar into the cheapest new energy source in most parts of the world.

- They are enabling green hydrogen, EV charging, and 24×7 renewable grids.

Each company’s journey is different — some chose scale, some chose technology, some chose specialization. But all share a common DNA: vision, courage, and relentless execution.

🚛 ABCC INDIA PROJECT CARGO CORPORATION – Enabler of Solar’s Rise

While these global giants manufacture, someone must move their technology to the ground. That’s where ABCC INDIA PROJECT CARGO CORPORATION comes in.

From heavy solar modules and inverters to oversized transformers and trackers, ABCC specializes in heavy haulage, road route surveys, permits, and damage-free transport. In India’s deserts, hills, and cities, ABCC ensures that the solar revolution isn’t just a global story — it becomes a local reality.

📧 Email: [email protected]

📞 Helpline No: +919408275245

🌐 Website: ROADSTRANSPORTER.COM

✨ Final Leadership Lesson

The industrialization of solar energy is not just about technology; it is about leadership choices. LONGi chose efficiency, Jinko chose execution, Trina chose ecosystem, JA chose consistency, Canadian Solar chose persistence, First Solar chose difference, Qcells chose localization, Tongwei chose specialization, Aiko chose innovation, and Astronergy chose bankability.

Together, they prove a timeless truth: when vision meets execution, industries transform.

And in solar, that transformation is lighting up the world.

☀️ Best Era & Recession Time for the Solar Industry (When & Why)

| 🗓️ Period | 📈 Best Era (Growth Boom) | 💡 Why it was the Best Era | 📉 Recession / Downturn | ⚠️ Why it Faced Recession |

|---|---|---|---|---|

| 1970s | 🌟 Oil Crisis triggered R&D interest in solar | Governments funded solar as alternative to oil; birth of industrial PV | – | – |

| 1990s | 🌟 Europe & Japan grid-connected programs | Early rooftop subsidies, FiT pilots, inverter advancements | – | – |

| 2008–2011 | 🌟 Golden Era of EU Feed-in Tariffs | Germany, Spain, Italy rolled out generous FiTs → rapid installation boom | 2012–2014 | Oversupply, subsidy cuts in EU, many small firms bankrupt |

| 2015–2019 | 🌟 Utility-scale solar boom | China’s scaling, India’s JNNSM Phase II, falling costs below coal | – | – |

| 2020–2023 | 🌟 Record-low tariffs, global adoption | Solar became cheapest energy; corporate PPAs, ESG investments surged | 2020 (short) | COVID-19 supply chain disruptions; project delays |

| 2023–2025+ (Present) | 🌟 Hybrid era: Solar + Storage + Green Hydrogen | Mass adoption, tech upgrades (TOPCon, bifacial, trackers), corporate demand | – | – |

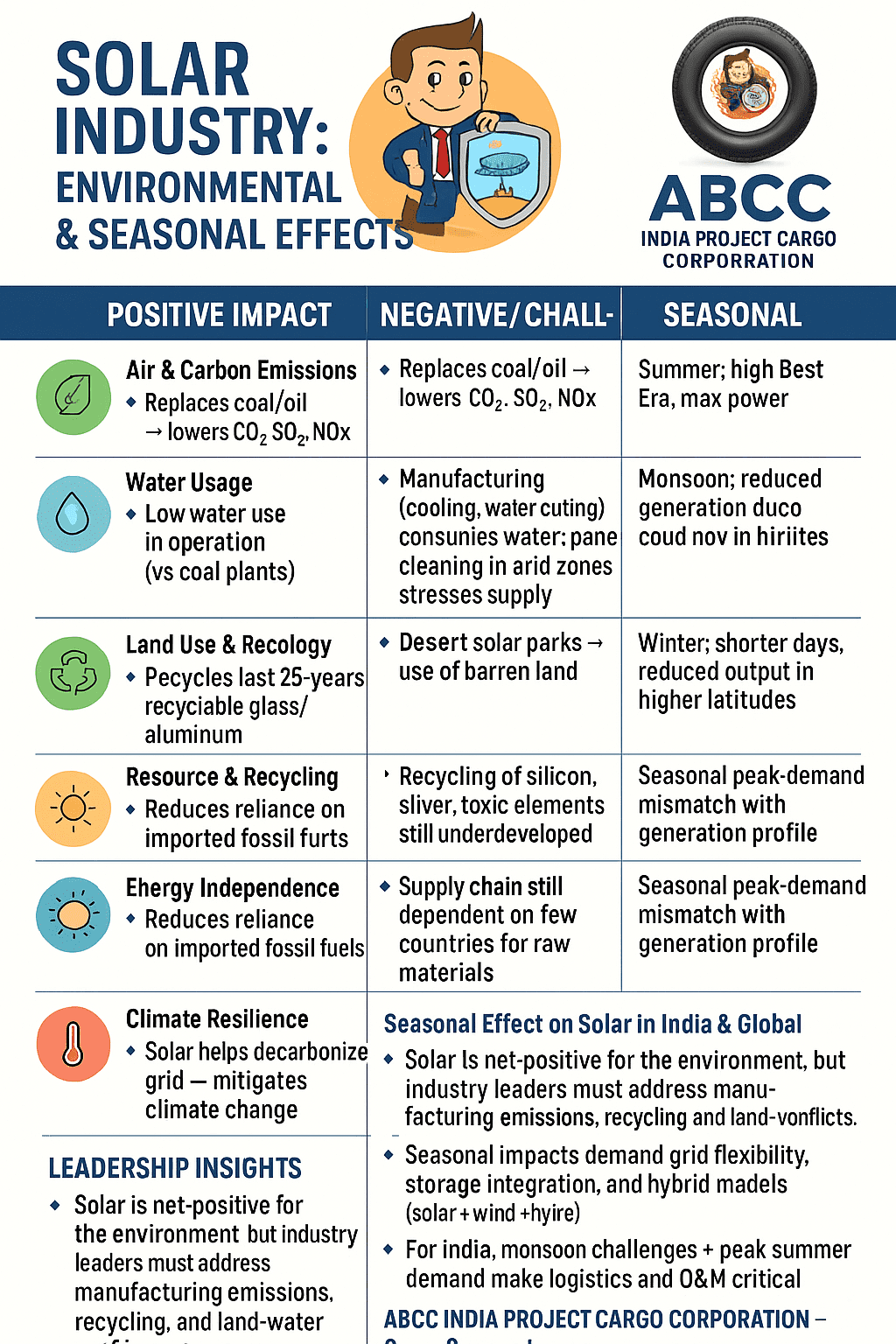

☀️ Solar Industry – Environmental & Seasonal Effects

| 🌍 Category | ✅ Positive Impact | ⚠️ Negative / Challenges | 🕰️ Seasonal Effect | 📌 Notes |

|---|---|---|---|---|

| 🌿 Air & Carbon Emissions | Replaces coal/oil → lowers CO₂, SO₂, NOx | Panel production uses energy-intensive processes (polysilicon refining) | Summer: high irradiance, max power | Solar is net cleaner than fossil fuels |

| 💧 Water Usage | Low water use in operation (vs coal plants) | Manufacturing (cooling, wafer cutting) consumes water; panel cleaning in arid zones stresses supply | Monsoon: reduced generation due to cloud cover | Smart cleaning tech reducing water footprint |

| 🌱 Land Use & Ecology | Desert solar parks → use of barren land | Large projects may disrupt biodiversity/agriculture if poorly planned | Winter: shorter days, reduced output in higher latitudes | Floating/canal-top PV reduces land conflicts |

| 🔋 Resource & Recycling | Panels last 25+ years, recyclable glass/aluminum | Recycling of silicon, silver, toxic elements still underdeveloped | Seasonal demand surges (summer A/C load, winter heating) | Circular economy models emerging |

| 🔆 Energy Independence | Reduces reliance on imported fossil fuels | Supply chain still dependent on few countries for raw materials | Seasonal peak-demand mismatch with generation profile | Storage solutions bridging gaps |

| 🌡️ Climate Resilience | Solar helps decarbonize grid → mitigates climate change | Panels degrade faster under high heat, dust, humidity | Extreme heat lowers efficiency; dust storms cut yield | New coatings, bifacial, and O&M robotics help maintain PR |

📊 Seasonal Effect on Solar in India & Global

- Summer (Apr–Jun): Best generation due to long sunny days and high irradiance.

- Monsoon (Jul–Sep): Sharp dip in generation in India/SE Asia due to clouds & rainfall.

- Autumn–Winter (Oct–Feb): Stable but reduced output; shorter daylight hours.

- Spring (Mar): Rising generation, good for grid balancing.

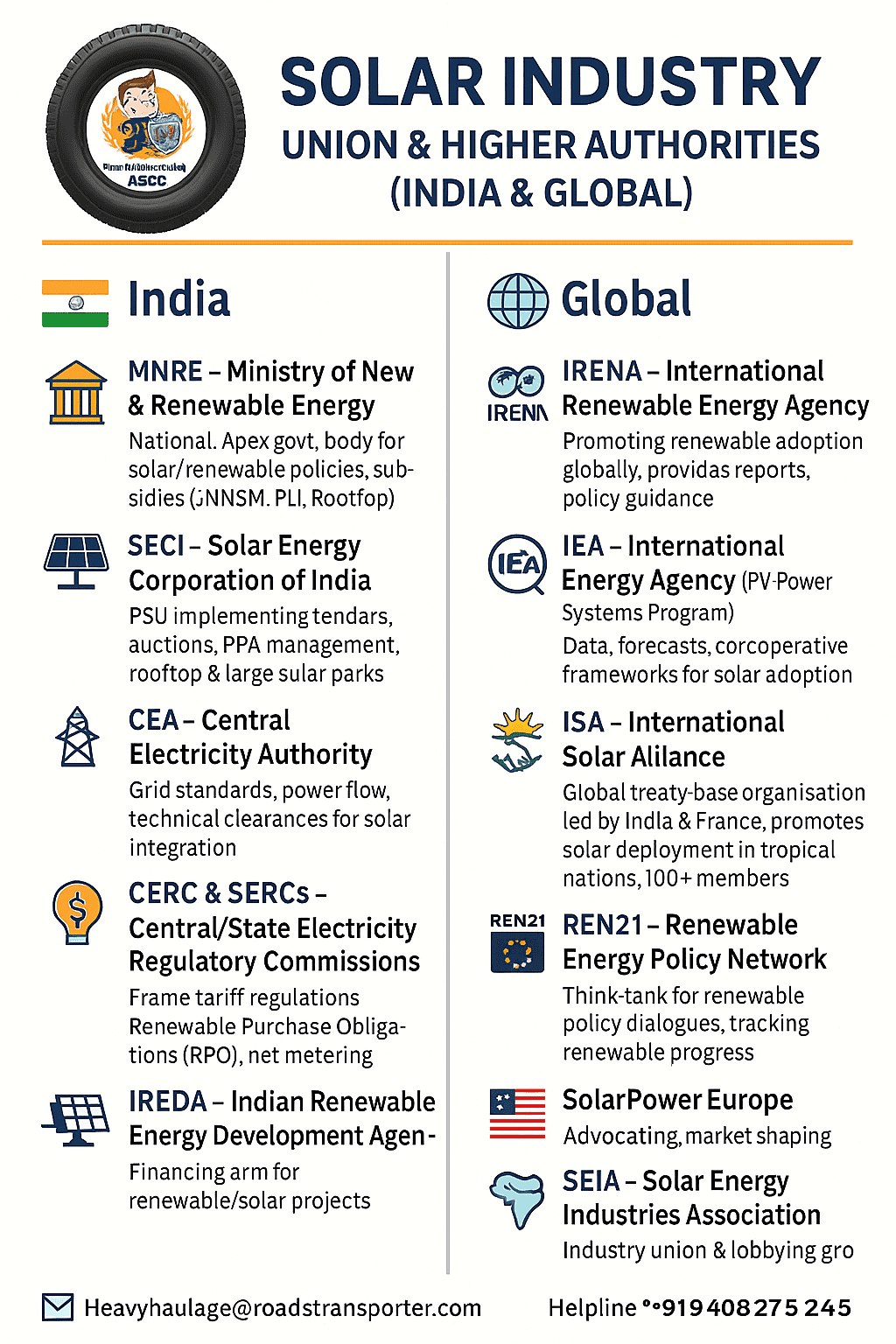

☀️ Solar Industry – Union & Higher Authorities (India & Global)

| 🌍 Level | 🏢 Authority / Union Name | 🌐 Region / Jurisdiction | 📌 Role & Functions |

|---|---|---|---|

| 🇮🇳 India | MNRE – Ministry of New & Renewable Energy | National (India) | Apex govt. body for solar/renewable policies, subsidies, missions (JNNSM, PLI, Rooftop). |

| SECI – Solar Energy Corporation of India | India | PSU implementing tenders, auctions, PPA management, rooftop & large solar parks. | |

| CEA – Central Electricity Authority | India | Grid standards, power flow, technical clearances for solar integration. | |

| CERC & SERCs – Central/State Electricity Regulatory Commissions | India | Frame tariff regulations, Renewable Purchase Obligations (RPO), net metering. | |

| IREDA – Indian Renewable Energy Development Agency | India | Financing arm for renewable/solar projects. | |

| ISMA – Indian Solar Manufacturers Association | India | Industry body for domestic manufacturers; lobbying & policy support. | |

| NISE – National Institute of Solar Energy | India | R&D, testing, training, and skill development for solar industry. | |

| 🌍 Global | IRENA – International Renewable Energy Agency | Global (170+ members) | Promotes renewable adoption globally, provides reports, policy guidance. |

| IEA – International Energy Agency (PV Power Systems Program) | Global / OECD | Data, forecasts, and cooperative frameworks for solar adoption. | |

| ISA – International Solar Alliance | Global (India-based, 100+ members) | Global treaty-based organization led by India & France; promotes solar deployment in tropical nations. | |

| REN21 – Renewable Energy Policy Network | Global | Think-tank for renewable policy dialogues, tracking renewable progress. | |

| SolarPower Europe | EU | Represents European solar companies; advocacy, market shaping. | |

| SEIA – Solar Energy Industries Association | USA | Industry union & lobbying group for solar firms in America. | |

| ASEAN Centre for Energy (ACE) | Southeast Asia | Regional platform for renewable collaboration including solar. |

☀️ Advantages & Disadvantages of the Solar Industry

| ✅ Advantages | ⚠️ Disadvantages / Challenges |

|---|---|

| 🌞 Clean & Renewable: No emissions during operation; reduces dependence on fossil fuels. | 🌑 Intermittency: Solar power depends on sunlight; cloudy/rainy seasons reduce efficiency. |

| 💰 Lower Operating Costs: After installation, minimal maintenance; long life (25+ years). | 💸 High Initial Investment: Upfront CAPEX for panels, inverters, and storage can be high. |

| 🌍 Energy Independence: Reduces imports of coal, oil, and gas; improves national security. | 🏭 Manufacturing Impact: Polysilicon refining, glass, and metals require energy and generate emissions. |

| 👷 Job Creation: Manufacturing, installation, O&M, and logistics provide millions of jobs. | 🌱 Land Use Issues: Large solar farms need vast land areas, may compete with agriculture. |

| 🔋 Scalability & Versatility: Rooftop, utility parks, floating, canal-top PV possible. | 🔋 Storage Requirement: Battery/storage costs remain high to ensure 24×7 reliability. |

| 🏘️ Decentralized Access: Rural electrification, mini-grids, and solar pumps empower villages. | 🛠️ Recycling Challenge: End-of-life panel recycling is still underdeveloped; risk of e-waste. |

| 📉 Falling Costs: Module prices dropped from $3/W (2010) to <$0.20/W today. | 📊 Market Volatility: Prices fluctuate due to supply chain, trade policies, raw material cycles. |

☀️ Legal & Compliance Framework + Quality Standards in the Solar Industry

| ⚖️ Area | 🇮🇳 India (Local) | 🌍 Global / International | 📑 Quality Standards & Certifications |

|---|---|---|---|

| Policy & Governing Authority | MNRE (Ministry of New & Renewable Energy) – apex policymaker | IRENA / IEA / ISA – promote renewables globally | IEC (International Electrotechnical Commission) – IEC 61215 (design), IEC 61730 (safety) |

| Project Development & Regulation | SECI (Solar Energy Corporation of India) – tenders, PPAs, auctions | Regional unions (EU – SolarPower Europe, USA – SEIA) | ISO 9001 (Quality Management), ISO 14001 (Environmental) |

| Tariffs & Purchase Obligations | CERC & SERCs – set tariffs, net metering, Renewable Purchase Obligations (RPO) | REN21 – renewable policy network guidance | UL Certification (USA), TÜV Rheinland (EU testing/certification) |

| Financing & Incentives | IREDA – financing arm for solar projects | World Bank / ADB / IMF green funds | BIS (Bureau of Indian Standards) – mandatory for solar modules in India |

| Research & Training | NISE (National Institute of Solar Energy) – testing, R&D, skill dev. | International R&D consortia (PVPS, EU Horizon programs) | ISO 45001 (Occupational Health & Safety), RoHS (Hazardous substances compliance) |

| Manufacturing Standards | ISMA (Indian Solar Manufacturers Association) – advocacy, domestic policy | Global traceability & supply chain laws (USA – Uyghur Forced Labor Prevention Act, EU traceability) | Energy Star, CE Marking (Europe), PV Cycle (Recycling compliance) |

| Grid Compliance | CEA (Central Electricity Authority) – interconnection & grid code | Utility-scale standards per country (e.g., FERC in USA, ENTSO-E in EU) | IEC 61853 (Performance testing), IEC 62116 (Anti-islanding protection) |

| Environmental & Safety | MoEFCC (Ministry of Environment, Forest & Climate Change) – clearance for solar parks | UNFCCC / Paris Agreement frameworks | EHS Audits, LCA (Life Cycle Assessment) certifications |

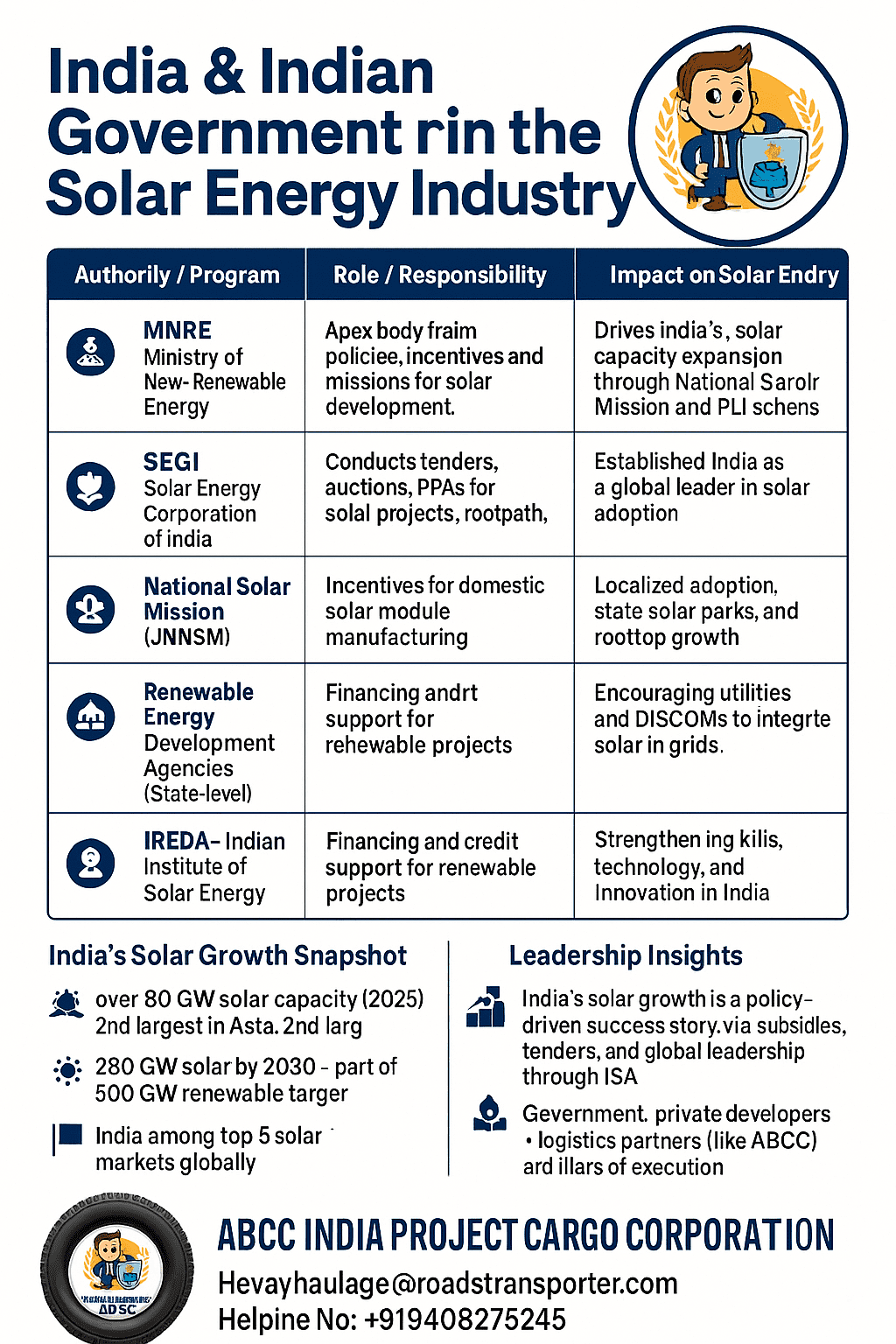

🇮🇳 India & Indian Government in the Solar Energy Industry

| 🏢 Authority / Program | 📌 Role / Responsibility | 💡 Impact on Solar Industry |

|---|---|---|

| MNRE – Ministry of New & Renewable Energy | Apex body framing policies, incentives, and missions for solar development. | Drives India’s solar capacity expansion through National Solar Mission and PLI schemes. |

| SECI – Solar Energy Corporation of India | Conducts tenders, auctions, PPAs for solar projects, rooftop, and solar parks. | Ensures large-scale deployment of solar with transparent bidding. |

| National Solar Mission (JNNSM) | Launched in 2010 targeting 100 GW solar capacity by 2022. | Established India as a global leader in solar adoption. |

| PLI Scheme – Production Linked Incentive | Incentives for domestic solar module manufacturing. | Reduces imports, builds Atmanirbhar Bharat capacity. |

| Renewable Energy Development Agencies (State-level) | Each state has SREDA for implementation of local policies & rooftop schemes. | Localized adoption, state solar parks, and rooftop growth. |

| CERC & SERCs – Electricity Regulatory Commissions | Tariff setting, net metering regulations, and Renewable Purchase Obligations (RPO). | Encourage utilities and DISCOMs to integrate solar in grids. |

| IREDA – Indian Renewable Energy Development Agency | Financing and credit support for renewable projects. | Helps developers access affordable funding. |

| NISE – National Institute of Solar Energy | R&D, training, testing, and certification of solar products. | Strengthens skills, technology, and innovation in India. |

| International Solar Alliance (ISA) | Headquartered in Gurugram, India; co-founded by India & France. | Global treaty-based body promoting solar in 100+ countries. |

☀️ Solar Industry Hubs & Big Markets in India

| 🏙️ Region / State | 📌 Solar Hub / Market | 🌞 Why Important | 🕰️ Seasonal Impact on Solar |

|---|---|---|---|

| Rajasthan | Bhadla Solar Park (world’s largest, >2.2 GW) | High irradiance desert land, large utility projects | Summer peak generation, minor dust impact; stable winter; low monsoon |

| Gujarat | Charanka Solar Park, Dholera Solar Park | Proactive state policy, coastal sites, strong DISCOM support | Summer strong; monsoon cloudy impact; good winter yield |

| Madhya Pradesh | Rewa Ultra Mega Solar Park | Central location, PPA with metro & industries | Summer max; monsoon dip; stable in post-monsoon |

| Karnataka | Pavagada Solar Park | Large-scale government-backed projects | Summer high; monsoon reduction; balanced winter |

| Tamil Nadu | Kamuthi Solar Power Project | Industrial state demand + high solar radiation | Summer/winter strong; monsoon dips |

| Andhra Pradesh | Kurnool & Anantapur Solar Parks | Large flat land, state policies, strong C&I demand | Summer/winter stable; monsoon cloud dips |

| Telangana | Multiple solar clusters | Good irradiance + rooftop push | Summer peak; monsoon lower |

| Maharashtra | Industrial hubs with growing solar demand | Rooftop and C&I adoption strong | Summer high; monsoon dip |

| Punjab & Haryana | Agro-solar push, canal-top projects | Agri + rooftop + canal-top PV | Summer high; foggy winters reduce yield |

| Uttar Pradesh | Rooftop & utility-scale demand rising | High population, rooftop subsidies | Seasonal variability; strong summer |

| Kerala | Rooftop-driven market | High literacy, rooftop penetration | Monsoon heavy → solar yield drops significantly |

| Northeast India | Emerging rooftop and small-scale | Distributed solar; state incentives | Seasonal cloud cover challenges |

☀️ Major Solar Parks in India

| 🏙️ State | 🌞 Solar Park Name | ⚡ Capacity (Approx.) | 📌 Highlights |

|---|---|---|---|

| Rajasthan | Bhadla Solar Park | 2,245 MW+ | World’s largest solar park; desert terrain with high irradiance. |

| Karnataka | Pavagada Solar Park | 2,050 MW+ | Spread over 13,000 acres; developed under PPP model with land leasing. |

| Andhra Pradesh | Kurnool Ultra Mega Solar Park | 1,000 MW | Among India’s first gigawatt-scale solar parks. |

| Madhya Pradesh | Rewa Ultra Mega Solar Park | 750 MW | Supplies power to Delhi Metro; benchmark tariffs for India. |

| Tamil Nadu | Kamuthi Solar Power Project | 648 MW | Once the world’s largest single-site solar plant. |

| Andhra Pradesh | Ananthapuramu – I & II Solar Park | 1,500 MW+ (planned) | Large-scale expansion in southern AP. |

| Gujarat | Charanka Solar Park (Gujarat Solar Park – I) | 600 MW+ | Flagship state-led solar project. |

| Gujarat | Dholera Solar Park | 5,000 MW (planned) | Future mega-project under development. |

| Telangana | NTPC & State-led Clusters | 500–1,000 MW cumulative | Rooftop + ground-mounted parks spread across districts. |

| Uttar Pradesh | Etah & Bundelkhand Solar Parks | 600 MW+ (combined, under dev.) | Focus on UP’s growing demand & rooftop support. |

| Maharashtra | Sakri Solar Plant | 125 MW | Maharashtra’s largest operational solar project. |

| Punjab & Haryana | Canal-Top Solar Projects | Small to medium (10–100 MW) | Innovative use of canal space for solar. |

| Kerala | Kayamkulam Floating Solar Plant (NTPC) | 105 MW (phase-1) | Largest floating solar plant in India. |

☀️ Solar Industry – Most Selling Items & Raw Material Rate Chart (with Big Suppliers)

| 🔆 Category | 📌 Item / Raw Material | 💰 Tentative Rate (India, 2025) | 🏭 Major Suppliers (Indicative) | 📑 Notes |

|---|---|---|---|---|

| Solar Modules | Mono-PERC/Bifacial Module (550–650 Wp) | ₹18,000 – ₹24,000 per module (~₹22–26/Wp) | Adani Solar (India), Vikram Solar (India), LONGi, Jinko, Trina (Global) | Most selling product; bulk demand in utility & rooftop |

| Solar Cells | Mono-PERC / TOPCon Cells | ₹13–15 per Wp | Waaree (India), Adani, Tongwei (China), Aiko Solar (China) | Efficiency drives pricing; India scaling local cell fabs |

| Inverters | Central Inverter (1–5 MW) | ₹15–25 lakh per unit | Sungrow, Huawei, TMEIC, Hitachi, ABB | Utility-scale use |

| String Inverter (10–250 kW) | ₹20,000 – ₹2,00,000 | SMA, Growatt, Delta, Waaree, Solis | Rooftop & C&I segment | |

| Mounting Structures | Hot-Dip Galvanized Steel Structures | ₹20–25/kg | Jindal Steel, Tata Steel, ISMT, Strolar | Seasonal steel price fluctuation |

| Trackers | Single Axis Solar Tracker | ₹8–12 lakh / MW | Nextracker, Array Tech, TrinaTracker | Used in utility-scale for yield gain |

| Raw Materials – Polysilicon | High-Purity Polysilicon | ₹3.5–4.5 lakh/MT | GCL Poly, Daqo, Wacker, OCI | Key base material for wafers |

| Raw Materials – Glass | Solar Glass (3.2mm tempered) | ₹40–50/sq.ft | Borosil Renewables (India), Xinyi (China) | Glass quality critical for efficiency |

| Raw Materials – EVA/POE Sheets | Encapsulation Sheets | ₹100–130/kg | Mitsui, Hangzhou First, RenewSys (India) | Protects cells in modules |

| Raw Materials – Backsheet | Fluoro/Non-Fluoro Backsheets | ₹120–150/sq.mtr | DuPont, Coveme, RenewSys | Determines module durability |

| Raw Materials – Aluminum Frames | Anodized Aluminum | ₹250–300/kg | Hindalco, Norsk Hydro | Lightweight, corrosion resistance |

| Cables & Junction Boxes | DC Cables, Combiner Boxes | ₹60–80/mtr (DC cables) | Polycab, KEI, Lapp | Key for BOS reliability |

| Transformers & Switchgear | Solar Duty Transformers | ₹15–40 lakh depending on capacity | BHEL, Siemens, CG Power | High voltage evacuation from parks |

☀️ Solar Industry – Best Vendors State-Wise

| 🏙️ State / UT | 🏭 Best Vendor / Company | 📧 Contact / Email | 📌 Why Best | 💰 Budget Range (Approx.) |

|---|---|---|---|---|

| Andhra Pradesh | Premier Energies | [email protected] | Top integrated module manufacturer, strong EPC presence | ₹20 L – ₹5 Cr |

| Arunachal Pradesh | Rooftop Integrators – State NREDA tie-ups | govt nodal | Local service providers with subsidy linkages | ₹5 L – ₹50 L |

| Assam | Jackson Solar | [email protected] | Reliable EPC, rooftop leader in NE India | ₹10 L – ₹2 Cr |

| Bihar | Vikram Solar EPC division | [email protected] | Leading EPC with state DISCOM experience | ₹25 L – ₹3 Cr |

| Chhattisgarh | Waaree Energies | [email protected] | Big distributor presence + O&M network | ₹15 L – ₹4 Cr |

| Delhi (NCT) | Tata Power Solar | [email protected] | Rooftop leader in NCR; strong residential market | ₹2 L – ₹1 Cr |

| Goa | Servotech Power Systems | [email protected] | Localized rooftop EPC with MNRE linkages | ₹5 L – ₹50 L |

| Gujarat | Adani Solar | [email protected] | India’s largest manufacturer, utility-scale leader | ₹50 L – ₹100 Cr |

| Haryana | Goldi Solar | [email protected] | Strong rooftop EPC, subsidy-driven | ₹10 L – ₹3 Cr |

| Himachal Pradesh | Local EPC + Waaree partners | state nodal | Rooftop + small ground projects | ₹5 L – ₹50 L |

| Jharkhand | Vikram Solar EPC + State tender vendors | [email protected] | DISCOM-based programs, small scale EPC | ₹15 L – ₹2 Cr |

| Karnataka | ReNew Power (EPC) + Adani | [email protected] | Large solar park projects (Pavagada) | ₹1 Cr – ₹100 Cr |

| Kerala | KSEB empaneled EPCs (Agency list) | nodal contacts | Rooftop/subsidy-driven | ₹3 L – ₹50 L |

| Madhya Pradesh | Rewa Ultra Mega Solar Park EPCs (ACME, Mahindra) | corporate contacts | Utility-scale pioneers in MP | ₹1 Cr – ₹100 Cr |

| Maharashtra | Waaree Energies HQ | [email protected] | Largest rooftop distribution + EPC | ₹10 L – ₹50 Cr |

| Manipur | Rooftop EPCs (state nodal empaneled) | – | Small-scale rooftop systems | ₹3 L – ₹30 L |

| Meghalaya | Rooftop-focused EPCs | – | Government rooftop subsidy market | ₹2 L – ₹25 L |

| Mizoram | Small EPC contractors | – | Local rooftop/grid-tied systems | ₹2 L – ₹20 L |

| Nagaland | Rooftop integrators | – | Subsidy-driven small EPCs | ₹2 L – ₹20 L |

| Odisha | Jakson + Tata EPC | [email protected] | Strong industrial + rooftop projects | ₹15 L – ₹4 Cr |

| Punjab | Hartek Solar | [email protected] | Rooftop, C&I EPC; canal-top solar leader | ₹20 L – ₹5 Cr |

| Rajasthan | Adani + ACME Solar | [email protected] | Bhadla Solar Park leaders; large EPC | ₹10 Cr – ₹200 Cr |

| Sikkim | Rooftop EPCs | – | Small grid-connected | ₹2 L – ₹25 L |

| Tamil Nadu | Sterling & Wilson Solar | [email protected] | Global EPC leader, Kamuthi project | ₹5 Cr – ₹200 Cr |

| Telangana | Premier Energies HQ | [email protected] | Big manufacturer + EPC | ₹50 L – ₹50 Cr |

| Tripura | Rooftop EPC contractors | – | State-level solar push | ₹2 L – ₹25 L |

| Uttar Pradesh | Tata Power Solar + Jakson Solar (Noida HQ) | [email protected] | Big rooftop + industrial EPC | ₹5 L – ₹50 Cr |

| Uttarakhand | State nodal EPCs | – | Rooftop focus | ₹2 L – ₹25 L |

| West Bengal | Vikram Solar HQ | [email protected] | One of India’s biggest manufacturers | ₹25 L – ₹100 Cr |

| Chandigarh (UT) | CREST Rooftop EPC program | state contacts | Rooftop + subsidy success | ₹5 L – ₹50 L |

| Andaman & Nicobar | NTPC Floating Solar EPCs | NTPC | Island microgrids + floating PV | ₹1 Cr – ₹20 Cr |

| J&K & Ladakh | SECI/NTPC projects | – | Cold-climate PV projects | ₹50 L – ₹10 Cr |

| Puducherry | Small EPC vendors | – | Rooftop market only | ₹3 L – ₹25 L |

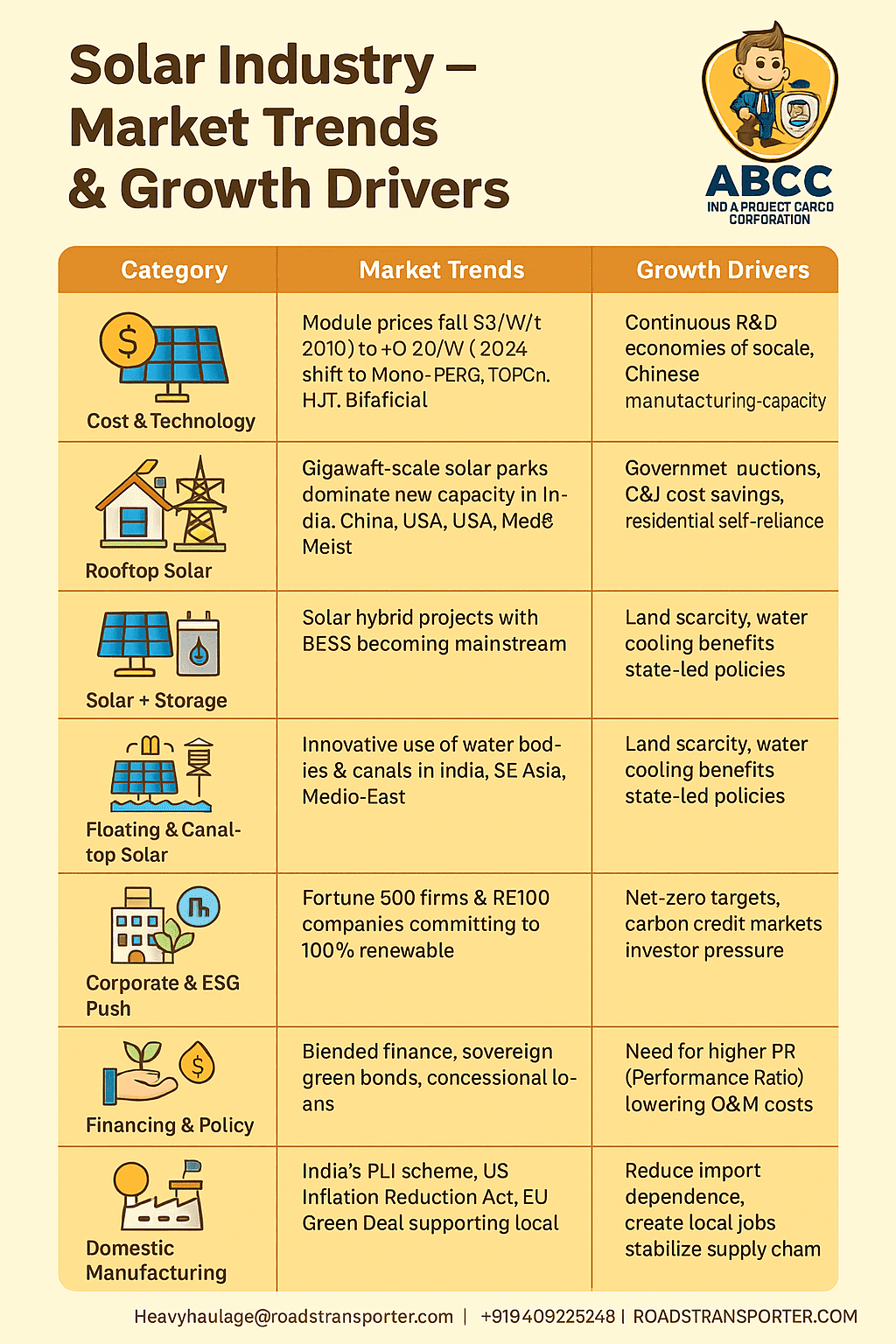

☀️ Solar Industry – Market Trends & Growth Drivers

| 📊 Category | 🔆 Market Trends | 🚀 Growth Drivers |

|---|---|---|

| Cost & Technology | Module prices fell from $3/W (2010) to <$0.20/W (2024); shift to Mono-PERC, TOPCon, HJT, Bifacial | Continuous R&D, economies of scale, and Chinese manufacturing capacity |

| Utility-Scale Projects | Gigawatt-scale solar parks dominate new capacity in India, China, USA, Middle East | Competitive auctions, lower LCOE vs coal, corporate RE demand |

| Rooftop Solar | Rapid adoption in India, EU, US, Japan; driven by net metering and subsidies | Government incentives, C&I cost savings, residential self-reliance |

| Solar + Storage | Solar hybrid projects with BESS becoming mainstream | Falling battery prices, need for 24×7 renewable supply |

| Floating & Canal-Top Solar | Innovative use of water bodies & canals in India, SE Asia, Middle East | Land scarcity, water cooling benefits, state-led policies |

| Corporate & ESG Push | Fortune 500 firms and RE100 companies committing to 100% renewable | Net-zero targets, carbon credit markets, investor pressure |

| Green Hydrogen Integration | Solar powering electrolyzers for hydrogen production | Global hydrogen economy, industrial decarbonization policies |

| Digitalization & O&M | AI-driven predictive maintenance, drone inspections, robotic cleaning | Need for higher PR (Performance Ratio), lowering O&M costs |

| Financing & Policy | Blended finance, sovereign green bonds, concessional loans | International funds (World Bank, ADB), supportive state & central policies |

| Domestic Manufacturing | India’s PLI scheme, US Inflation Reduction Act, EU Green Deal supporting local fabs | Reduce import dependence, create local jobs, stabilize supply chain |

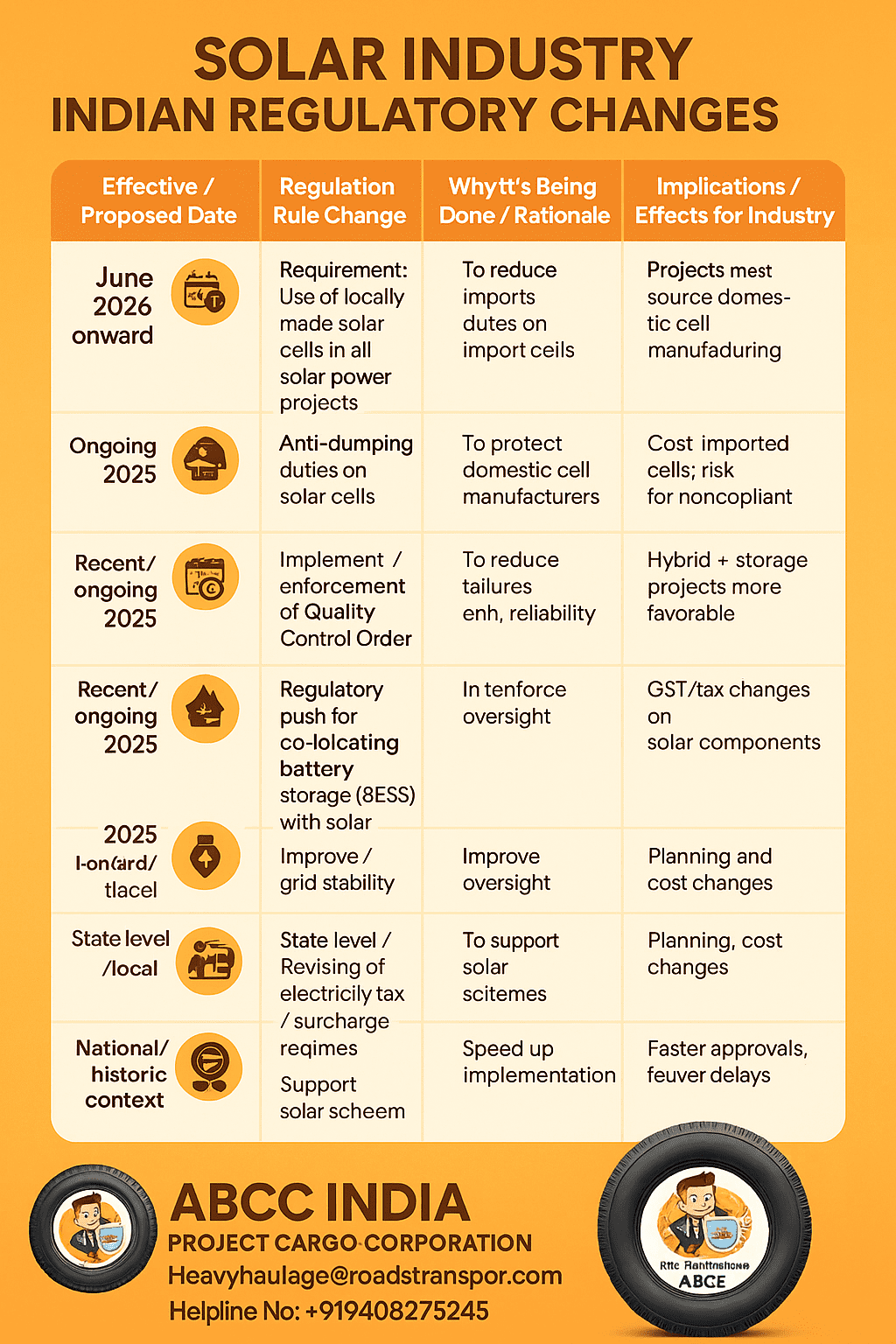

🇮🇳 Major Regulatory Changes in India’s Solar Industry (and Why They Matter)

| 📅 Effective / Proposed Date | ⚙️ Regulation / Rule Change | 🤔 Why It’s Being Done / Rationale | 📝 Implications / Effects for Industry |

|---|---|---|---|

| June 2026 onward | Requirement: Use of locally-made solar cells in all clean energy / solar power projects | To reduce dependence on imports (especially from China), boost local manufacturing, and secure supply chains | Projects must source domestic cell makers; foreign cell imports will be restricted; list of approved manufacturers will matter heavily |

| Ongoing / 2025 | Anti-dumping duties on solar cells (imported) | To protect domestic cell manufacturers from unfairly low-priced imports | Cost of imported cells will increase; domestic industry gets breathing space; developers will recalibrate procurement strategy |

| 2025 | Implementation / enforcement of Quality Control Order (for modules, inverters, etc.) | To improve reliability, reduce failures, and ensure performance (durability, safety) across solar installations | Vendor vetting stricter; non-compliant products may be banned or penalized; higher upfront quality costs but lower lifecycle risk |

| Recent / ongoing | Regulatory push for co-locating battery storage (BESS) with solar | To manage grid stability, reduce deviation penalties, and make solar “dispatchable” | Hybrid (solar + storage) projects become more favorable; standalone solar may face higher risk from grid penalties |

| 2025–onwards | Tighter Deviation Settlement Mechanism (DSM) / grid discipline rules for renewable producers | To enforce grid stability and penalize imbalances in supply vs scheduled output | Renewable developers may need storage or buffering; project financial modeling must account for penalties |

| 2025 | Import monitoring & tracking system for solar equipment | To improve oversight over imported modules, cells, and components; curb illicit/undervalued imports | All importers will have to comply with stricter documentation and tracking; compliance risk increases |

| 2025 | GST / tax changes on solar components | To adjust tax burdens and encourage deployment | Recently, there’s talk of reducing GST on modules & devices from 12 % to lower to promote adoption |

| State level / local rules | States revising electricity tax / surcharge regimes, subsidy frameworks, etc. (e.g. Maharashtra increasing sales tax to fund solar pumps) | To support state-level solar schemes (such as agricultural pumps) and cross-subsidize rural solar programs | Industrial / commercial consumers may see higher power cost; project planning in states needs that local tax risk factored |

| Regulatory / procedural | Easier clearance via single-window systems, decriminalization, faster approvals | To reduce red tape, speed up solar project implementation | Faster permit approvals, fewer delays, better predictability |

| National / historic context | Domestic Content Requirement (DCR) policies | India has periodically required modules / cells to be locally produced for eligibility in certain tenders | Incentivizes local manufacturing; importers / foreign players must localize or partner |

🔍 Key Trends & Strategic Takeaways

Make in India is turning into “Must in India”

The June 2026 cell localization mandate is a turning point. It will force global players to set up local plants or lose business.

Domestic manufacturers will gain strategic advantage.

Hybrid (Solar + Storage) becomes the default architecture

Because of stricter DSM rules and incentives for storage, future solar projects will largely be hybrid setups.

Quality & reliability now legally mandated

Quality control orders and testing regimes will weed out substandard vendors.

Developers must choose trusted brands or risk compliance failures.

Cost structure shifts

Import duties + anti-dumping measures will raise costs for imported cells/components.

Modules, inverters, etc., will see more emphasis on local sourcing.

Regulatory risk is state-specific

States like Maharashtra are using electricity taxes and surcharges to fund solar schemes for agriculture. Developers must understand local tax and policy regimes.

Project viability modeling must evolve

Project financial models must include storage costs, DSM penalties, compliance overheads.

Contracts (PPAs) will need flexibility to adapt to regulation changes.

Timing matters

Developers who lock in procurement before the regulatory changes (e.g. before June 2026) may have an edge, but also risk misalignment if rules change.

Long-term projects must be future-proofed.

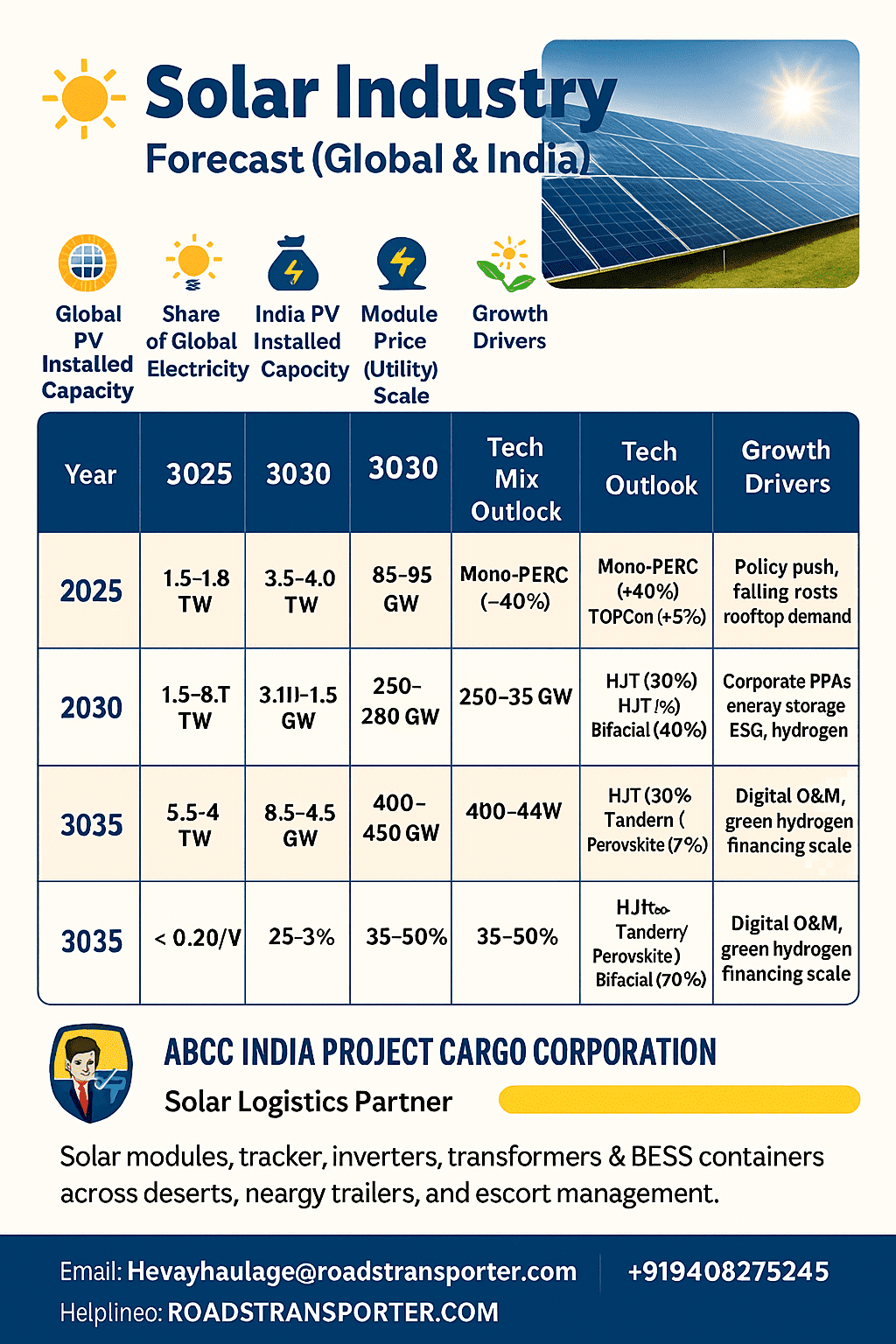

☀️ Solar Industry – Forecast (Global & India)

| 📅 Year | 🌍 Global PV Installed Capacity | ⚡ Share of Global Electricity | 🇮🇳 India PV Installed Capacity | 💸 Module Price (Utility Scale) | 🔋 Storage Attach Rate | 🔧 Tech Mix Outlook | 🚀 Growth Drivers |

|---|---|---|---|---|---|---|---|

| 2025 | 1.5–1.8 TW | 6–7% | 85–95 GW | <$0.20/W | 10–15% | Mono-PERC (~40%), TOPCon (~50%), Bifacial (~40%) | Policy push, falling costs, rooftop demand |

| 2030 | 3.5–4.0 TW | 12–15% | 250–280 GW | $0.12–0.16/W | 25–35% | TOPCon (~55%), HJT (~20%), Perovskite (~5%), Bifacial (~60%) | Corporate PPAs, energy storage, ESG, hydrogen |

| 2035 | 5.5–6.5 TW | 18–22% | 400–450 GW | $0.10–0.14/W | 35–50% | HJT (~30%), Tandem/Perovskite (~15%), Bifacial (~70%) | Digital O&M, green hydrogen, financing scale |

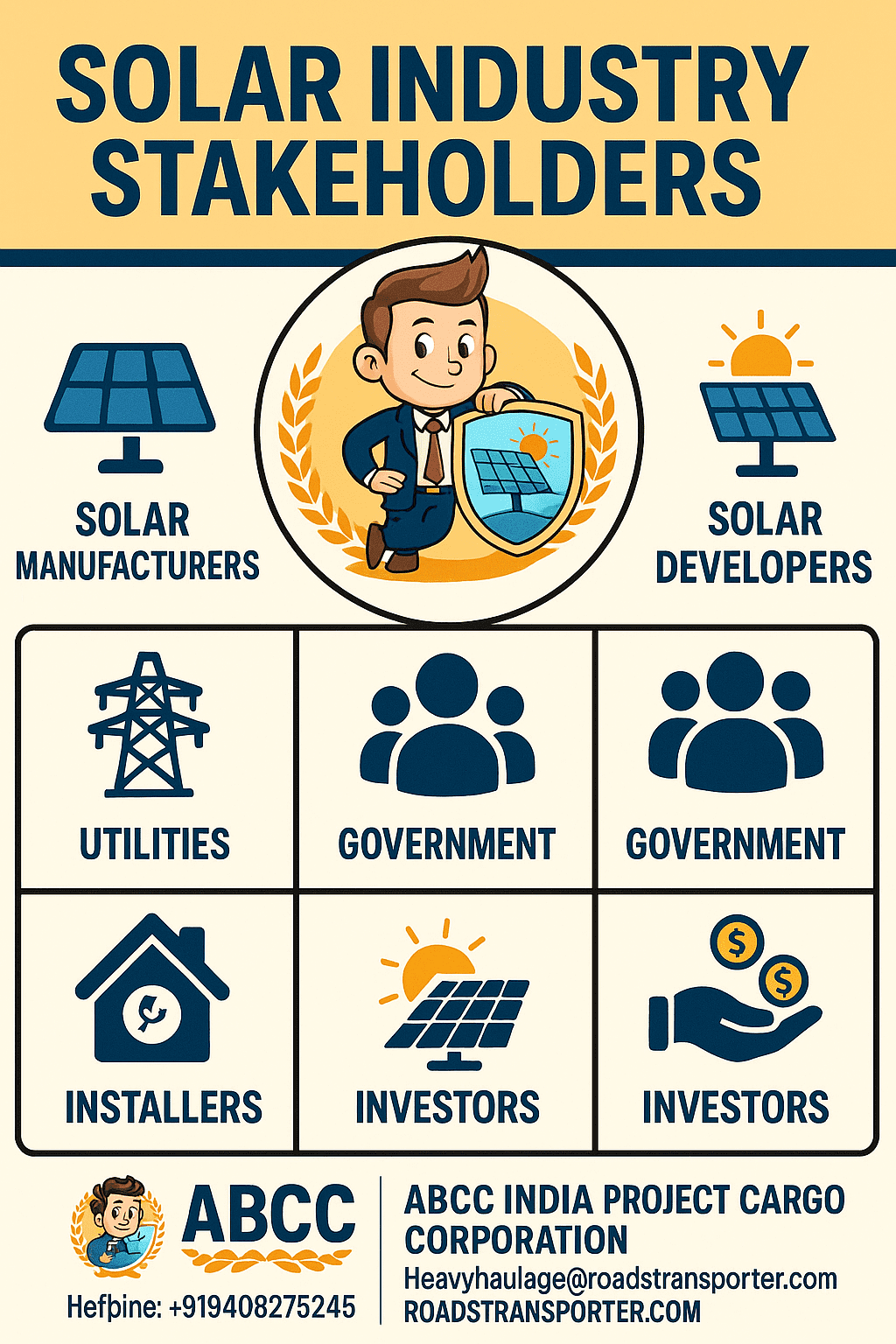

☀️ Solar Industry – Stakeholders

| 🏢 Category | 👥 Key Stakeholders | 📌 Role in Solar Industry |

|---|---|---|

| Government & Regulators | MNRE (India), SECI, CERC/SERCs, State Nodal Agencies | Policy making, subsidies, tenders, tariff regulation, compliance |

| Manufacturers | Adani Solar, Vikram Solar, Waaree, LONGi, Jinko, Trina, Canadian Solar | Produce solar cells, modules, inverters, trackers, raw materials |

| Developers / EPC Companies | Tata Power Solar, ReNew Power, ACME Solar, Sterling & Wilson, Azure Power | Develop solar parks, rooftop projects, EPC execution |

| Investors & Financiers | IREDA, World Bank, ADB, Green Bonds, Private Equity, Banks | Provide capital, loans, green finance, PPAs |

| Technology Providers | SMA, Sungrow, Huawei, Borosil Renewables, RenewSys | Inverters, glass, backsheets, software, monitoring systems |

| Research & Training | NISE (India), IEC, ISO, Universities, R&D Labs | Testing, certifications, innovation, skill development |

| Corporates & Consumers | Industries (C&I sector), RE100 members, households | Buy and use solar power; rooftop installations; corporate PPAs |

| Logistics & Supply Chain | ABCC INDIA PROJECT CARGO CORPORATION | Transport solar modules, inverters, trackers, transformers, and ODC cargo safely across terrains |

| O&M Service Providers | Drone inspection firms, robotic cleaning startups, specialized contractors | Maintain and optimize solar farms |

| Global Bodies | IRENA, ISA, SEIA (USA), SolarPower Europe | Global advocacy, treaties, and renewable deployment strategies |

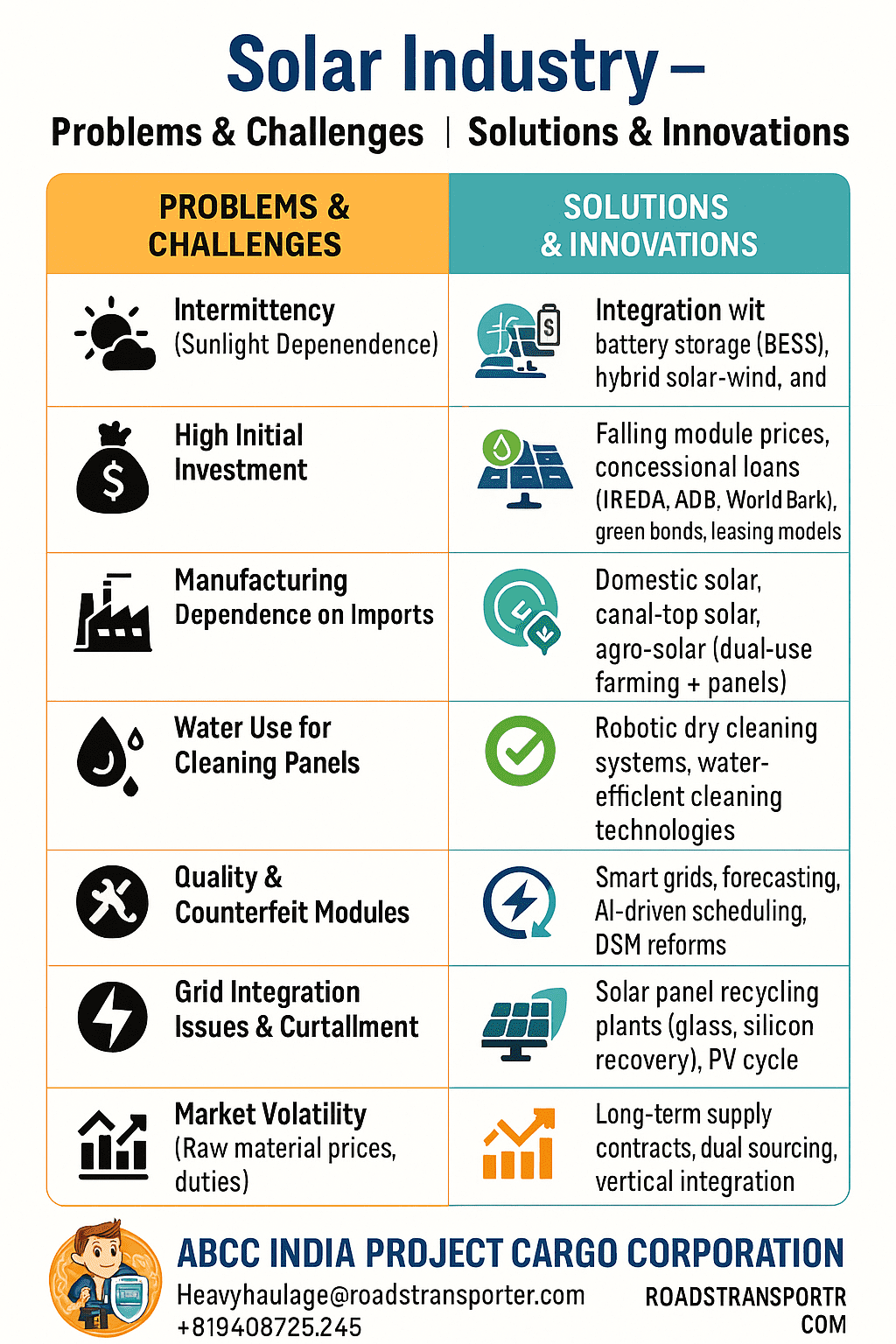

☀️ Solar Industry – Problems & Challenges / Solutions & Innovations

| ⚠️ Problems & Challenges | 💡 Solutions & Innovations |

|---|---|

| 🌑 Intermittency (Sunlight Dependence) | 🔋 Integration with battery storage (BESS), hybrid solar-wind, and pumped hydro solutions |

| 💸 High Initial Investment | 💰 Falling module prices, concessional loans (IREDA, ADB, World Bank), green bonds, leasing models |

| 🏭 Manufacturing Dependence on Imports | 🏭 Domestic manufacturing expansion via PLI schemes, Atmanirbhar Bharat, local glass & cell fabs |

| 🌱 Land Use Conflicts (Agriculture, Forests) | 🌿 Floating solar, canal-top solar, agro-solar (dual-use farming + panels) |

| 💧 Water Use for Cleaning Panels | 💧 Robotic dry cleaning systems, water-efficient cleaning technologies |

| 🛠️ Quality & Counterfeit Modules | ✅ BIS certification in India, IEC/ISO global standards, traceability systems |

| ⚡ Grid Integration Issues & Curtailment | ⚡ Smart grids, forecasting, AI-driven scheduling, DSM reforms |

| 🌍 Recycling & End-of-Life Management | 🔄 Solar panel recycling plants (glass, silicon recovery), PV cycle initiatives |

| 📊 Market Volatility (Raw material prices, duties) | 📊 Long-term supply contracts, dual sourcing, vertical integration |

| 🌡️ Performance in Extreme Climates (Dust, Heat, Snow) | 🌡️ Anti-soiling coatings, bifacial modules, advanced trackers, snow-shedding designs |

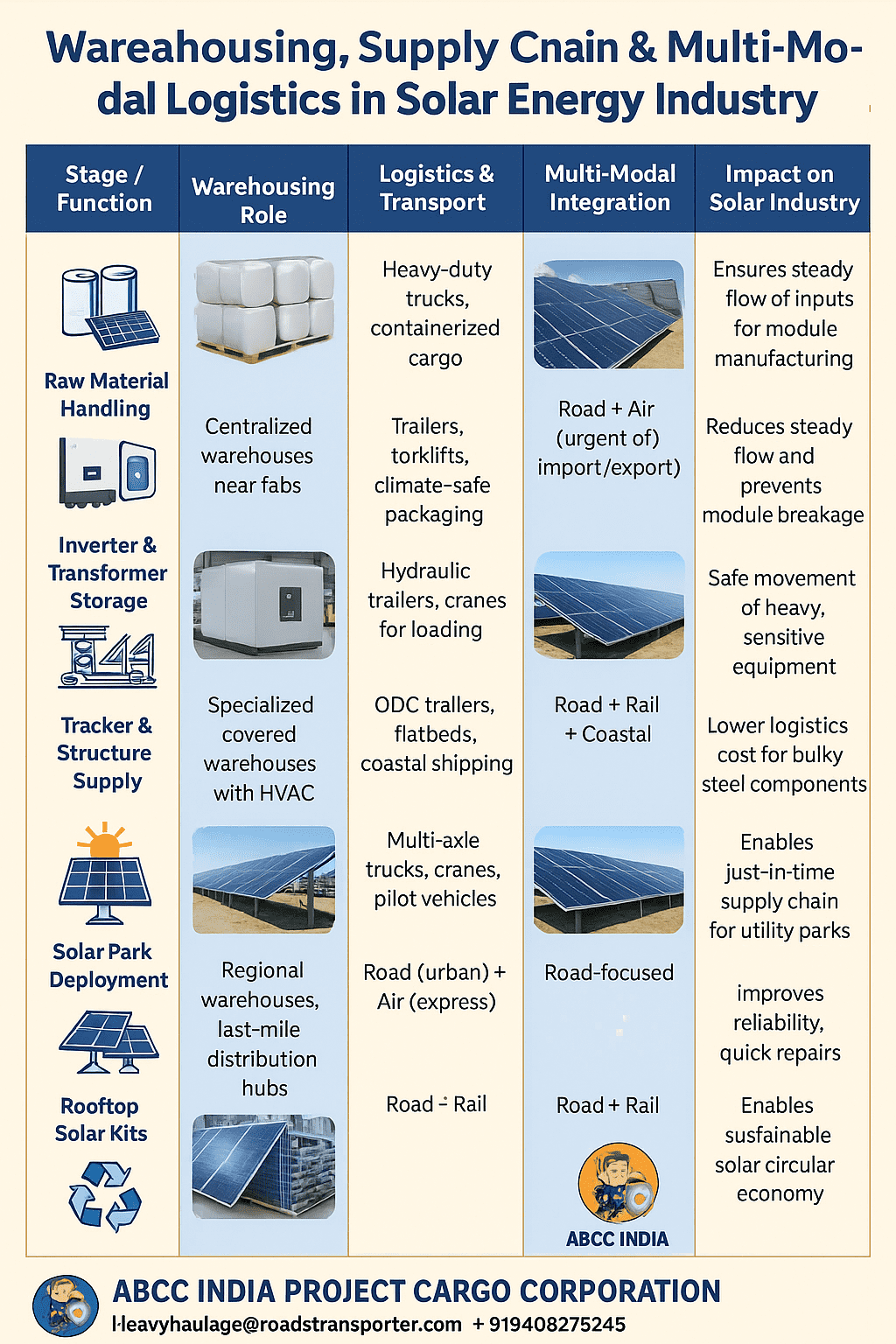

☀️ Warehousing, Supply Chain & Multi-Modal Logistics in Solar Energy Industry

| 🏢 Stage / Function | 📦 Warehousing Role | 🚚 Logistics & Transport | 🌐 Multi-Modal Integration | ⚡ Impact on Solar Industry |

|---|---|---|---|---|

| Raw Material Handling | Storage of polysilicon, glass, EVA, aluminum | Heavy-duty trucks, containerized cargo | Road + Rail for bulk movement | Ensures steady flow of inputs for module manufacturing |

| Module Manufacturing Supply | Centralized warehouses near fabs | Trailers, forklifts, climate-safe packaging | Road + Air (urgent import/export) | Reduces lead times and prevents module breakage |

| Inverter & Transformer Storage | Specialized covered warehouses with HVAC | Hydraulic trailers, cranes for loading | Road + Sea (import of inverters) | Safe movement of heavy, sensitive equipment |

| Tracker & Structure Supply | Open yards for steel frames, mounting structures | ODC trailers, flatbeds, coastal shipping | Road + Rail + Coastal | Lower logistics cost for bulky steel components |

| Solar Park Deployment | Regional warehouses near project sites | Multi-axle trucks, cranes, pilot vehicles | Road-dominant; Rail for long-distance bulk | Enables just-in-time supply chain for utility parks |

| Rooftop Solar Kits | Smaller warehouses, last-mile distribution hubs | Mini trucks, e-vehicles | Road (urban) + Air (express) | Fast installation for residential & commercial rooftops |

| O&M Supplies | Spare parts hubs, tools storage | Vans, medium trucks | Road-focused | Improves reliability, quick repairs |

| Recycling & End-of-Life | Collection centers, dismantling yards | Reverse logistics trucks, containers | Road + Rail | Enables sustainable solar circular economy |

🌞Solar Industry And ABCC India Project Cargo Corporation

The solar energy industry stands as a beacon of hope in the global transition toward clean, sustainable, and cost-effective power. From desert megawatt-scale solar parks to rooftop panels in cities and floating solar on water bodies, the sector is evolving rapidly with innovation, policy, and global collaboration.

Yet, no solar project can succeed without the backbone of logistics, warehousing, and heavy cargo movement. This is where ABCC INDIA PROJECT CARGO CORPORATION plays a defining role.

As India marches toward its 2030 renewable targets, ABCC ensures:

- Safe, on-time delivery of solar modules, inverters, transformers, trackers, and storage systems.

- Expertise in multi-modal logistics – road, rail, air, and coastal shipping.

- Complete support from warehousing to last-mile supply, even in remote terrains.

- Route surveys, crane operations, and ODC transport, enabling execution of the largest solar parks.

The future of solar energy lies not just in cheaper panels and new technologies but in integrated ecosystems where logistics, technology, and innovation align.

With its decades of expertise, ABCC INDIA PROJECT CARGO CORPORATION is not just a transporter — it is a strategic partner in powering India’s green future.

☀️ The Future of the Solar Energy Industry

🌍 Global Vision

- By 2030, solar will be the largest contributor to new electricity generation capacity worldwide.

- By 2050, solar could supply 25–30% of global electricity, supported by energy storage, smart grids, and green hydrogen.

- Perovskite & tandem solar cells, combined with bifacial and tracking systems, will deliver record efficiency.

🇮🇳 India’s Solar Future

- India aims for 280 GW of solar by 2030 as part of its 500 GW renewable goal.

- Expansion will be driven by mega solar parks in Rajasthan, Gujarat, MP, and Karnataka, as well as rooftop and rural solarization.

- Domestic manufacturing (PLI scheme) will make India a global hub for module and cell production.

- Hybrid projects (solar + wind + storage) and floating/canal-top PV will overcome land and seasonal challenges.

🔋 Technology & Innovation

- Storage Integration: Solar + Battery Energy Storage Systems (BESS) will make renewable power 24×7 reliable.

- Green Hydrogen: Solar will be the backbone of the hydrogen economy for steel, fertilizer, and transport industries.

- Digitalization: AI, drones, and robotics will drive predictive O&M, boosting performance and lowering costs.

- Circular Economy: Recycling plants will handle end-of-life modules, ensuring sustainability.

📊 Key Drivers

- Falling Costs: Solar remains the cheapest source of new energy.

- Policy Push: Global net-zero commitments and India’s ambitious renewable missions.

- Corporate Demand: C&I sector, EV charging, and data centers shifting to solar PPAs.

- Environmental Necessity: Rising climate risks making clean power adoption urgent.

🚚 ABCC INDIA PROJECT CARGO CORPORATION – Powering the Future of Solar

The solar future is not only about technology but also about execution and delivery.

ABCC ensures:

- Safe transport of solar modules, trackers, inverters, transformers, and storage systems.

- Multi-modal logistics: road, rail, sea, and air connectivity.

- Route surveys, cranes, and ODC cargo solutions for giga-scale projects.

- A reliable supply chain to connect manufacturers, EPCs, and solar parks across India.

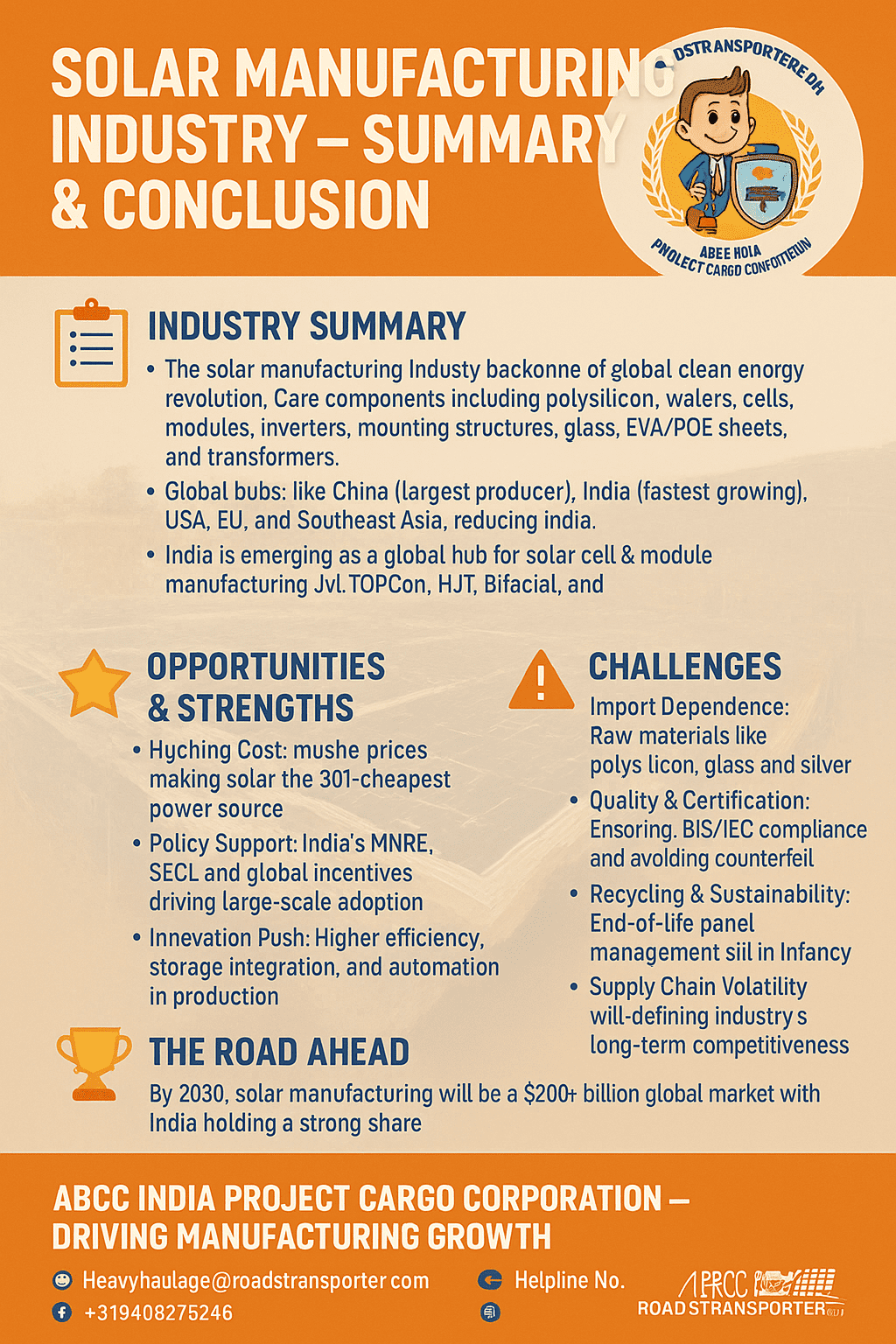

☀️ Solar Manufacturing Industry – Summary And Conclusion

📌 Industry Summary

- The solar manufacturing industry is the backbone of the global clean energy revolution.

- Core components include polysilicon, wafers, cells, modules, inverters, mounting structures, glass, EVA/POE sheets, and transformers.

- Global hubs: China (largest producer), India (fastest-growing), USA, EU, and Southeast Asia.

- India’s position: With policies like the PLI Scheme, India is emerging as a global hub for solar cell & module manufacturing, reducing dependency on imports.

- The industry is evolving with advanced technologies like TOPCon, HJT, Bifacial, and Perovskite/Tandem cells.

🔑 Opportunities & Strengths

- Cost Decline: Module prices have fallen drastically, making solar the cheapest power source.

- Policy Support: India’s MNRE, SECI, and global incentives are driving large-scale adoption.

- Innovation Push: Higher efficiency, storage integration, and automation in production.

- Green Hydrogen & EVs: Solar manufacturing is positioned to fuel these next-gen industries.

⚠️ Challenges

- Import Dependence: Raw materials like polysilicon, glass, and silver still heavily imported.

- Quality & Certification: Ensuring BIS/IEC compliance and avoiding counterfeit products.

- Recycling & Sustainability: End-of-life panel management still in infancy.

- Supply Chain Volatility: Global trade duties and raw material price swings affect margins.

🌟 The Road Ahead

- By 2030, solar manufacturing will be a $200+ billion global market with India holding a strong share.

- Domestic value chains will expand, from raw materials to module exports.

- Digital manufacturing, automation, and AI-driven quality checks will become the norm.

- Sustainability & recycling will define the industry’s long-term competitiveness.

🚚 ABCC INDIA PROJECT CARGO CORPORATION – Driving Manufacturing Growth

As the logistics backbone of the solar manufacturing industry, ABCC ensures:

- Safe transport of modules, inverters, raw materials, trackers, and transformers.

- Expertise in multi-modal logistics (road, rail, sea, air) for domestic & export supply chains.

- Warehousing & route surveys to optimize manufacturing-to-project delivery timelines.

- Enabling India’s vision of becoming a global solar manufacturing hub by 2030.

📧 Email: [email protected]

📞 Helpline No: +919408275245

🌐 Website: ROADSTRANSPORTER.COM

{kind=link}